Palau boasts rich blue carbon resources and strong potential for wetland conservation. (Photo: Flickr/Holger Krupp CC BY-NC-SA 2.0)

The first part of the article highlighted the potential and pathways for overseas carbon credit development through successful cases in the Asia Pacific region. This second part shifts the focus to Taiwan’s diplomatic allies, exploring how businesses can engage in international climate action via carbon projects by looking at market trends and policies.

Compared with other markets, Taiwan’s allies provide an official cooperation framework that offers a more solid foundation for advancing Taiwan’s carbon diplomacy and fostering sustainable international partnerships.

Taiwan’s advantage in carbon diplomacy lies in its existing foreign aid foundations

Taiwan currently maintains diplomatic ties with twelve countries, primarily located in Central and South America and the Pacific Ocean. These nations offer favorable conditions for developing carbon projects, with abundant resources spanning forests, oceans, agriculture, and soil management.

With existing diplomatic foundations, Taiwan has the potential to build cooperation models that combine both market value and diplomatic significance by introducing technology and investment of private sector and advancing projects in line with international standards. For its diplomatic allies, this represents opportunities for resource integration and industrial upgrading, while for Taiwanese companies, it offers a pathway to overcome domestic regulatory barriers and expand into international markets.

Three key aspects to assess carbon market potential in Taiwan’s diplomatic allies

When evaluating carbon credit collaboration between Taiwan and its diplomatic allies, consideration should go beyond geopolitical and bilateral relations to include three key factors: price performance, project types, and regulatory cooperation.

1. Geographic distribution and price trends

According to data published by Ecosystem Marketplace, Oceania accounted for just 0.1% of global carbon credit trading volume in 2023, but prices in the region surged by 153%, the highest increase in the world (See Figure 1).

Figure 1. Distribution of global carbon market prices and trading volume[1]

This trend reflects that demand for high-quality carbon credits is increasing rapidly, particularly those tied to projects with co-benefits. For instance, blue carbon initiatives help protect marine ecosystems, forest conservation supports biodiversity, and sustainable agriculture creates local job opportunities and boosts economic development. Although the overall scale remains limited, carbon credits from these projects are highly valued by international buyers.

Central and South America, on the other hand, saw average carbon credit prices rising by 2% in the same year. Although the increase was modest, prices remained resilient despite downward trends in the global market. This stability can be attributed to the region’s well-established forest resources and community-based projects. Central and South America also account for 27% of global carbon credit trading, the second-largest share after Asia’s 31%, making it a key focus for the international carbon market.

2. Project types and carbon reduction potential

In terms of project structure, carbon credit development in Oceania is heavily concentrated in forest preservation, with 82.5% of its annual emissions reductions coming from reduced emissions from deforestation and forest degradation (REDD) projects (See Figure 2). However, REDD credits have remained at relatively low-price levels in recent years and have faced ongoing controversy, making it difficult for their market value to fully reflect their actual impact.

Therefore, the market is shifting toward new types of projects that emphasize clear co-benefits and nature-based solutions (NbS), such as blue carbon, ecotourism, and community-led conservation projects. Many island nations in Oceania are well-suited to develop small-scale, high-quality projects of this kind. Taking Palau for example, mangroves cover 10.5% of the nation’s land area, providing favorable conditions for blue carbon development.

Blue carbon credits traded on Singapore’s Climate Impact X (CIX) exchange reached USD 27.8 per ton in 2022, with 30% of bids as high as USD 35 per ton, reflecting strong international demand and buyers’ willingness to pay a premium for such projects.

In comparison, project structures in Central and South America are more diversified and offer greater potential for scaling up (See Figure 3). Annual emissions reduction in the region is projected to reach 240 million tons of CO2 equivalent, more than four times that of Oceania.

While REDD projects remain the primary focus, other categories such as afforestation, reforestation, and revegetation (ARR), as well as agricultural land management (ALM), also account for a significant share. This reflects not only the region’s abundant natural resources but also broader opportunities for companies to engage and collaborate.

3. Policy collaboration framework

In addition to market structure and project type, policy frameworks and bilateral cooperation mechanisms are also critical factors in determining whether companies can participate effectively. Most of Taiwan’s diplomatic allies have yet to establish comprehensive carbon registries or trading systems, creating opportunities for Taiwan to engage early in the planning stage and contribute to project design and implementation.

Moreover, Taiwan’s allies are generally open to foreign aid and technological collaboration. For example, many Pacific island nations rely heavily on support from countries like Australia and New Zealand. Taiwan has accumulated extensive experience in policy development and project implementation for greenhouse gas reduction over the past decade. Leveraging this foundation to jointly develop internationally certified projects with its allies would help strengthen bilateral influence and enhance Taiwan’s global reputation.

How can Taiwanese companies engage?

In this emerging market, businesses can play multiple roles beyond serving as funders. They may also act as project developers, technology providers, or platform integrators. Below are some potential strategies for engagement.

1. Technology export and project management

Taiwan holds competitive advantages in areas such as smart agriculture, water resource management, and ICT applications. Businesses can export mature technologies through project-based collaborations. For example, the smart agricultural technology services promoted by Taiwan’s Ministry of Agriculture can support allies in adopting data monitoring or tracking solutions.

2. Investment or co-development

Companies with sufficient capital and resources may consider co-developing projects with local NGOs or public-sector entities. This approach allows them to secure a share of carbon credits in advance and lock in future supply through long-term contracts. Common participants in such collaborations include individual project developers, development banks, and impact investors.

3. Participation in international platforms

Given the challenges of developing projects independently, businesses may join internationally led platforms, such as Japan’s Joint Crediting Mechanism (JCM). By participating as equipment providers, technology consultants, or supply chain partners, companies can reduce development risks and lower market entry barriers under the established frameworks.

Taiwan’s Ministry of Agriculture and Ministry of Foreign Affairs formed the “new smart agriculture advisory team” in March to strengthen cooperation with diplomatic allies on AI and digital technologies. (Photo: Ministry of Foreign Affairs)

Opportunities for public-private bilateral collaboration

Achieving carbon diplomacy requires not only participation from the private sector but also guidance from government agencies. Currently, Taiwan’s Ministry of Foreign Affairs is spearheading a plan to bring prosperity to its allies, helping lay an initial foundation across sectors such as agriculture, energy, and the environment. Looking ahead, these efforts could be expanded to include cooperation projects with tangible carbon credit benefits.

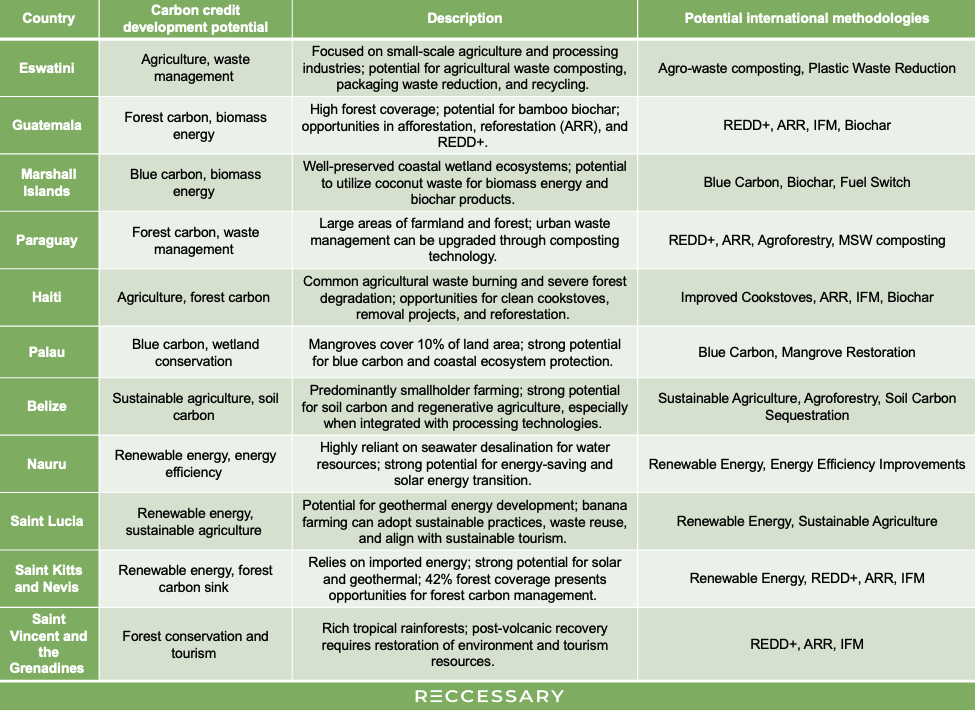

The table below summarizes potential carbon credit development opportunities among Taiwan’s diplomatic allies, based on demand assessments provided by the International Cooperation and Development Fund (ICDF).

Table 1. Carbon credit project potential in Taiwan’s diplomatic allies[4]

The table outlines potential international methodologies based on natural conditions, industrial structures, and national climate goals. It serves as an initial reference for companies evaluating carbon project opportunities. For example, Central and South American countries such a Guatemala, Paraguay, and Saint Vincent offer clear potential in forest and agricultural carbon sinks, while Pacific island nations like Palau, Tuvalu, and the Marshall Islands are well-positioned on blue carbon development.

Taiwan’s carbon diplomacy taking shape: Public-private collaboration needed

As Article 6.4 of the Paris Agreement prepares to usher in a new era for the global carbon market, carbon diplomacy is set to become a key frontier in international climate governance.

Taiwan’s Ministry of Environment has recently initiated plans to form an inter-ministerial working group with the Ministry of Foreign Affairs to advance discussions on “new energy and carbon markets,” with the goal of providing businesses with a clearer framework for participation.

In the global net-zero transition, the role of the private sector is critical — not only as practitioners of emissions reduction but also as potential pioneers in advancing Taiwan’s climate diplomacy. This offers a unique opportunity to achieve both sustainability goals and diplomatic gains.

[1] Source: Ecosystem Marketplace

[2] Source: Verra Registry

[3] Source: Verra Registry

[4] Compiled by Reccessary, with reference to Verra, Gold Standard, CDM, FAO, ICDF, and national climate policies.

.jpg)