.jpg)

The Philippine Energy Plan aims for a 50% renewable energy share by 2040, a seven-fold increase from 2023 levels. (Photo: iStock)

In recent days Taiwan’s Economic Affairs Minister Kuo Jyh-huei (郭智輝) publicly proposed a plan to import renewable energy from the Philippines to meet Taiwan’s domestic demand, sparking heated discussions on the idea’s feasibility. Many are doubtful about the costs of imported energy being lower than local production taking into consideration the construction of a 300-kilometer long submarine cable.

But apart from costs, power stability and the Philippines’ domestic demand are also important things to consider. To gain a more comprehensive understanding of this discussion, this article will introduce the Philippines’ renewable energy development and market dynamics.

The upsides and challenges of renewable energy development in the Philippines

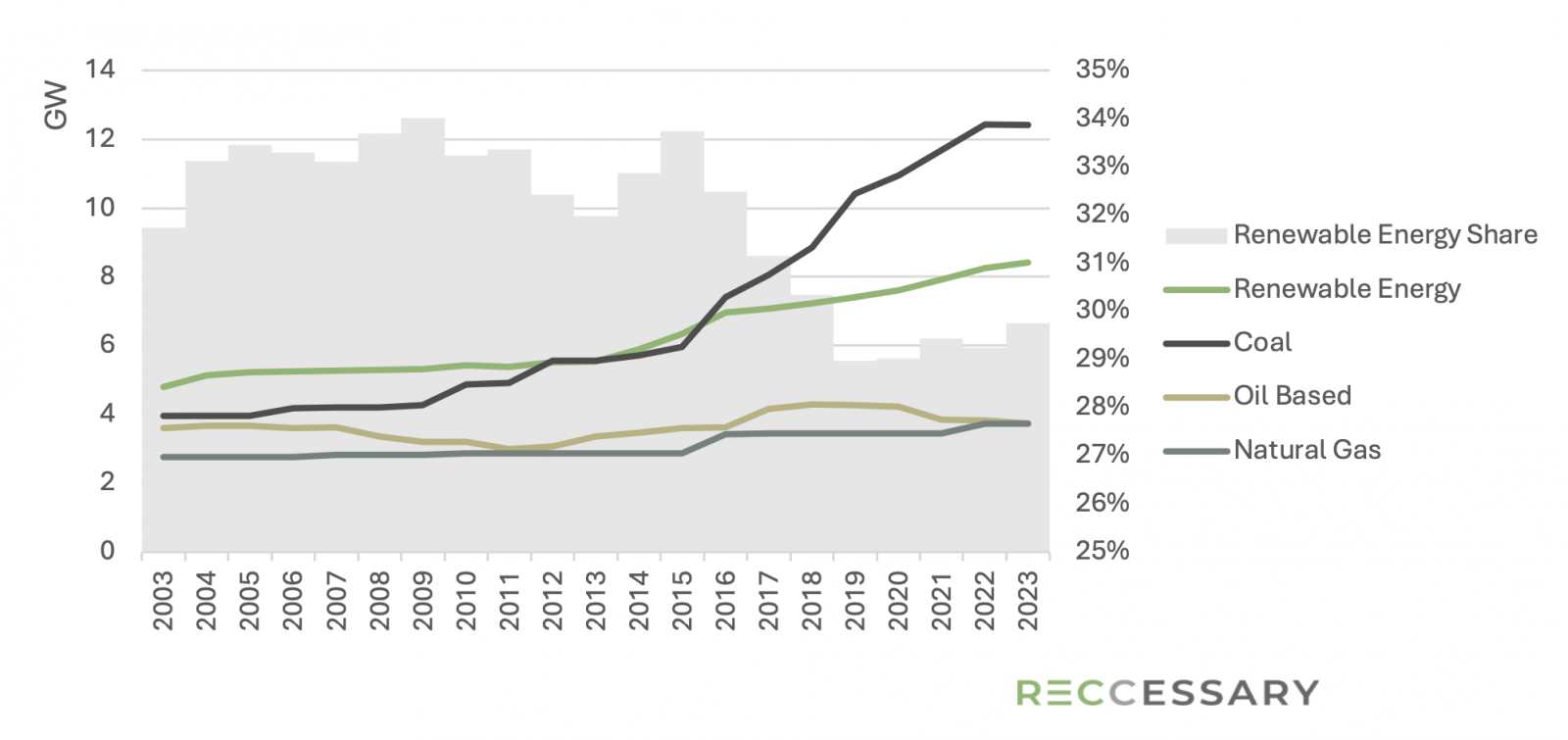

Renewable energy capacity composed 29.4% of total installed power capacity in the Philippines in 2023. Graph 1 shows that prior to 2012 renewable energy capacity has remained constant and notable growth was stipulated under feed-in tariff (FIT) between 2013 and 2017.

But after the oversubscription and uncoordinated expansion of renewables under the FIT, the scheme has been suspended and new installed renewable capacity continues but at much slower rates. Coal capacity, on the other hand, was once overtaken by renewables 2014 and 2015 but began to surge ever since, eclipsing renewable energy’s share in the energy mix.

Yet according to the Philippine Energy Plan (2023-2050), the country will reach 35% renewable energy share by 2030 and 50% by 2040, or a seven-fold increase of renewable energy capacity in 2040 compared to 2023 level.

Graph 1. Installed Capacity and Renewable Energy Share (2003-2023)

Renewable Portfolio Standard (RPS)

In order to achieve the targets, a number of policies are put in place, making the Philippines one of the most progressive countries in the region in promoting renewable energy growth. One particular policy is the Renewable Portfolio Standards (RPS) policy, which requires electricity suppliers to purchase a minimum percentage of renewable energy electricity.

In 2022, the mandated renewable energy portion under the RPS has increased from 1% annual increment to 2.52% starting in 2023. In the same year, the country also removed investment restrictions on renewable energy projects to allow 100% foreign ownership, courting global private capitals for the country’s renewable energy ambition.

Green Energy Auction Program (GEAP)

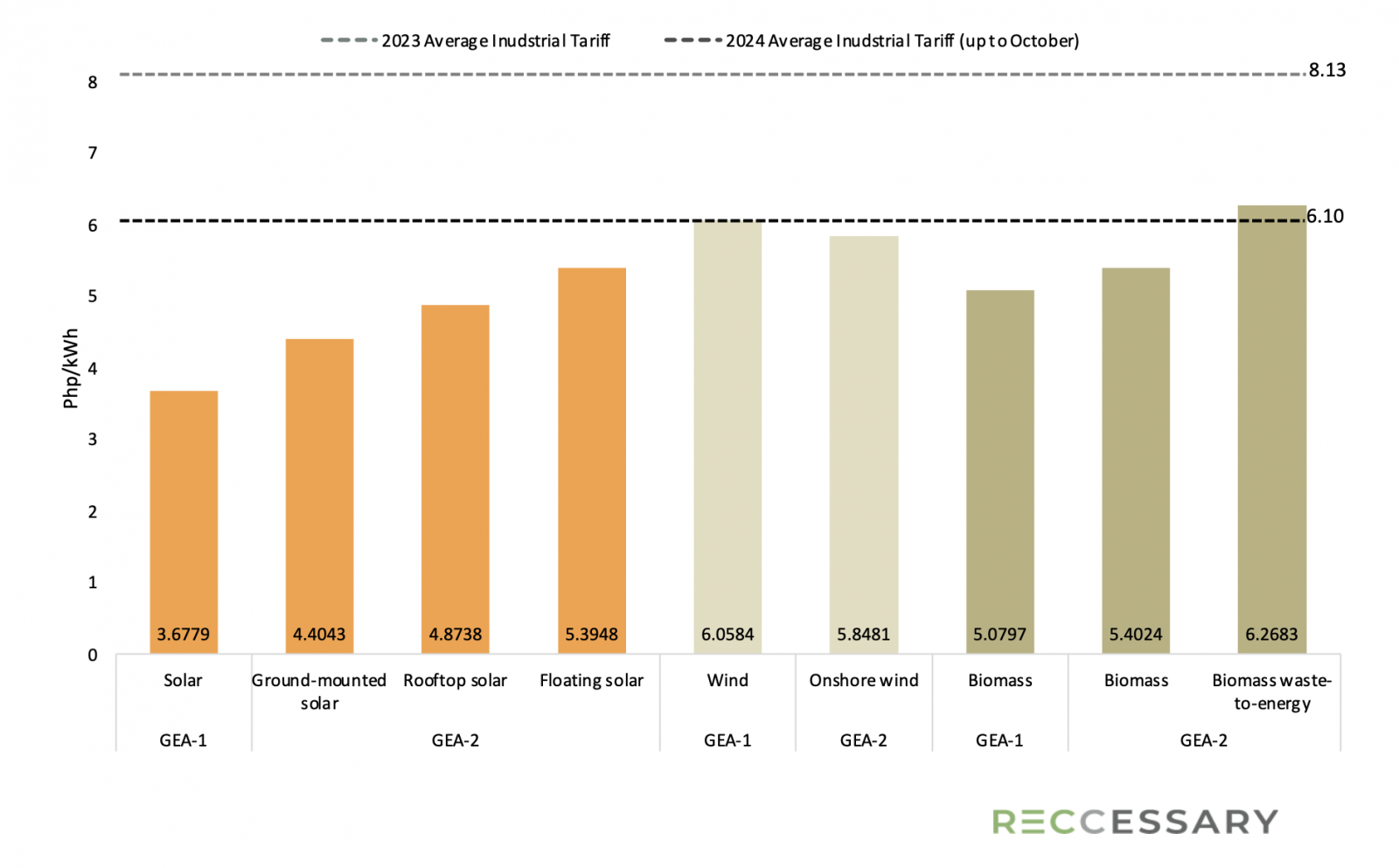

Supplementing the RPS, renewable energy auction was put in place to help suppliers achieve their renewable energy goals. The Green Energy Auction Program (GEAP) started in 2022 has thus far awarded 5.4 GW of renewable energy capacity with delivery year up to 2026.

However, as can be seen from the table below, the subscription rate dropped significantly in the second round. This is mainly due to investor uncertainties on transmission availability and waste supply availability for biomass and waste-to-energy technologies. GEA-2’s undersubscription was also attributed to the unrealistic ceiling prices to recover construction costs as reported by developers. Delays in grid impact study were also stated as another factor for the underperformance of GEA-2.

In GEA-3, only dispatchable renewable energy sources will be awarded capacity, indicating the government’s intention to minimize grid burden.

| Auction Round | GEA-1 (2022) | GEA-2 (2023) | GEA-3 (2024) | ||

| Delivery Years | 2023-2025 | 2024-2026 | 2025-2032 | ||

|

| Target (MW) | Awarded (MW) | Target (MW) | Awarded (MW) | Target (MW) |

| Ground-Mounted Solar | 1,260.78 | 1,490.23 | 6,715 | 1,968.98 | 0 |

| Roof-Mounted Solar | 0 | 0 | 605 | 9.39 | 0 |

| Floating Solar | 0 | 0 | 300 | 90 | 0 |

| Onshore Wind | 360 | 374 | 3,720 | 1,512.38 | 0 |

| Biomass | 0 | 3.4 | 230 | 0 | 0 |

| Run-of-River Hydro | 145.35 | 119.1 | 0 | 0 | 0 |

| Waste-to-Energy | 0 | 0 | 30 | 0 | 0 |

| Geothermal | 0 | 0 | 0 | 0 | 1,400 |

| Pumped-Storage Hydro | 0 | 0 | 0 | 0 | 1,400 |

| Impounding Hydro | 0 | 0 | 0 | 0 | 1,599 |

| Total | 1,766.13 | 1,986.73 | 11,600 | 3,580.76 | 4,399 |

Table 1. The Green Energy Auction Program (GEAP) in the Philippines

The silver lining in the challenges is the Green Energy Auction Reserve prices, or the price ceilings, for each technology for the first two rounds, were actually lower than the annual average industrial tariff for both 2023 and 2024, except for biomass waste-to-energy with relatively low awarded capacity (Graph 2).

This is an optimistic development for renewable energy consumers, who can pay less for more sustainable energy. However, while the RPS and the GEAP work together to boost new renewable energy installation through regulatory and fiscal incentives, issues in pricing and grid stability hinder the full potential of these programs.

Graph 2. Auction Ceiling Prices vs Industrial Tariff

Demand-side market mechanisms for renewable energy development: Limited effectiveness

As a forerunner in market liberalization and renewable energy target-setting, the Philippines has also actively worked to enhance market accessibility of renewable energy electricity. The country has developed a myriad of market mechanisms and policy tools to drive renewable energy growth and lower purchase threshold.

A game-changer is the Green Energy Option Program (GEOP), which aims to enable qualified consumers the freedom to choose renewable energy suppliers in addition to their current utility. The GEOP focuses on providing 100% renewable energy for consumers with an average peak demand over 100 kW in the past 12 months.

| GEOP | |

| Mechanism | Initiated under Renewable Energy Act (2008); enables sourcing electricity exclusively from RE sources since December 2021. |

| Energy Sources | Suppliers provide electricity solely from renewable sources like solar, wind, hydro, and geothermal. |

| Consumer Eligibility | Average peak demand of at least 100 kW over the past 12 months. |

Table 2. The Green Energy Option Program (GEOP)

Promulgated in 2021, the scheme has attracted 531 end-users as of November 2024 but in there are only 20 renewable energy suppliers, stressing undersupply of the program. Furthermore, a 2023 survey[1] aiming to improve the GEOP shows that businesses have little awareness of the scheme and while they are highly interested, they cited challenges in fulfilling the peak demand threshold and the application process, as well as concerns over supply availability.

As a matter of fact, end-users need to go through a 90-day switch procedure in order to switch from their current distribution utility to a renewable energy supplier in the GEOP. The lack of supply is recognized among renewable energy developers, who recognize of the growing demand but are discouraged by heavy bureaucracy in project approval, obtaining loans for small industry players, and grid limitation.

Progressive market mechanisms constrained by the grid

The Philippines is an archipelagic country with over 7,000 islands and islets but the grid infrastructure was designed for conventional baseload power such as coal and gas and is now experiencing difficulty accommodating variable renewable energy. So despite the country’s progressive electricity market liberalization and ambitious renewable energy policies to enable greater access to renewable energy supply, grid constraints have prohibited industry players from taking the necessary steps toward renewables.

Nonetheless, the policies and market mechanisms in the Philippines have just started out and are in the process of being fine-tuned (the GEOP began at the end of 2021 and the GEAP started in 2022). We expect an uptake in renewables to truly manifest when the grid is ready as the government improve administerial efficiency and financial feasibility in renewable energy investment and utilization. Because market mechanisms are already in place, once the infrastructure is ready, existing framework will streamline businesses’ renewable energy procurement process.

On a related note, the possibility of power export to another island across the strait will depend on how much excess capacity there is after the growing domestic demand has been satisfied. Submarine grid construction required for the cross-border power trading is also likely a second objective after the domestic grid system enhancement. Moreover, Taiwan needs to think about whether the energy source and plants it wishes to procure align with Taiwanese companies’ purchase standards.

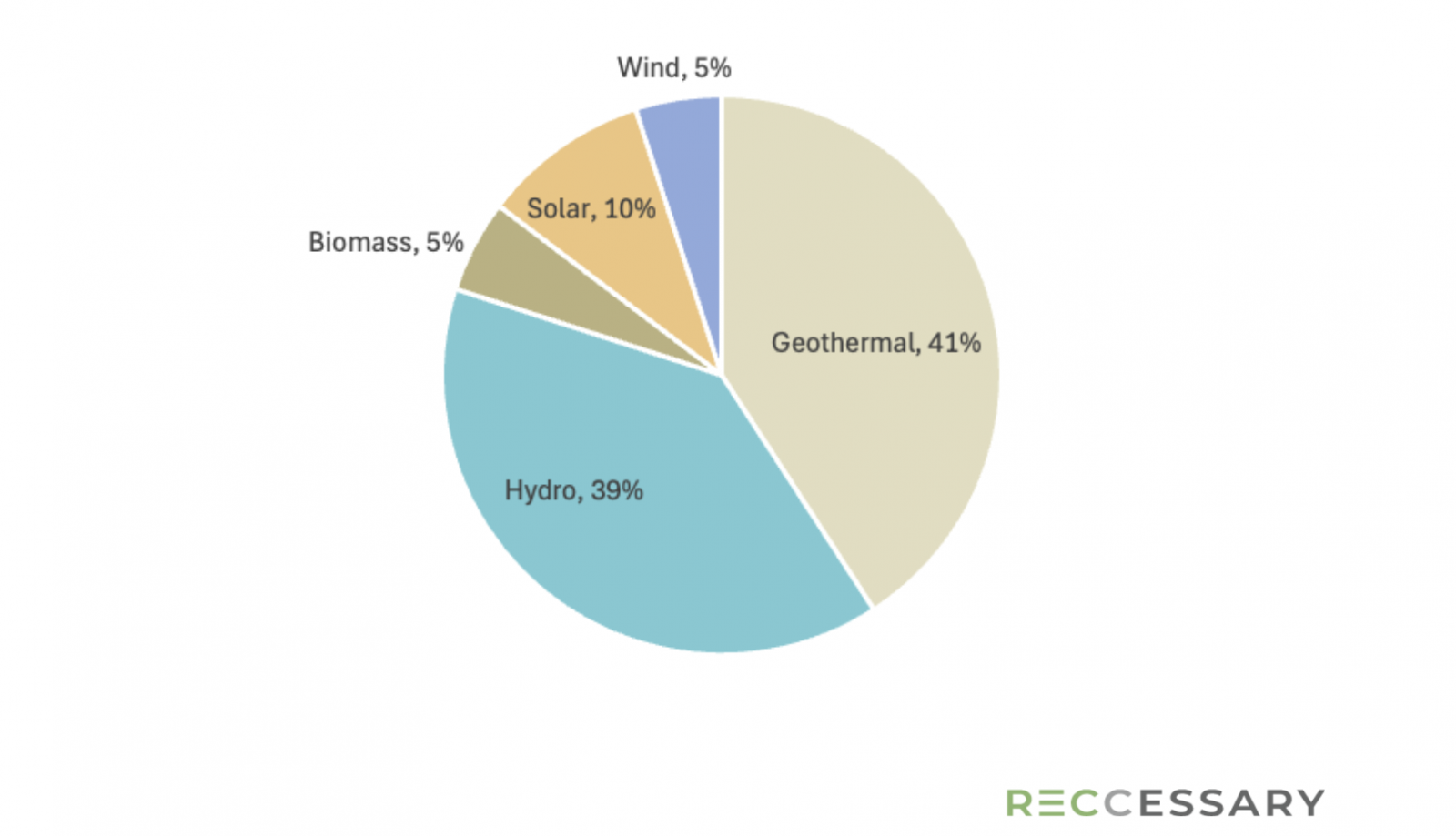

Geothermal and hydropower made up 80% of the Philippines renewable energy generation in 2023 (Graph 3). While both are dispatchable energy that provides consistent baseload, which is ideal for cheaper and more controllable long-distance transmission, these projects were built decades ago and may come into conflict with international standards for corporate scope 2 decarbonization.

Graph 3. Renewable Energy Generation by Technology (2023)

All in all, the Philippines’ policies are heading toward its energy transition target and actively competing with its regional neighbors in creating a low-carbon environment for foreign investments.

[1]RE Energize PH Survey Report by The Climate Reality Project, Philippines