(Photo: iStock)

In June, Taiwan's Carbon Exchange launched its first batch of blue carbon credits from a mangrove restoration project in Myanmar, certified by international body Verra. This initiative is part of a broader plan to promote high-quality, nature-based carbon credits, a type favored by global corporations like Apple and Microsoft.

With a wide array of carbon credit types and price ranges in the market, how can businesses evaluate the benefits and risks of these instruments? This report delves into the evolving dynamics of the voluntary carbon market.

Global voluntary carbon market: Decline in trading volumes

Despite the growing focus on emissions reduction, the 2023 Global Voluntary Carbon Market Report reveals a contraction of at least 60% in market value, down to $723 million. This decline stems from increasing scrutiny of carbon credit quality and widespread greenwashing scandals.

As a result, many businesses and investors have opted to monitor market developments while waiting for stricter and more credible standards. This cautious approach has led to decreases in both trading volumes and total transaction value (see Figure 1).

.png)

Figure 1. Voluntary carbon market trading trends, 2005–2023

The decline in market confidence is also reflected in falling prices across most types of carbon credits (see Figure 2). For instance, projects in the Forestry and Land Management category, particularly REDD+ projects (78% market share), have seen reduced demand due to overestimated benefits in the past. Buyers are now cautious, and sellers are waiting for more rigorous methodologies, resulting in sluggish trading and declining prices.

Meanwhile, renewable energy projects have witnessed slowing demand growth due to decreasing additionality. However, Agriculture projects, supported by technologies like soil carbon sequestration, have experienced continuous growth in trading volume over the past four years, despite falling prices due to increased supply.

.png)

Figure 2. Changes in carbon credit prices in the voluntary market, 2022–2023

Corporate use of carbon credits: Trends and preferences

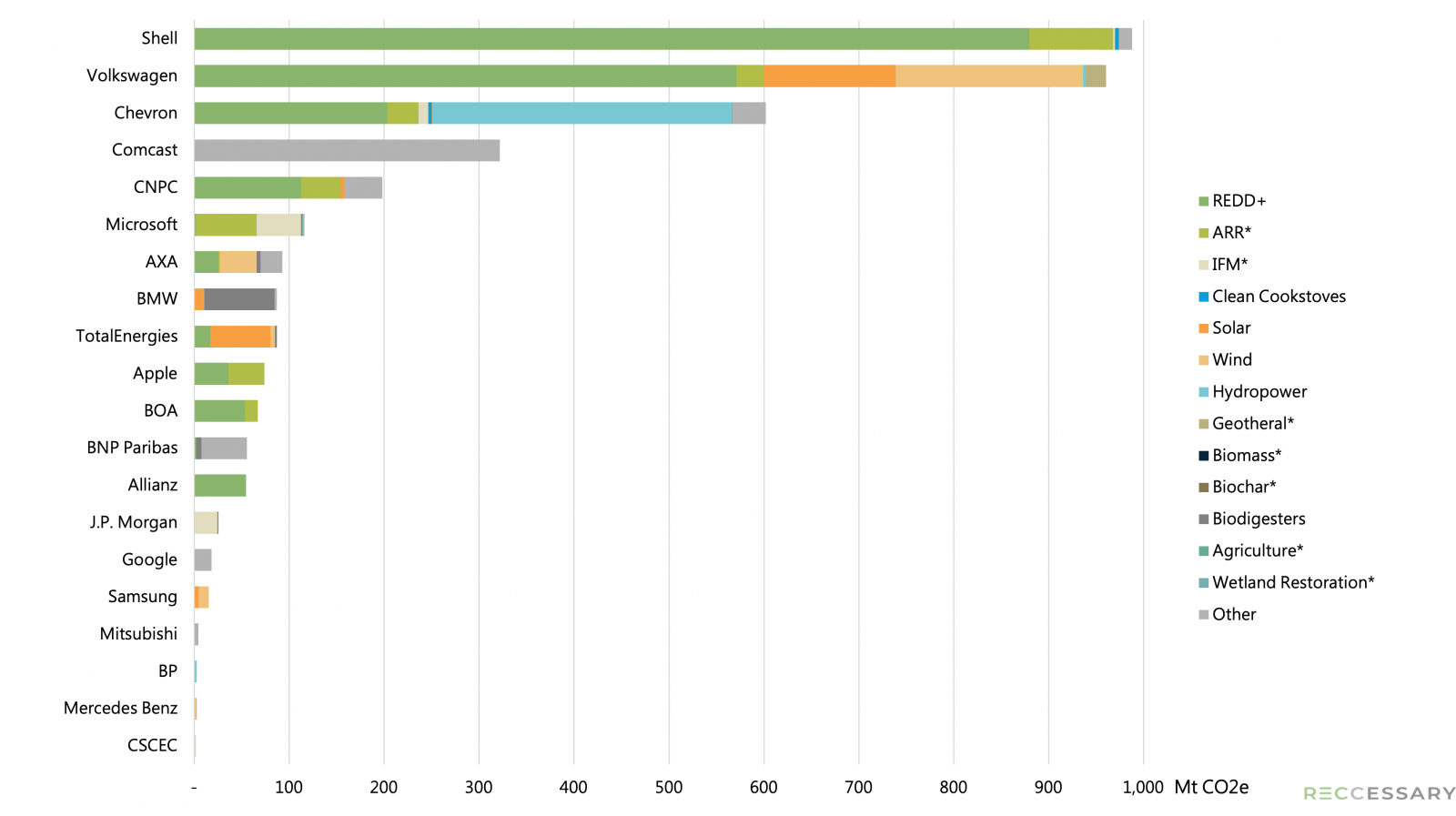

The behavior of individual corporations plays a significant role in shaping the global carbon market. Many major companies are actively investing in carbon credits, and supply chain businesses must align with these preferences. Figure 3 highlights the types of carbon credits used by the top 20 corporate users globally.

Figure 3. Top 20 corporate users of carbon credits by type, 2020–2022[1]

1. Preference for removal-based projects

Carbon credits are categorized into removal and avoidance types. Removal credits involve directly capturing greenhouse gases from the atmosphere, such as through afforestation, improved forest management, soil carbon sequestration, or blue carbon initiatives like wetland restoration. These projects are growing rapidly, with trading volumes increasing sevenfold in the past year, despite high technical and cost barriers.

Conversely, avoidance credits (e.g., REDD+ or renewable energy) prevent emissions but do not remove existing emissions. These projects rely on assumptions and projections, often leading to overestimated benefits.

Despite their limitations, avoidance credits account for 75% of corporate carbon offset usage. Businesses must carefully assess the risks associated with these credits, as highlighted by a Corporate Accountability investigation showing that over 90% of Chevron's credits were deemed low-quality.

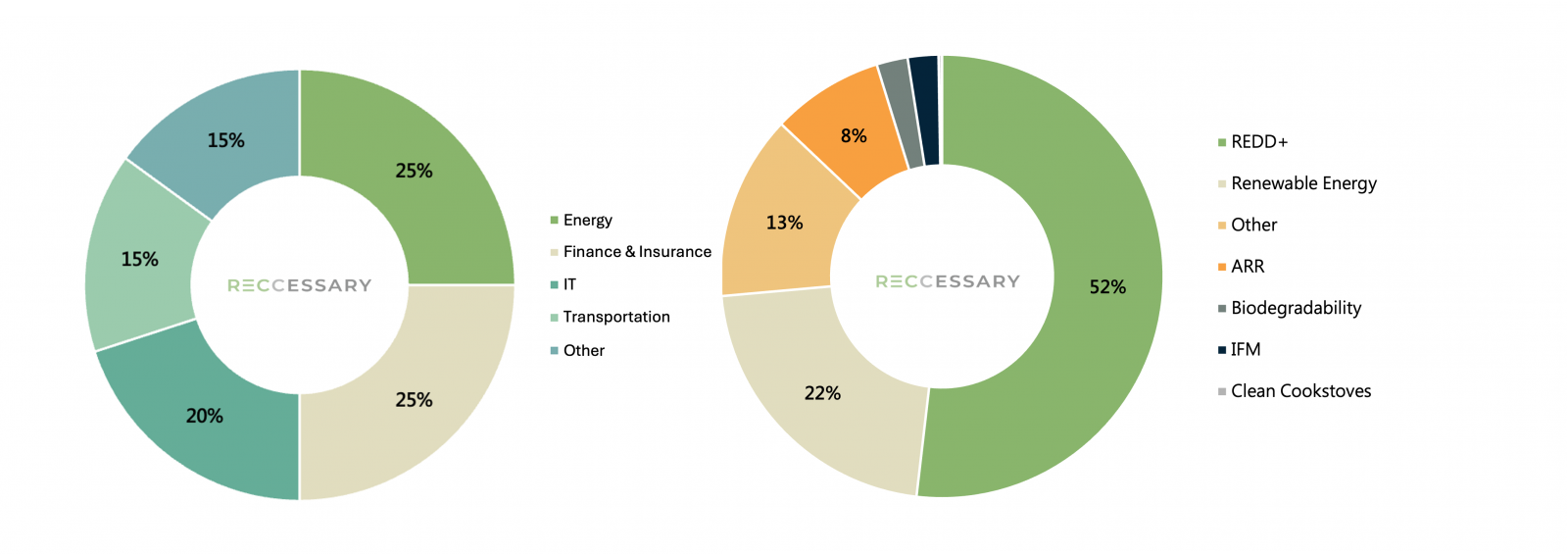

2. Dominance of the energy and financial sectors

Energy and financial companies dominate the list of top carbon credit users, followed by technology firms like Apple, Google, and Microsoft (see Figure 4). Within the energy sector, fossil fuel companies such as Shell and Chevron are prominent.

These firms face high emissions but often opt for low-cost carbon credits—such as forest credits priced at $3–$17 per tonne—over investing in innovative green technologies, which cost $30–$150 per tonne. This strategy enables them to reduce costs by 2 to 50 times compared to more sustainable methods.

Figure 4. Industry distribution of the top 20 corporate users of carbon credits

3. REDD+ projects: The most popular choice until 2023

Despite controversies, REDD+ projects accounted for nearly 80% of transactions within the forestry category, followed by afforestation (ARR) and renewable energy projects. Companies like Shell, Volkswagen, and Bank of America continue to favor these credits, highlighting their commitment to biodiversity and forest conservation.

In renewable energy, hydropower, wind, and solar remain popular due to technological maturity and lower costs.

Corporate strategies for long-term engagement in carbon markets

Given the volatile nature of the voluntary carbon market, businesses must adopt strategies to mitigate risks and achieve sustainable goals. The following three principles can guide effective decision-making:

1. Avoid high-risk carbon projects

While companies like Apple and Shell continue using riskier carbon credits, this approach may not suit all businesses. Short-term compliance with supply chain requirements may be acceptable, but long-term strategies should focus on high-quality projects to avoid investments becoming obsolete or rejected by the market.

2. Focus on removal-based projects

Removal projects, such as direct air capture (DACCS) or blue carbon initiatives, offer long-term storage of greenhouse gases and align with stringent climate goals. Taiwan’s Carbon Exchange recently launched such projects, emphasizing their future importance as scalable solutions.

3. Prioritize internal emission reductions

Carbon credits should serve as supplementary tools rather than primary solutions. Companies should prioritize reducing emissions within their operations through process improvements, energy efficiency upgrades, or digital carbon management systems to achieve carbon neutrality.

Conclusion

The voluntary carbon market remains a vital tool in the global fight against climate change, despite its current challenges. For companies, navigating this complex landscape requires diligence in project selection, an understanding of market dynamics, and a commitment to sustainable practices. By balancing investments in high-quality carbon credits with internal decarbonization efforts, businesses can position themselves as leaders in the transition to a low-carbon economy.

[1] The asterisk (*) indicates that the carbon credit belongs to the carbon removal category.

Sources: Ecosystem Marketplace, CDP, Climate Action 100+, Carbon Brief