The 2024 International Sustainable Energy Summit (ISES) in Kuala Lumpur, organized by PETRA and SEDA, gathers over 5,000 global participants to advance sustainable energy solutions. (Photo: ISES)

This article expands on the discussions from the International Sustainable Energy Summit (ISES) in Kuala Lumpur Malaysia from August 20 to 21, 2024, focusing on on Malaysia’s current status and future planning around grid modernization and new energy sources.

Grid modernization: Renewable energy utilization empowered by a stable and flexible grid

Variable renewable energy’s (VRE) nature presents challenges for grid stability. For Malaysia, electricity generation from VRE has seen the fastest growth in the past decade compared to that from dispatchable renewable energy and fossil fuels (Graph 1).

Graph 1. Electricity generation by energy sources (TWh)

As solar generation take up greater proportion in the energy mix to meet national renewable energy target, gird modernization becomes a necessity. While currently solar only made up 1.7% of Malaysia’s total electricity generation in 2023, the Malaysian government has designated solar to provide 35% of the energy generation in 2050. A boom in solar generation will assert great pressure on the grid. As can be seen from Vietnam’s frequent power outages last year, grid stability can be easily compromised in the events of hydropower generation shortfall due to a dry season or exception periodic electricity demand from the heat in the equatorial region.

Additionally, the Internation Energy Agency has identified 20% to 30% VRE penetration as the critical point of grid flexibility upgrade . In other words, the current 3 GW installed capacity may be within the grid capacity but as solar’s role increases in Malaysia’s power generation, it is necessary that the grid can adopt to the intermittent nature of solar.

Grid modernization can be looked at through two lenses: stability and flexibility. On increasing grid stability, battery storage has been highlighted on the panel as a crucial technology to provide grid stability and fully utilize solar generation. Just as Germany uses storage to leverage 60% of its solar, Southeast Asian countries like Malysia and Vietnam that are seeing unprecedented solar capacity growth can adopt the same grid ancillary services design.

On adding flexibility, demand response was brought up as a solution for consumers to help alleviate grid burden at peak hours. Likewise, as Malaysia opens up for third party access, the prospect of independent power producers to act as distributed energy resources (DERs) is added to the formula. But it is noted that for DERs to play a role in the grid, a transparent and efficient energy management system is of paramount significance. Several speakers stressed the importance of AI integration to interpret big data in the management of the distribution and transmission network. On this front, one of the guest speakers reflected on the difficulty in data collection and management in Malaysia at this stage.

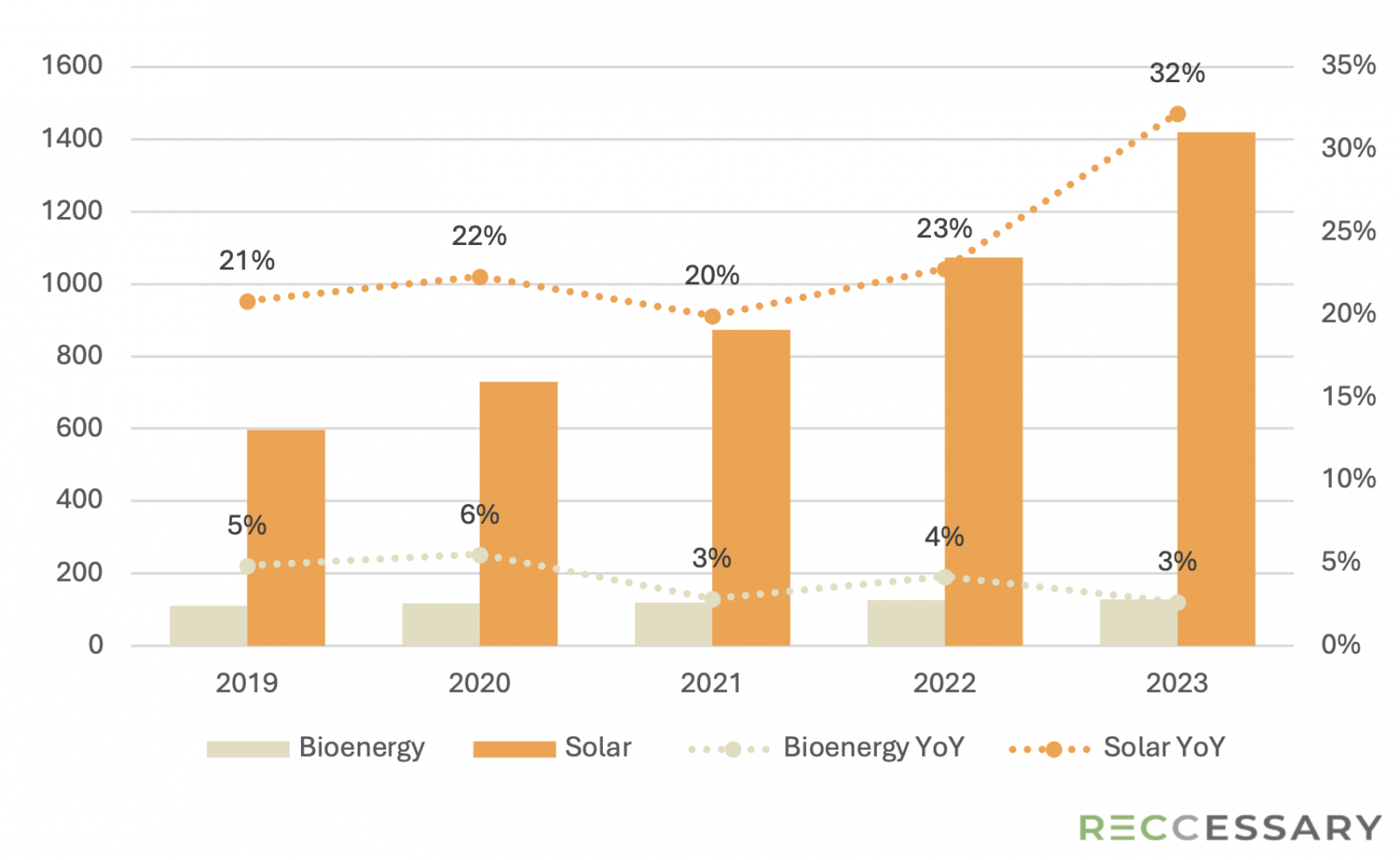

Is it bioenergy’s time to shine yet?

As the world's second-largest palm oil producer, Malaysia is working to convert industry waste into sustainable energy. (Photo: iStock)

Having the world’s second largest palm oil industry, Malaysia aims to tap into the potential of converting the residual wastes of the industry into sustainable energy. At the moment, bioenergy only makes up 3% of all renewable energy installed capacity and generation in the country. The reasons for this slow development is multifold.

On the regulatory side, historically bioenergy has been overshadowed by solar project programs like LSS. While the minimum feed-in tariffs (FIT) for biogas increased by 26% from 2022 to 2023 and remains at the new rate in 2024, biomass FIT did not adjust upwardly in the past five years.

|

| Solar (max) | Solar (min) | Biogas (max) | Biogas (min) | Biomass (max) | Biomass (min) |

| 2020 | 0.5413 | 0.3096 | 0.3184 | 0.2210 | 0.3085 | 0.2687 |

| 2021 | 0.4872 | 0.2632 | 0.3184 | 0.2210 | 0.3085 | 0.2687 |

| 2022 | 0.4385 | 0.2237 | 0.3184 | 0.2210 | 0.3085 | 0.235 |

| 2023 | 0.3947 | 0.1901 | 0.3184 | 0.2786 | 0.3085 | 0.2687 |

| 2024 | 0.3522 | 0.1616 | 0.3184 | 0.2786 | 0.3085 | 0.2687 |

Table 1. Historic maximum and minimum feed-in tariffs for solar, biogas, and biomass (MYR)

Furthermore, bioenergy production is not yet on par with the technological maturity of solar nor has it reach the economy of scale, but still has lower maximum tariff rates. Low bids that do not guarantee project completion but aim to secure FIT quota is another reason for the stalled development.

Graph 2. Year-on-year capacity growth: Bioenergy vs. solar

New energies

Energy diversification and management are crucial in achieving a successful energy transition. Going beyond renewable energy, public and private sectors are exploring the potential of green hydrogen and nuclear energy, which are also promising technology that balance grid instability from VRE.

Hydrogen has been placed at the center of Malaysia’s domestic energy diversification and energy export economy. The National Energy Transition Roadmap designated hydrogen as one of the six energy transition levers and for Sarawak, where hydropower is abundant, the energy utilities are actively exploring the business models for the development of green hydrogen.

Sarawak’s cheap hydropower is an attractive resource for the green hydrogen industry that has 60% to 80% of the production costs coming from electricity. But in the short term, ammonia will be produced first to be used in hard-to-abate sectors such as energy, steel, and shipping due to its relative advantage in storage and transportation compared to hydrogen.

The Bakun Hydroelectric Plant, located in central Sarawak. (Photo: Sarawak Energy)

Currently, the cost of green hydrogen can be six times as high as grey hydrogen and using CCUS with grey hydrogen also doubles the cost. So for green hydrogen to be commercially available, clearer policy framework is needed to finance the investment in the early stage. Regulatory support could be in the forms of grid transmission waiver, tax incentives, and auctioning mechanism for the consumers to help bridge the gap between subsidies and production costs.

As for nuclear energy, it is expected to become an energy source in Malaysia in the long term. That said, it is important that nuclear literacy starts now to provide the public with transparent and scientific information on the safety and sustainability issues around it. Related to grid stability, traditional large nuclear reactors have must-run capacity rates between 90%-100% that could add stress to the grid when renewable energy penetration is high. In this sense, small modular reactors (SMRs) become a more flexible energy source. But the challenge lies in the cost as the technology has not enter the commercial stage.

Opportunities and insights for investors in Malaysia’s renewables

Grid modernization is essential in releasing the potential of Malaysia’s renewable energy capacity. Without an adaptive grid for solar, the country could face serious renewable curtailment that have been found in other countries in past and present. At the same time, alternative energy sources that increase grid flexibility need to develop in tandem. Based on the panel discussions and exchanges with industry players at the ISES, we foresee the following in Malaysia’s energy transition:

1. Bioenergy

Power generation from bioenergy is expected to see greater development in the near future. But at the moment, renewable energy certificate (REC) traders have indicated that market demand for the energy source has been sluggish, with only one industry expert observing a small increase two months ago for reasons unknown.

- Recommendation for power consumers: In our view, bioenergy RECs may have a competitive price with state subsidies, but they are more suitable for consumers who are not obliged to strict greenhouse gas emission standards.

2. Nuclear

Nuclear is the long-term energy transition strategy while the green hydrogen industry is embarking on an exciting phase of international cooperations and public-private investments.

- Recommendation for investors: SDEC Energy[1] and Gentari both plan to apply green hydrogen first in transportation but currently Malaysia does not have a hydrogen vehicle industry yet, presenting immense business space for exploration.

The ISES assembled policy makers, industry experts, and scholars to enlighten on the promises and challenges in Malaysia’s energy transition. Reccessary has gathered first-hand insights with the delegates at the event. For companies eying the renewable energy sector in Malaysia, whether as an investor or a consumer, please don’t hesitate to reach out to us for the latest market development.

[1] SDEC Energy a wholly-owned subsidiary established by the Sarawak Economic Development Corporation in 2019. It is responsible for promoting Sarawak's hydrogen energy and its downstream retail business.