.jpg)

(Photo: iStock)

As the global carbon market rapidly expands, carbon credits have evolved beyond an environmental issue into a strategic arena for both corporate investment and international diplomacy. For Taiwanese companies, where domestic carbon trading is still in its infancy and the policy framework under construction, developing carbon credit projects abroad may offer a forward-looking strategic pathway.

This report explores successful carbon diplomacy models in Japan, Singapore, and selected ASEAN countries, outlining practical opportunities and insights for Taiwanese businesses interested in entering the international carbon space.

Why carbon credit "development" outweighs "trading"

In the carbon market, development and trading represent supply and demand respectively. While Japan and Singapore are rapidly establishing themselves as regional trading hubs—such as Tokyo Carbon Exchange (TSE) and Climate Impact X (CIX)—Taiwan remains in early stages in terms of emissions regulation and market integration, limiting near-term international participation.

Instead, Taiwanese firms may find competitive advantage by engaging in overseas carbon credit development. This approach not only allows them to generate tradable credits, but also build practical expertise and technical capacity. Small and medium enterprises (SMEs) can participate through technical collaboration, project management, or international partnerships, thereby expanding overseas presence and building a sustainable brand image. Programs such as Taiwan’s MOFA "G-NEX Initiative" and TaiwanICDF’s "Impact Frontiers Program" are opening up new transnational participation channels for the private sector.

Participation is not limited to intergovernmental agreements; companies can also develop projects independently or through market mechanisms—even without formal Paris Agreement obligations.

Asia-Pacific case studies: Japan, Singapore, ASEAN

1. Japan: JCM bilateral cooperation model

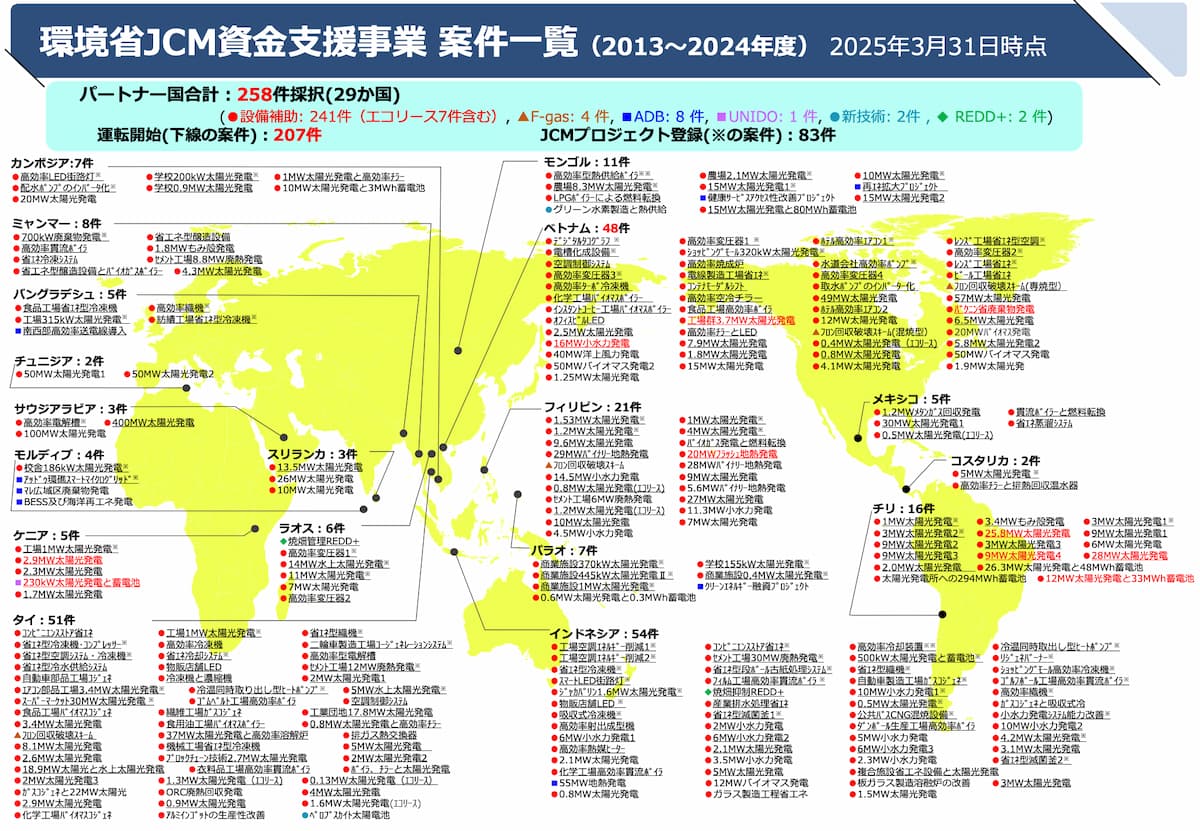

Launched in 2013, Japan’s Joint Crediting Mechanism (JCM) is a flagship model for carbon credit diplomacy. Under JCM, Japan signs bilateral agreements with developing countries, enabling Japanese companies to implement local emission reduction projects and convert those reductions into credits to fulfill Japan’s NDC commitments. As of March 2025, JCM spans 29 countries across Southeast Asia and Latin America.

Figure 1. Distribution of signatory countries and carbon reduction projects under Japan’s JCM mechanism[1]

In ASEAN alone, JCM projects account for 63% of total reductions[2]. Notable project types include energy efficiency, renewables, forest conservation, and transport infrastructure.

One example is a 2015 project to enhance grid efficiency in southern Vietnam. Local firm THIBIDI manufactured transformers, while Japanese firm Yuko Keiso provided advanced amorphous metal technologies. The project cut energy losses by 33% and reduced CO2 emissions by 3,885 tonnes annually, later expanding to Laos and scaling up sevenfold within three years.

Key JCM advantages include:

-

Cost-effective emission reductions: Japan’s high environmental standards and tech maturity[3] raise its marginal abatement costs; outsourcing cuts costs.

-

Sustainable tech transfer: Japanese capital, tech, and project management help developing nations build long-term low-carbon infrastructure.

-

Commitment clarity: Clear bilateral frameworks ensure emission reductions are equitably allocated and aligned with climate goals.

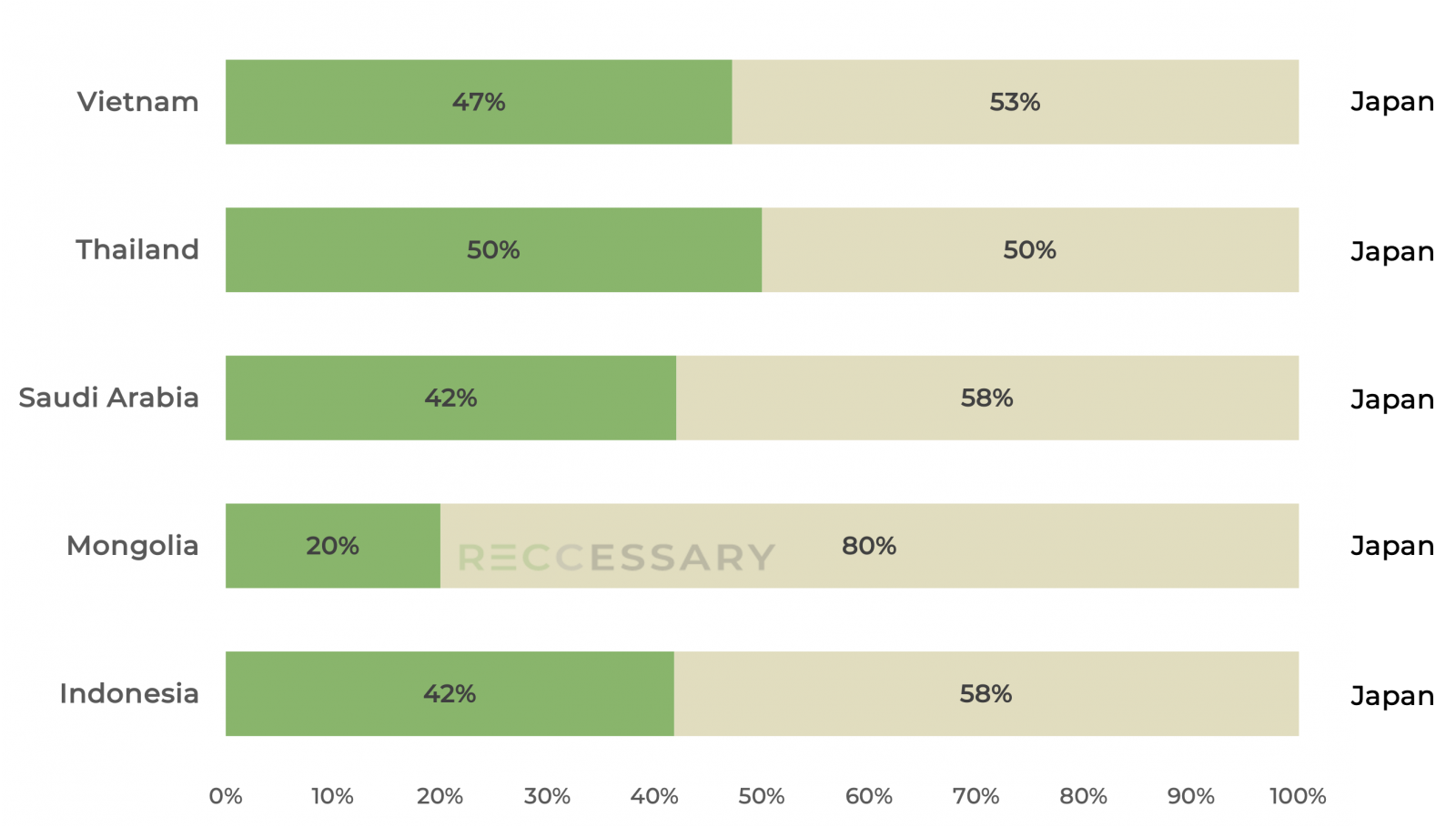

Figure 2. Allocation of carbon credits among the top five JCM partner countries[4]

2. Singapore: Emerging hub for regional carbon trade

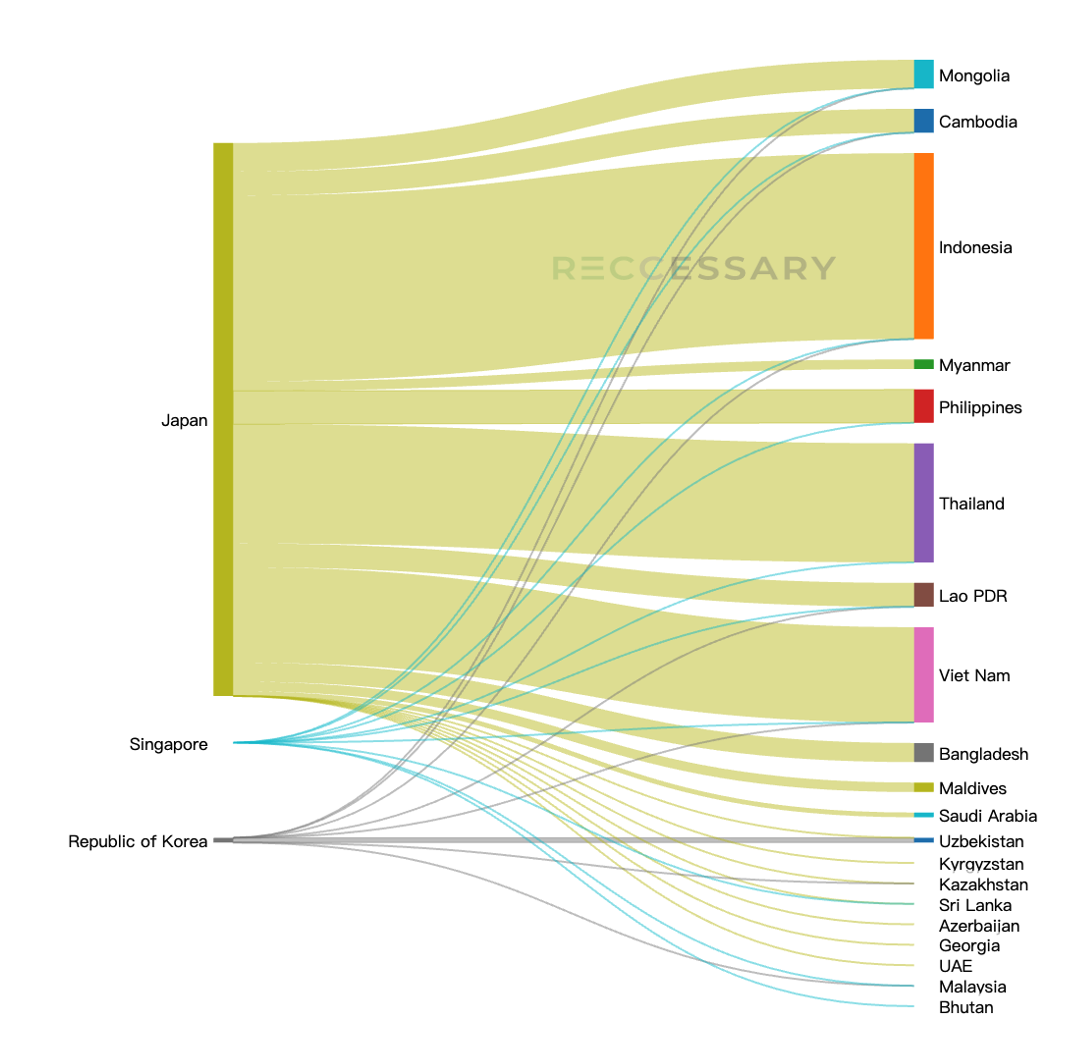

Singapore has positioned itself as an ASEAN carbon hub through the launch of exchanges like ACX and CIX. However, constrained by limited natural resources, the country has pivoted toward international carbon credit development.

By March 2025, Singapore has signed bilateral agreements with Bhutan, Ghana, and others—demonstrating how carbon trading supports broader diplomatic strategy. With Taiwan facing similar domestic limitations, partnerships with friendly nations abroad may offer practical entry points.

Figure 3. Status of bilateral agreements under the Paris Agreement across Asia[5]

3. ASEAN: Resource-rich hotspot for carbon credit development

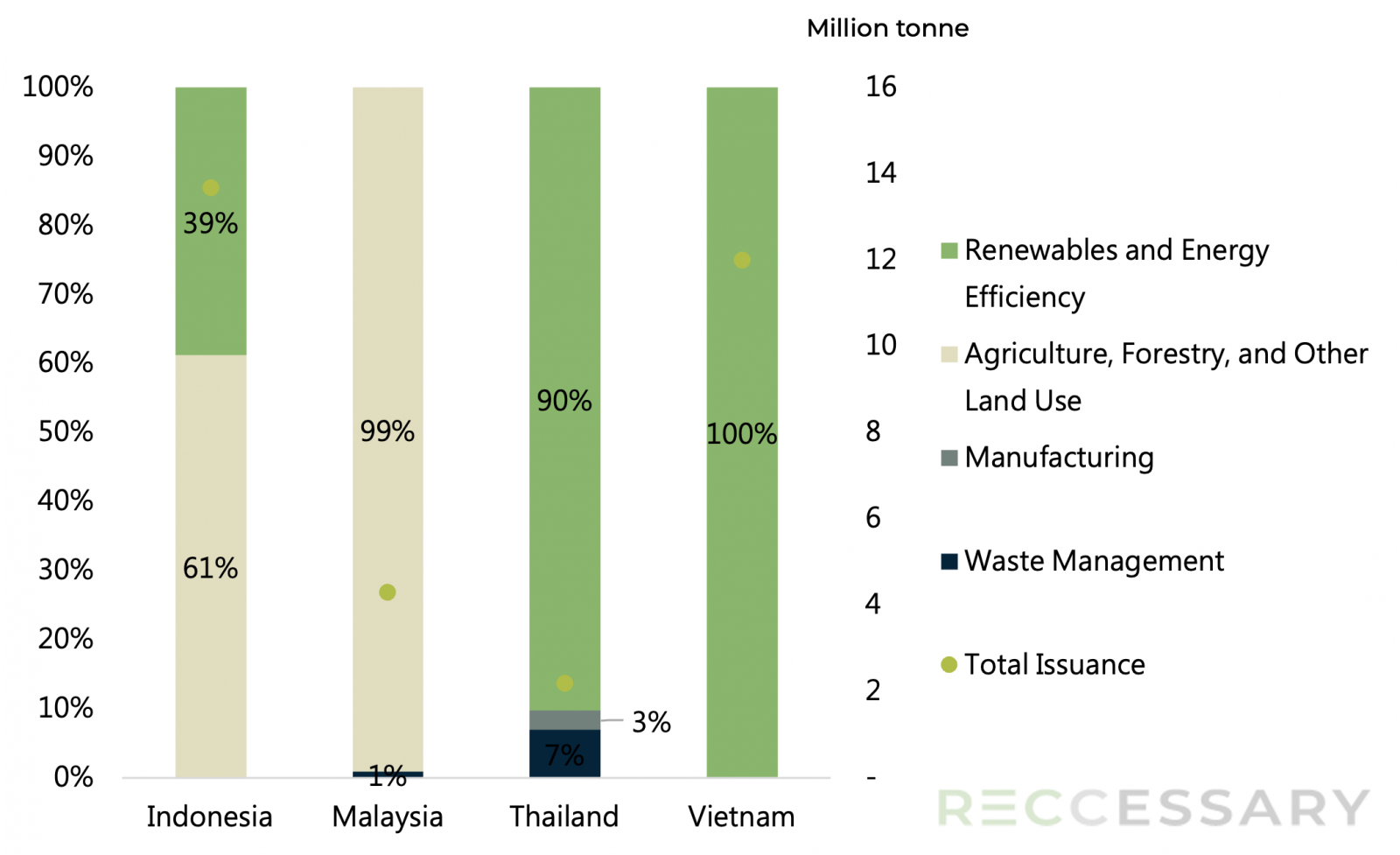

Southeast Asia’s abundant natural assets offer strong foundations for nature-based carbon solutions. According to Verra, between 2022 and 2024, Indonesia, Malaysia, Thailand, and Vietnam issued over 32 million tons in carbon credits—mainly from forestry, land-use, and renewable projects.

Figure 4. Carbon credit issuance by representative ASEAN countries, 2022–2024[6]

Each country tailors its development strategy:

-

Indonesia: Focuses on REDD+ and afforestation due to its tropical forest assets. The government is aggressively attracting international investment.

-

Vietnam: With rapid solar and wind growth, most projects are renewable energy-based.

-

Malaysia: Has the highest forest coverage in ASEAN but faces high deforestation rates, making forest-based credits a government priority.

Understanding each market’s development focus is essential for any business entering the ASEAN region.

Risks and challenges to watch

Despite opportunities, Taiwanese firms must remain vigilant of key risks:

-

Policy uncertainty: Many host nations are still forming carbon regulations, risking changes in oversight or eligibility. Legal and operational support is critical.

-

Carbon price volatility: Credit prices vary by project type, quality, cost, and exchange platform. Firms should assess long-term ROI before committing.

-

Sociocultural sensitivities: Projects often operate in developing regions with complex land use and community dynamics. Mutual respect and stakeholder engagement are vital to avoid conflict.

Carbon development as economic diplomacy

Carbon credits are no longer just environmental tools—they are instruments of international cooperation and economic diplomacy. Asia-Pacific’s evolving markets show that supply-side engagement offers not just revenue streams, but also reputational leverage.

For Taiwanese firms, proactively developing overseas projects may be more strategic than passively awaiting domestic market maturity. Early participation builds competitive advantages and aligns companies with global climate leadership.

In our next feature, RECCESSARY will explore carbon development opportunities in Taiwan’s diplomatic allies, offering insights to help companies map tailored pathways toward sustainable global impact.

[1] Source: Global Environment Centre Foundation

[2] Based on the volume of carbon credits issued

[3] Technological upgrades can raise the capital and technical barriers for emission reduction in a country or sector, including advanced R&D, equipment modernization, and organizational low-carbon transition

[4] Source: Official website of Japan's JCM

[5] Source: UNEPCCC, data as of April 2025

[6] Source: Verra