Solar power farm in Cam Ranh, Vietnam. (Photo: iStock)

Vietnam is emerging as a significant player in the renewable energy market, attracting multinational corporations with its rapid economic growth and commitment to reducing carbon emissions. The Power Development Plan 8 (PDP 8) outlines ambitious goals to increase renewable energy capacity, making it a prime destination for foreign investment.

Right now, the country already has a high proportion of renewable energy in its installed capacity, but would it be enough for the growing demand from corporate users? This is pertinent question especially when the grid has demonstrated insufficient capacity to handle the new buildouts of VRE.

This article will discuss the current development and challenges in Vietnam’s renewable energy sector as well as the availability of renewable electricity for MNCs aiming to reduce their scope 2 emissions in the country. It is the first part of a two-part series on Vietnam’s renewable energy market.

Vietnam’s challenges in massive solar buildout and promises in wind capacity

Vietnam's renewable energy potential is immense, particularly in solar and wind power. The country’s coastal regions and tropical climate offer significant solar and wind energy resources, positioning Vietnam as a leader in Southeast Asia’s clean energy transition.

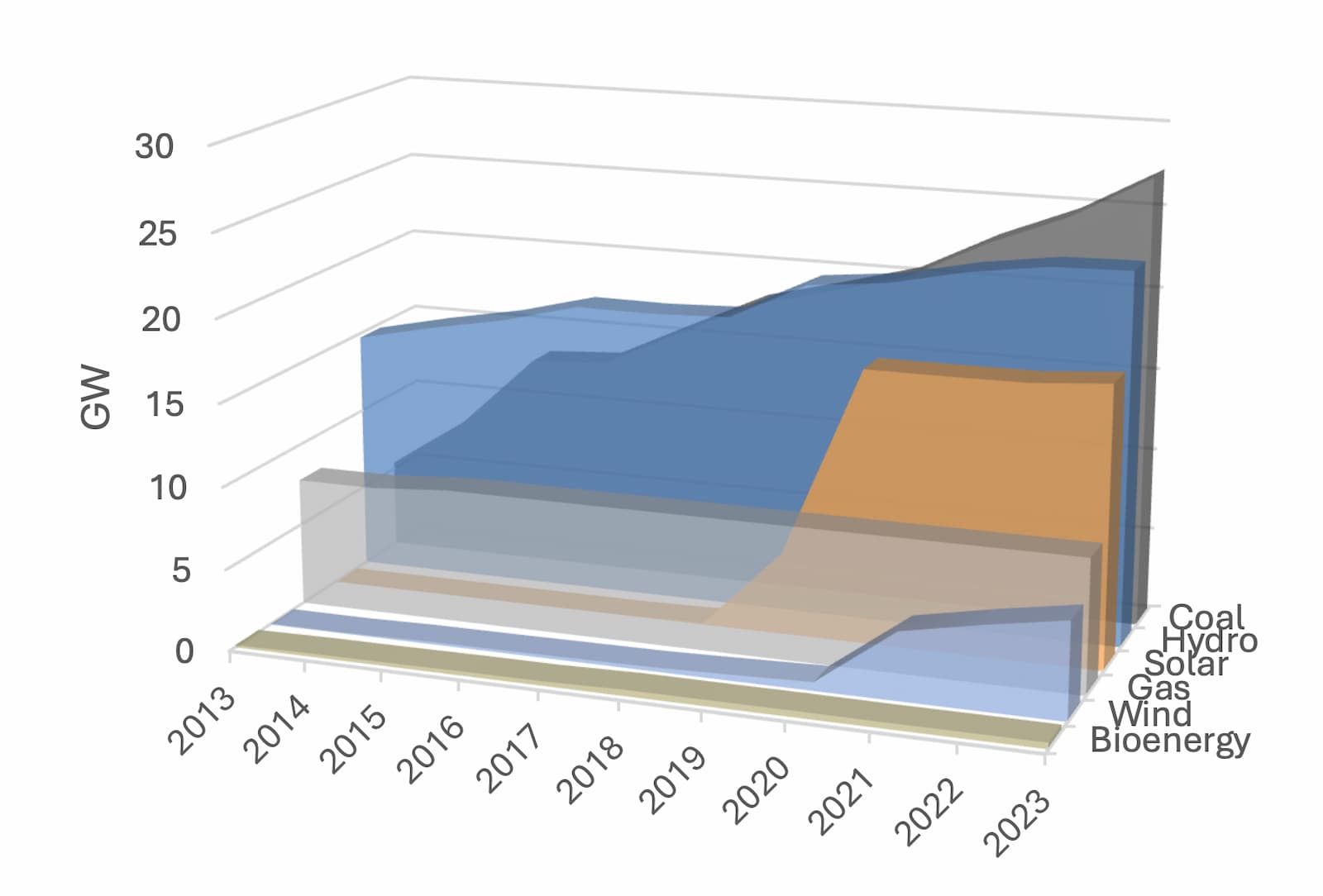

As of 2023, Vietnam had installed 17.08 GW of solar capacity, making it the largest solar power producer in the region, while onshore wind power capacity stood at around 5.89 GW with offshore wind gaining greater interest in the mid to long term. But in the short run, investors are hesitant about going into Vietnam’s offshore wind industry too quickly due to the lack of clear policy framework.

Graph 1. Vietnam energy mix in the past decade

In fact, solar capacity skyrocketed by over threefold from 2019 to 2020. Undoubtedly the favorable feed-in-tariff rates helped drove the astonishing growth. But as later revealed by the Government Inspectorate, among the 154 solar projects, 123 projects with the total capacity of 8,496 MW were approved under inadequate legal ground from 2016 to 2020. As a result, Vietnam actually exceeded the PDP VII target by 20-fold (PDP 7 set the target for 850 MW by 2020).

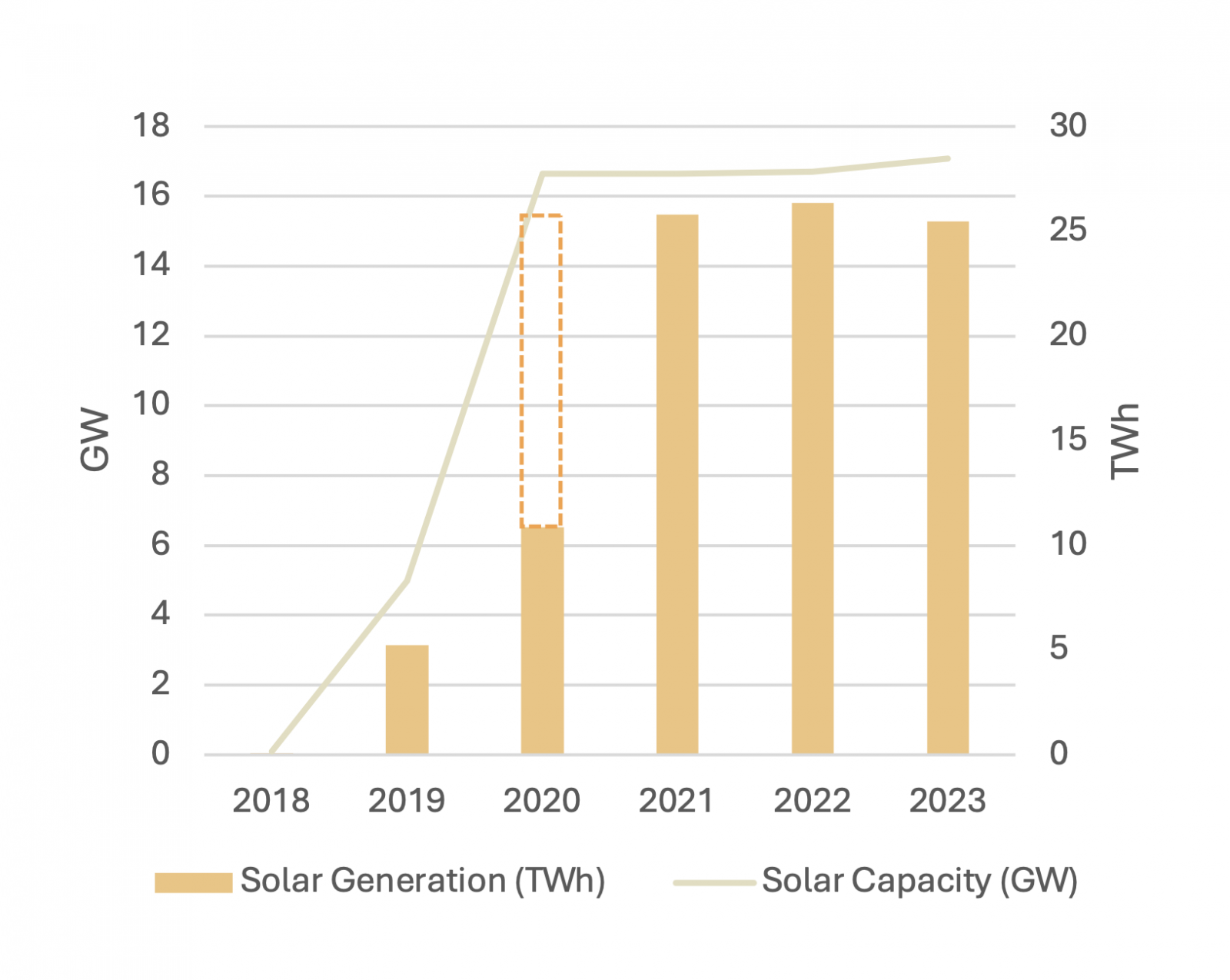

This uncontrolled pace of installation created immense strain on the national grid and led EVN to curtail excess solar electricity by close to 60% in 2020 (Graph 2). The FIT that drove this frenzy ended in the same year, resulting in little new solar capacity installation.

Graph 2. Solar power curtailment in 2020

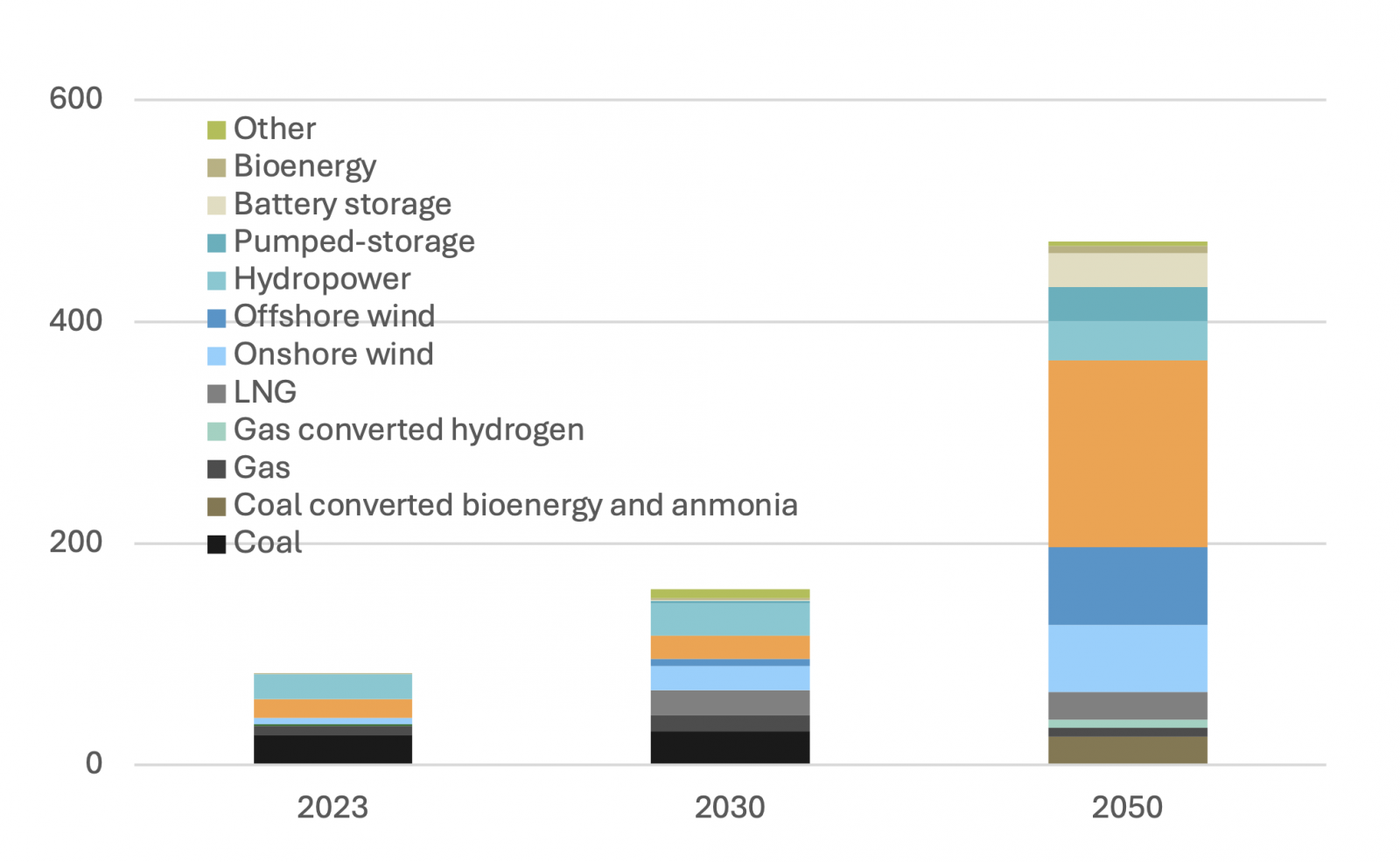

As solar capacity growth slows, another renewable energy is gaining attention – wind. PDP 8 aims to raise the current 43% of renewables to 47% by 2030. In the short term, the largest contributor of this effort would come from onshore wind, targeted with a 16 GW increase whereas solar capacity is planned with an additional 4 GW.

At the same time, offshore wind will grow from none as of today to 6 GW by 2030. Going towards 2050, onshore and offshore wind are expected to reach installed capacity of 60 GW and 70 GW respectively, substantially altering Vietnam’s energy mix.

Graph 3. PDP 8 Energy Targets

How much new capacity serves the free market?

As impressive as Vietnam’s renewable energy growth and targets are, the inevitable question remains just how much of the capacity receiving FIT are available for the growing corporate appetite for green power.

The long-anticipated DPPA was a much welcome market mechanism that aims to make newly built renewable energy projects more available for private entities with high electricity consumption, instead of all going to EVN under the FIT. Hence, it is no surprise that its implementation has infused new vigor into the solar market that has stalled since the end of the FIT. There is no doubt there is a willingness to build new projects, but how about the willingness to buy and sell under DPPA? It is one thing to subsidize new projects through state funds and another to ask these project owners to exit the 20-year guaranteed income and enter a volatile pricing framework.

.jpg)

Vietnamese government passed the "Direct Power Purchase Agreement" (DPPA) in July. (Photo: Vietnam's Ministry of Industry and Trade)

Take Taiwan’s renewable energy retail market for instance. Due to high FIT rates for solar, it would require even higher prices for project owners to leave the FIT regime. For buyers, electricity from generously subsidized projects is more difficult for smaller corporate buyers to purchase since project developers prefer to sell their product to companies with higher credit rating that help them obtain project loans from banks.

On the production side, it is also important that the Vietnamese government clarify on whether FIT project owners can break away from their PPA with EVN and participate as a supplier under DPPA. In Taiwan, project owners have the choice to return to the FIT system after trying out their luck in the free market. It remains to be seen whether this type of safety net measure will be implemented under DPPA.

Regarding renewable energy producers’ willingness to participate, a survey conducted by the Ministry of Industry and Trade (MOIT) of Vietnam revealed that about 24 renewable energy projects, with a total capacity of 1,773 MW, expressed interest in selling electricity through the DPPA mechanism. Additionally, 17 more projects, with a combined capacity of 2,836 MW, were considering joining. Either way, we know that these two groups represent only 10% and 16.6% of the total solar capacity, leaving much room for further release of renewable energy for the free market. But it is unclear whether these projects are subsidized projects. If they are projects that received FIT, then they are likely to have different costs entering the DPPA than new projects with no subsidies.

Meanwhile, the survey found that there are already 20 large consumers interested in a total direct power purchase of close to 1,000 MW. However, the solidification of these interests largely depends on the price that will be set by EVN for those participating DPPA via the national grid.

While it is still unclear the rates and transmission fees that will be decided by EVN, given that most projects were built receiving generous FIT rates, we expect that interested buyers could see PPA prices somewhere around USD 75 - 102/MWh[1] . Using this price range, it seems that compared to the conventional purchase of unbundled RECs perhaps the costs for PPA could be competitive for high voltage, peak hour power consumers. Multinational companies looking to source clean energy for their operations or invest in energy production can benefit from Vietnam’s abundant renewable resources. Solar has expanded and overreached the national target in just two years, which has become both an inspiration and cautionary tale for the country in the continuation of renewable energy development.

EVN’s recent expedited grid upgrade for the transmission between the central region to the north was a sanguine development for greater renewable energy access and stability. For enterprises eyeing to expand their operation in Vietnam, we offer the following recommendations:

- First, assess your demand for renewable energy and financial and human resource, then weigh them against each green power procurement mechanisms. DPPA can very well secure power for longer terms, but it is also far more complex to execute and requires market expertise.

- Second, without a clear price signal it is difficult to gauge how much capacity will be released into the free market under the DPPA mechanism. Relatedly, be prepared to see the price range for DPPA to bring changes to the unbundled renewable energy certificate market in Vietnam that has long enjoyed competitive market prices. Corporates should ready themselves of these changes and evaluate how their long-term energy strategy and cost structure will be affected.

The second part of this series will explore the promises and potential concerns of Vietnam’s latest mechanisms in enabling the development and utilization of renewable energy based on our first-hand information gather locally. In the meantime, please feel free to reach out to the author for any questions or discussion.

[1] This price range is a rough estimate, prices are also dependent on the contract length and the DPPA model the buyers enter.