(Photo: iStock)

As climate action accelerates globally, carbon pricing has become a central instrument for countries seeking to achieve net-zero emissions. In 2025, carbon markets worldwide are exhibiting distinct regional trends—while the EU continues refining its policy tools, China consolidates its role as a leader among emerging markets, and Southeast Asia lays the groundwork for cross-border carbon credit cooperation. These developments reflect a diversified global approach to decarbonization and energy transition.

RECCESSARY’s upcoming annual report Renewable Energy in Southeast Asia and Global Carbon Market Trends: 2024 Recap & 2025 Outlook will analyze these key dynamics in 2025 and provide a retrospective of policy progress over the past year, equipping companies and investors with forward-looking insights.

Performance review: Three leading carbon markets—EU, China, and South Korea

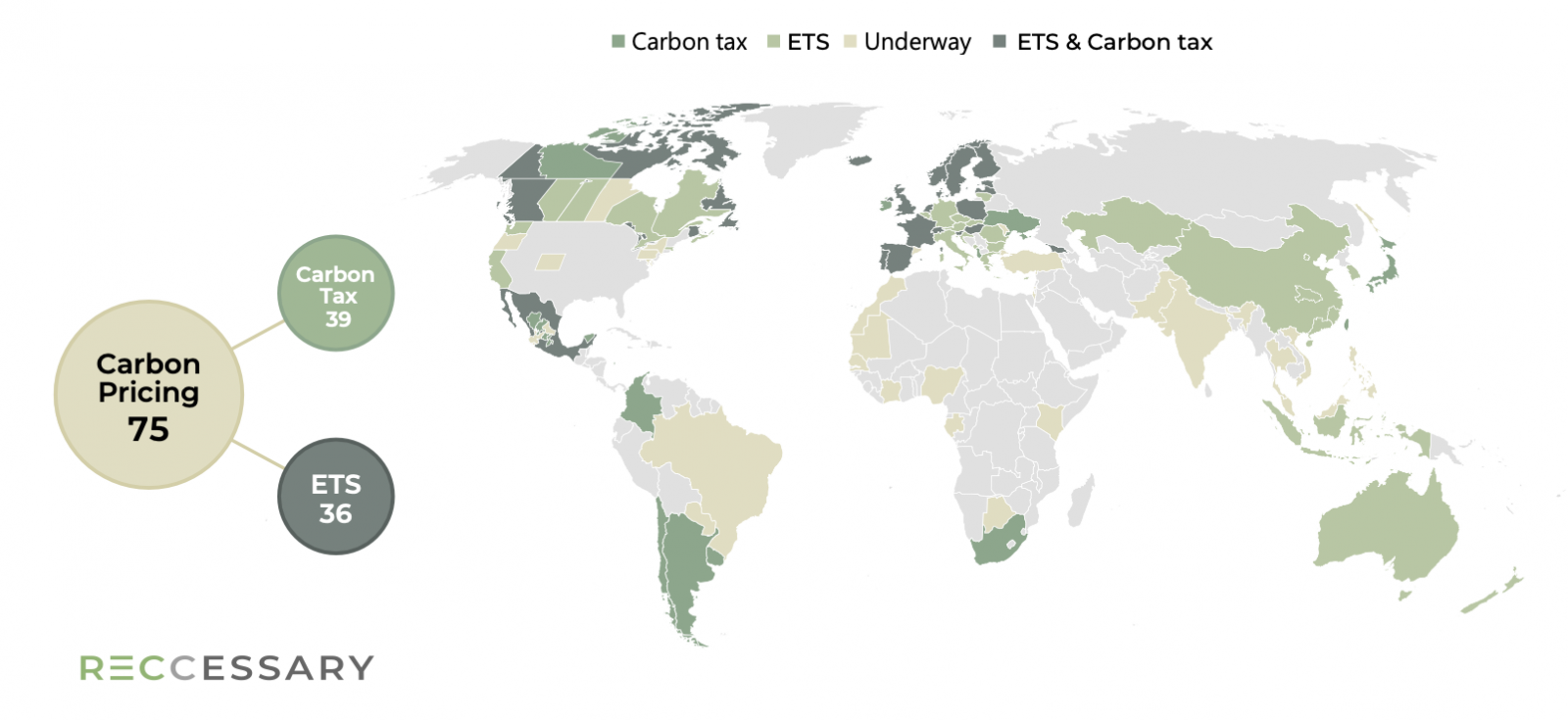

As of 2024, 36 countries or regions have implemented Emissions Trading Systems (ETS), covering around 18% of global greenhouse gas emissions. The following summarizes the carbon market performance of the EU, China, and South Korea.

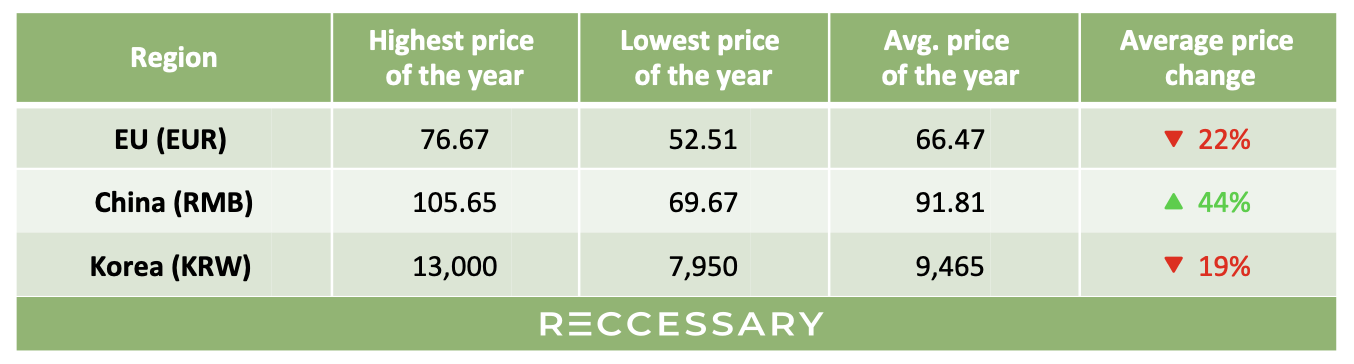

Table 1. Carbon price trends in major global markets, 2024

European Union: Tightened supply, weak demand—Prices hit 3-year low

The EU ETS remains the world’s most mature carbon market, covering approximately 45% of the bloc’s emissions. In 2024, key developments included allocation cuts and the inclusion of the maritime sector. However, carbon prices fluctuated due to weak demand and oversupply. The extension of the compliance deadline to September 30 led to reduced procurement in the first half of the year, causing prices to drop to €52/ton in February. Despite a rebound later in the year, the annual average price still declined by 22% compared to 2023.

Looking ahead, the EU is expected to further reduce free allowances and advance discussions on ETS 2. These measures could support price recovery. Nevertheless, pressure from energy-intensive sectors and the price spillover from the Carbon Border Adjustment Mechanism (CBAM) will remain key influencing factors.

China: Policy push fuels demand, carbon price hits record high

From 2025 onward, China will expand its national carbon market to include the steel, cement, and electrolytic aluminum sectors, covering about 60% of total national emissions. In 2024, the average price of China Emission Allowances (CEA) rose to RMB 91.81/ton—an increase of 44% year-on-year—marking the highest level since market inception. The expansion of regulated sectors drove compliance demand, with prices exceeding RMB 100/ton by year-end.

Market activity increased significantly in 2024, as China entered the fourth year of national ETS operations. Future efforts will focus on optimizing allowance allocation and strengthening compliance oversight.

South Korea: Oversupply continues, market reform in progress

South Korea's K-ETS is East Asia’s first carbon market, covering nearly 89% of national emissions. In 2024, prices remained sluggish, averaging KRW 9,465/ton—a 19% decline from the previous year—primarily due to oversupply and weak demand.

Despite reform measures such as easing allowance carryover restrictions and enabling financial institution participation, liquidity remains limited. Looking ahead to 2025, Korea plans to introduce new financial instruments like exchange-traded notes (ETNs) and carbon futures. The government is also intensifying bilateral cooperation under Article 6.2 of the Paris Agreement to strengthen international market ties.

Key carbon market themes for 2025: Legislative trends in the EU, U.S., and Southeast Asia

Since the Paris Agreement in 2015, countries have pursued ambitious climate goals through carbon pricing and trading mechanisms. RECCESSARY has tracked global developments and identified 2025’s critical themes and legislative milestones to guide corporate and investor strategy.

Figure 1. Global carbon pricing implementation regions, 2024

EU and U.S.: Global climate influence remains strong

In the US, political uncertainty loomed over 2024 climate policy. While the Inflation Reduction Act (IRA) continued to fund clean energy, the absence of a national ETS limits the US’s ability to compete with the EU. At the state level, Washington’s ETS faced backlash for its impact on fuel prices, sparking debate on balancing cost and climate action.

Meanwhile, the EU’s CBAM advanced further, imposing price pressure on imports and encouraging other countries to adopt carbon pricing. This spillover effect is expected to be a major driver of global carbon policy in 2025. Overall, the EU continues to lead in regulatory rigor, while uncertainty in the US may hinder its influence.

Southeast Asia: A rising carbon market hotspot

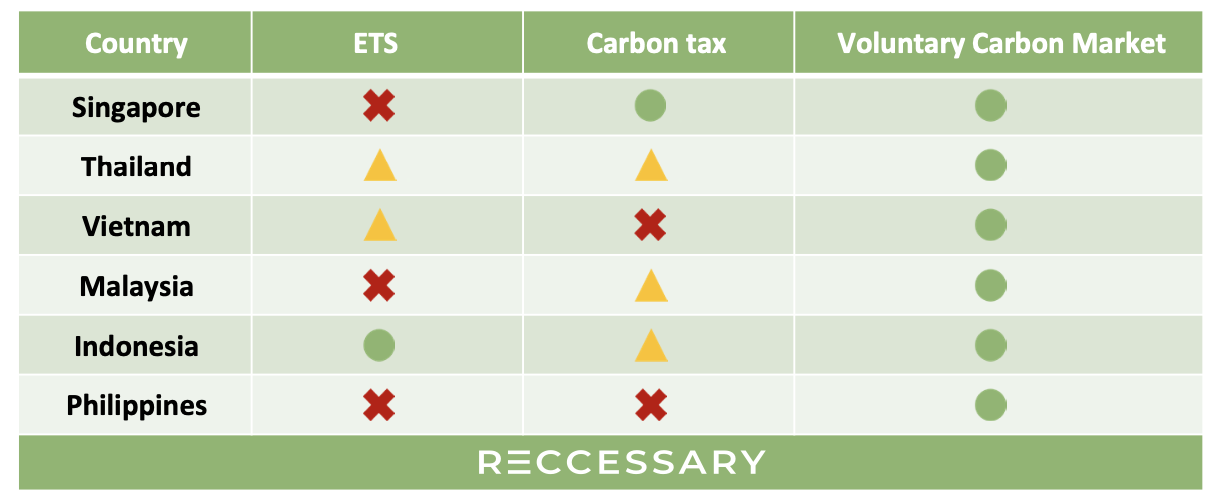

Table 2. Overview of carbon pricing policy progress in Southeast Asia, 2025

Compared to Western markets, Southeast Asia’s carbon policy landscape is still taking shape. Despite varying levels of progress, countries are actively positioning themselves as carbon trading hubs within ASEAN. Key developments include:

Thailand

-

Operationalizes the T-VER voluntary offset program, with growing interest in blue carbon projects.

-

Plans to implement a carbon tax of THB 200/ton by 2025, though the low price may limit long-term impact.

-

Carbon credit issuance is growing, with trading facilitated by TGO and other platforms.

Malaysia

-

Strengthening market presence through domestic credit auctions, though liquidity remains a challenge.

-

The second auction included high-quality, locally developed forest management credits.

-

A carbon tax is expected in 2026 to align with CBAM and boost ETS development.

Vietnam

-

Pilot phase of ETS scheduled for 2025, starting with the steel and cement sectors.

-

A proposed increase in offset usage to 20% raises concerns about mitigation integrity.

-

Progress is hampered by incomplete regulations, especially in monitoring and verification.

Indonesia

-

Expands ETS coverage in 2025 to include gas-fired power and smaller coal plants.

-

Carbon tax implementation has been delayed; the pricing framework needs improvement.

-

IDX Carbon Exchange opens to foreign investors and introduces new projects to diversify offerings.

These advances reflect Southeast Asia’s growing role in global carbon trading. The success of these policies will depend on timely implementation and real market outcomes.

Paris Agreement Article 6.4 launch to reshape carbon markets in 2025

With the operationalization of Article 6.4 of the Paris Agreement, 2025 is set to usher in a new era of global carbon trading. The EU’s pricing and regulatory influence will continue to shape market behavior, while China and Korea focus on increasing liquidity and oversight. Southeast Asia will see greater opportunities—and challenges—in cross-border trading and domestic carbon taxation.

Looking forward, the global carbon market will prioritize alignment with international standards and enhanced transparency. Governments and businesses must strike a balance between technological innovation and policy coordination to achieve net-zero goals while seizing opportunities in the green economy.