ASEAN-6 is advancing its renewable energy transition amid rapid economic growth, with a 5.2% average GDP rise in 2024. (Photo: iStock)

As Southeast Asia's economic growth accelerates, driven by its emergence as a manufacturing hub amid global geopolitical shifts, the development of renewable energy in the region is increasingly vital. The ASEAN-6 nations—Indonesia, Thailand, Singapore, Vietnam, Malaysia, and the Philippines—are at the forefront of this transition, balancing economic expansion with the pressing need for energy decarbonization.

RECCESSARY is set to launch an annual report on trends in ASEAN's green energy market, focusing on key developments in 2025. The report will also review policy progress over the past year, providing businesses and investors with insights into the latest market trends.

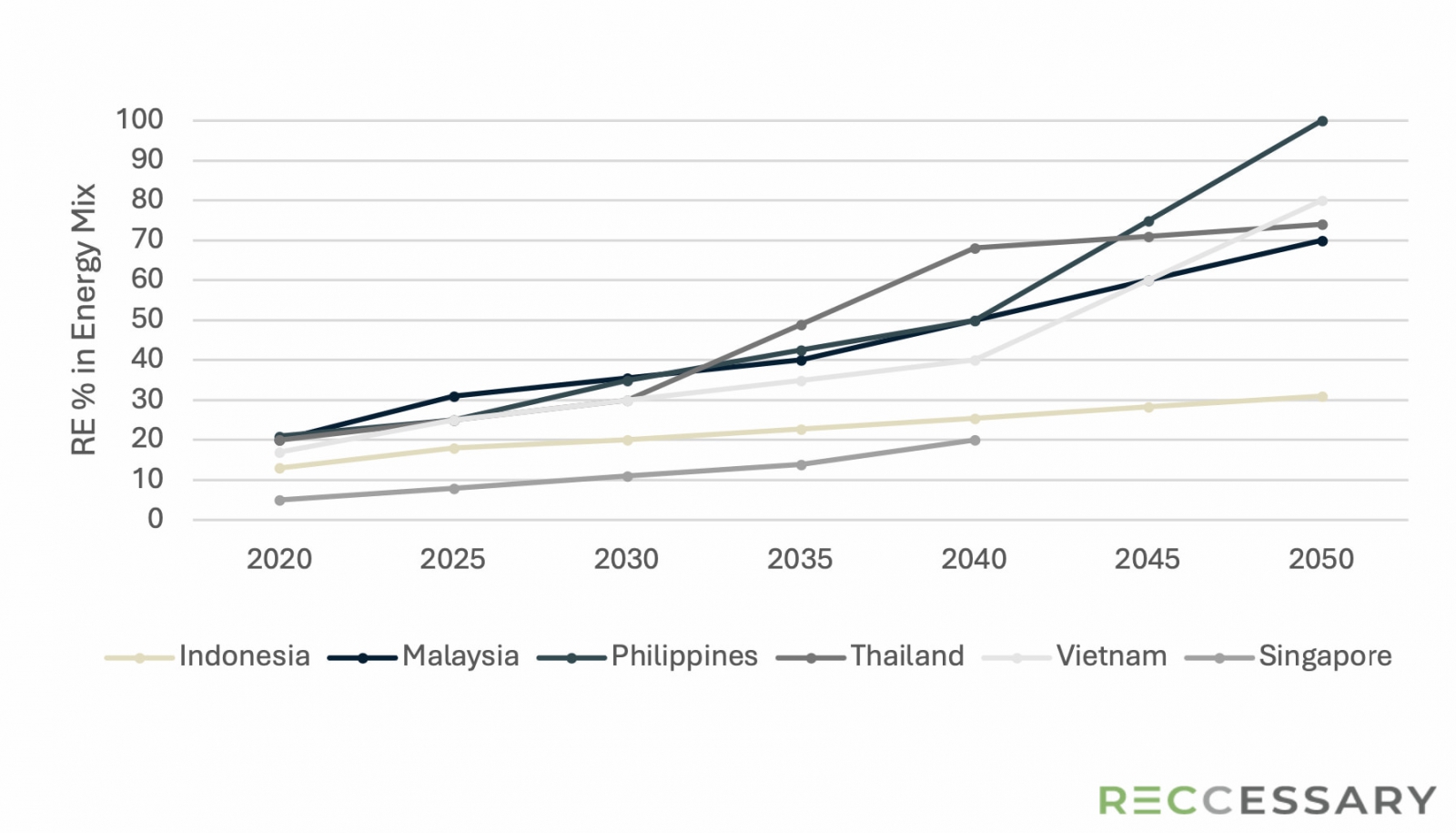

In 2024, ASEAN-6 countries experienced robust economic growth, with an average GDP increase of 5.2% by the third quarter. This growth has amplified energy demand, highlighting the urgency of renewable energy adoption to meet both economic needs and carbon reduction goals. Despite ambitious targets (Figure 1), the region faces numerous challenges, including entrenched reliance on fossil fuels, inadequate grid infrastructure, and regulatory ambiguities. These factors hinder the rapid deployment of renewables, with new fossil fuel plants offsetting the emissions avoided by renewable projects.

Figure 1. ASEAN-6 renewable energy targets

Vietnam: A regional leader in renewable energy

Vietnam has become a dynamic player in Southeast Asia's renewable energy landscape. In 2024, the implementation of the National Power Development Plan VIII (PDP8) set ambitious targets, aiming for a 30% renewable energy share by 2030 and net-zero emissions by 2050. This translated into substantial growth in solar and wind energy, with solar capacity reaching 17 GW and wind energy nearing 6 GW.

However, grid infrastructure constraints and regulatory uncertainties remain significant challenges. The country's transmission network struggles to accommodate the rapid growth of intermittent renewable sources, leading to frequent curtailments. Looking ahead to 2025, Vietnam plans to address these issues through grid modernization and energy storage solutions. Offshore wind, with a potential of 160 GW, is a key area of focus, supported by new investment-friendly policies.

.jpg)

Vietnam is driving renewable growth with PDP8, targeting 30% renewables by 2030. (Photo: EVN)

Thailand: Expanding policies, slow growth

Thailand’s renewable energy progress in 2024 was shaped by the draft Power Development Plan for 2024-2037 (PDP 2024), which raised the renewable energy target to 51% of the energy mix by 2037. Despite supportive mechanisms like feed-in tariffs (FIT) and direct power purchase agreements (DPPA), the country’s solar and wind capacities grew at a slower pace than expected due to insufficient monetary incentives and policy limitations.

In 2025, Thailand aims to accelerate growth through revised policies, expanded FIT quotas, and new capacity installations under the DPPA framework. Finalizing the PDP 2024 will be critical to achieving these goals and ensuring sustainable energy development.

Philippines: Leveraging natural resources

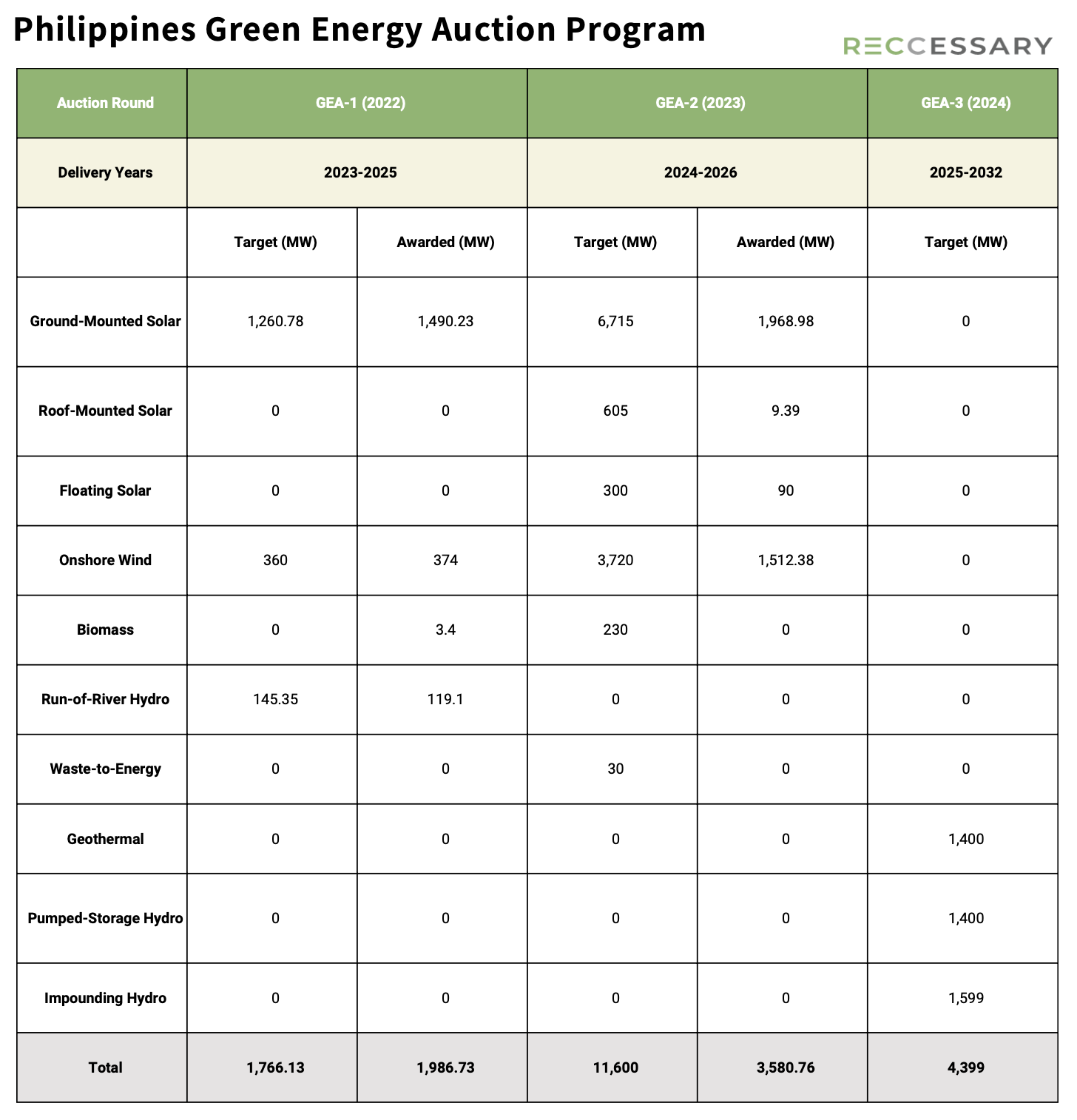

The Philippines capitalized on its abundant natural resources in 2024, with renewable energy accounting for 29% of its installed capacity. Key developments included the Green Energy Auction Program (GEAP), which allocated over 11 GW of capacity to solar, wind, and waste-to-energy projects, and the removal of foreign ownership restrictions in renewable energy projects.

Table 1. Philippines Green Energy Auction Program (GEAP)

Despite these advancements, grid bottlenecks and regulatory inefficiencies pose significant challenges. The government’s focus in 2025 will be on enhancing grid reliability, streamlining permitting processes, and expanding auction programs. The Energy Virtual One-Stop Shop (EVOSS) is expected to simplify project implementation, attracting greater investments.

Read more: Taiwan plans to import Philippine green energy: What are the potentials and obstacles?

Malaysia: Bridging the gap to 2025 targets

Malaysia made notable progress in 2024, with renewable energy reaching 24.3% of its capacity mix (Figure 2). Solar energy was a key driver, supported by programs like Large-Scale Solar (LSS5) and Net Energy Metering (NEM). Additionally, the Green Electricity Tariff (GET) and cross-border trade initiatives, such as Energy Exchange Malaysia (ENEGEM), bolstered renewable energy development.

.jpg)

Figure 2. Malaysia’s capacity mix (2023)

However, challenges like grid capacity constraints and insufficient incentives for bioenergy persisted. In 2025, Malaysia aims to focus on energy storage solutions, rural electrification, and large hydropower projects, alongside expanding solar capacity through policy enhancements.

Indonesia: Ambitious targets amid structural challenges

Indonesia, Southeast Asia’s largest economy, faced mixed progress in 2024. While policy reforms like the draft New Energy and Renewable Energy (EBET) Bill showed promise, renewable energy investments, particularly in solar, remained limited. The country’s reliance on fossil fuels and grid connectivity issues further hindered progress.

In 2025, Indonesia is set to focus on solar and geothermal energy, leveraging international partnerships to overcome infrastructure bottlenecks. The rooftop solar quota and additional geothermal site tenders will play crucial roles in achieving the country’s renewable energy targets.

Read more: Japan's Inpex plans to double geothermal power capacity in Indonesia

Muara Laboh geothermal power plant in West Sumatra. (Photo: ESDM)

Singapore: Innovating within constraints

Singapore demonstrated remarkable progress in 2024, driven by policy initiatives and regional cooperation. The SolarNova program propelled solar capacity to over 1.3 GWp (Figure 3), and cross-border energy trading under the Lao PDR-Thailand-Malaysia-Singapore Power Integration Project (LTMS-PIP) enhanced energy security.

.jpg)

Figure 3. Solar PV installation by consumer type

Challenges such as land scarcity and reliance on natural gas persist. In 2025, Singapore plans to expand its solar capacity, develop energy storage systems, and deepen regional energy collaborations. Floating solar farms and hydrogen strategy advancements will further support its transition to a low-carbon economy.

Regional trends and outlook for 2025

The ASEAN-6 countries have set ambitious renewable energy targets, aiming to reduce their reliance on fossil fuels while meeting growing energy demands. Policies like DPPAs, FIT schemes, and green energy tariffs are creating opportunities for private-sector investments. However, achieving these targets requires addressing critical challenges such as grid modernization, regulatory clarity, and financial incentives.

Regional initiatives, such as the ASEAN Power Grid and cross-border energy trade agreements, are playing a pivotal role in enhancing energy security and resource optimization. These collaborations are expected to expand in 2025, fostering technology transfer, competitive pricing, and greater integration of renewable energy sources.

Technological innovations, including energy storage systems, floating solar farms, and smart grids, are essential for overcoming land and infrastructure constraints. Investments in these technologies will be crucial for scaling up renewable energy capacity across the region.

ASEAN-6 gears up for greener future

The ASEAN-6 nations are making significant strides in renewable energy development, reflecting their commitment to sustainable growth amid rapid economic expansion. While challenges such as policy ambiguities, grid constraints, and reliance on fossil fuels persist, the outlook for 2025 is promising.

By leveraging regional cooperation, innovative technologies, and supportive policies, these countries are well-positioned to accelerate their transition to a low-carbon future. For businesses and investors, understanding the evolving dynamics of each market will be key to navigating opportunities in this vibrant and rapidly growing sector.