.jpg)

(Photo: iStock)

Total issuance of I-RECs and TIGRs saw a 130% year-on-year growth last year in the region. There is little doubt that renewable energy certificates (RECs) are growing in popularity as a tool for scope 2 decarbonization in Southeast Asia. The reasons are straightforward, including the tool’s easy-to-understand mechanism, flexible procurement term and amount, and at times, cheaper prices. But there are a few things to watch out for when buying this simple tool in the region.

The matters with unbundled RECs: greenwashing risks and market instability

Greenwashing

Greenwashing concern has surfaced to the forefront of environmental commodities purchase around the world. For RECs, the use is clouded by 1) double counting and 2) environmental attribute overstatement.

Double counting, or otherwise understood as double claiming of the environmental attribute of RECs, occurs when power producers and utilities both claim the RECs from green power. This may be an especially prominent issue in Southeast Asia where ownership disputes of power generation between independent power producers and utilities have been identified.

Overstating environmental attribute is another issue. RECs can be used to overstate the extent to which companies are decarbonizing their power use. The problem arises because renewable energy already reduces grid emissions when it is generated so companies’ claims of emission reduction with REC purchase could be redundant. Relatedly, because unbundled RECs do not involve the actual use of renewable energy, the associated environmental attribute stops short at financing renewable energy projects with each purchase, a claim that has been found to be dubious by some researchers. According to an insider, profits from RECs are more often reaped by the middlemen between producers and end clients, rather than the facilities.

Market Instability

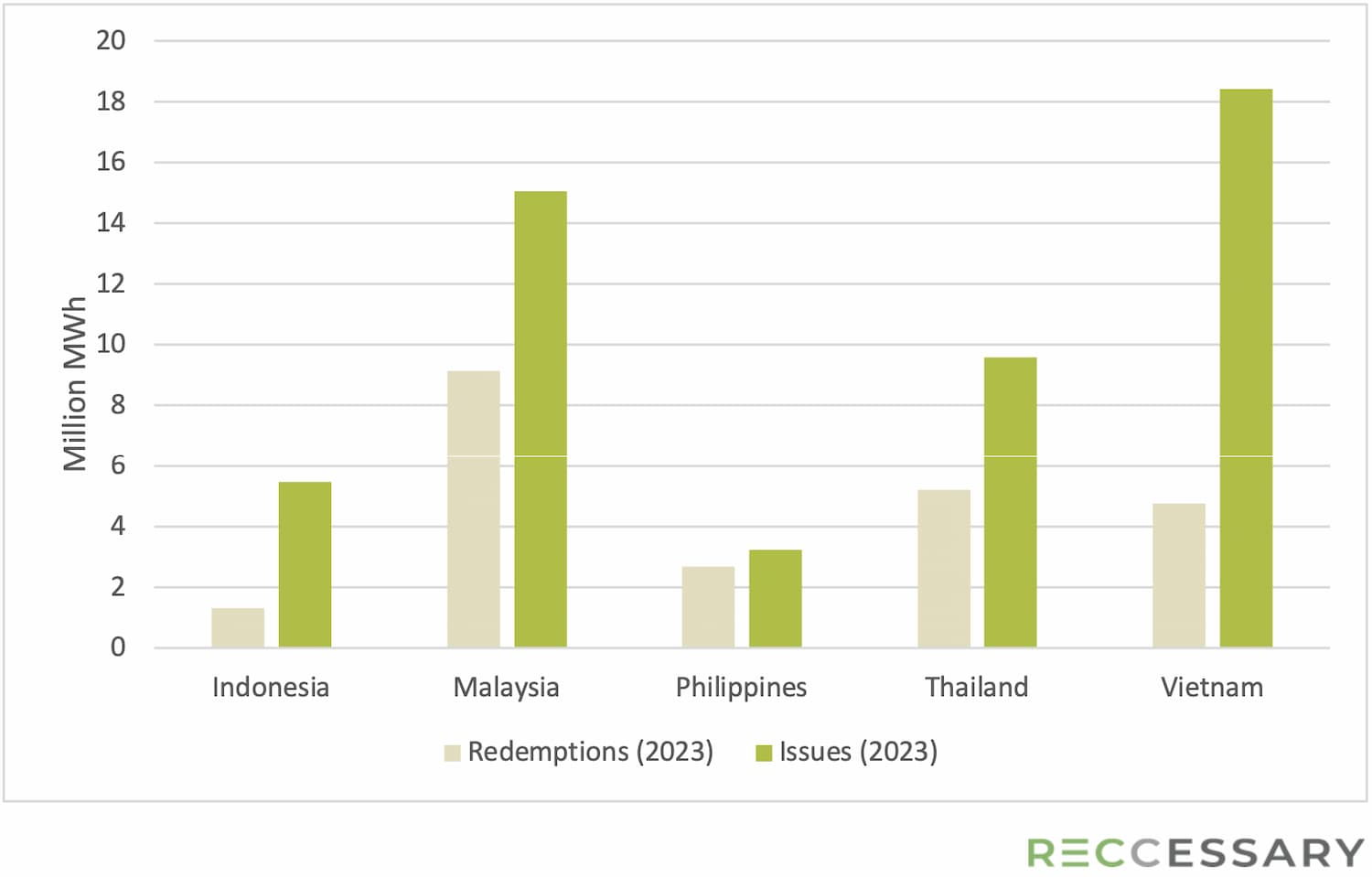

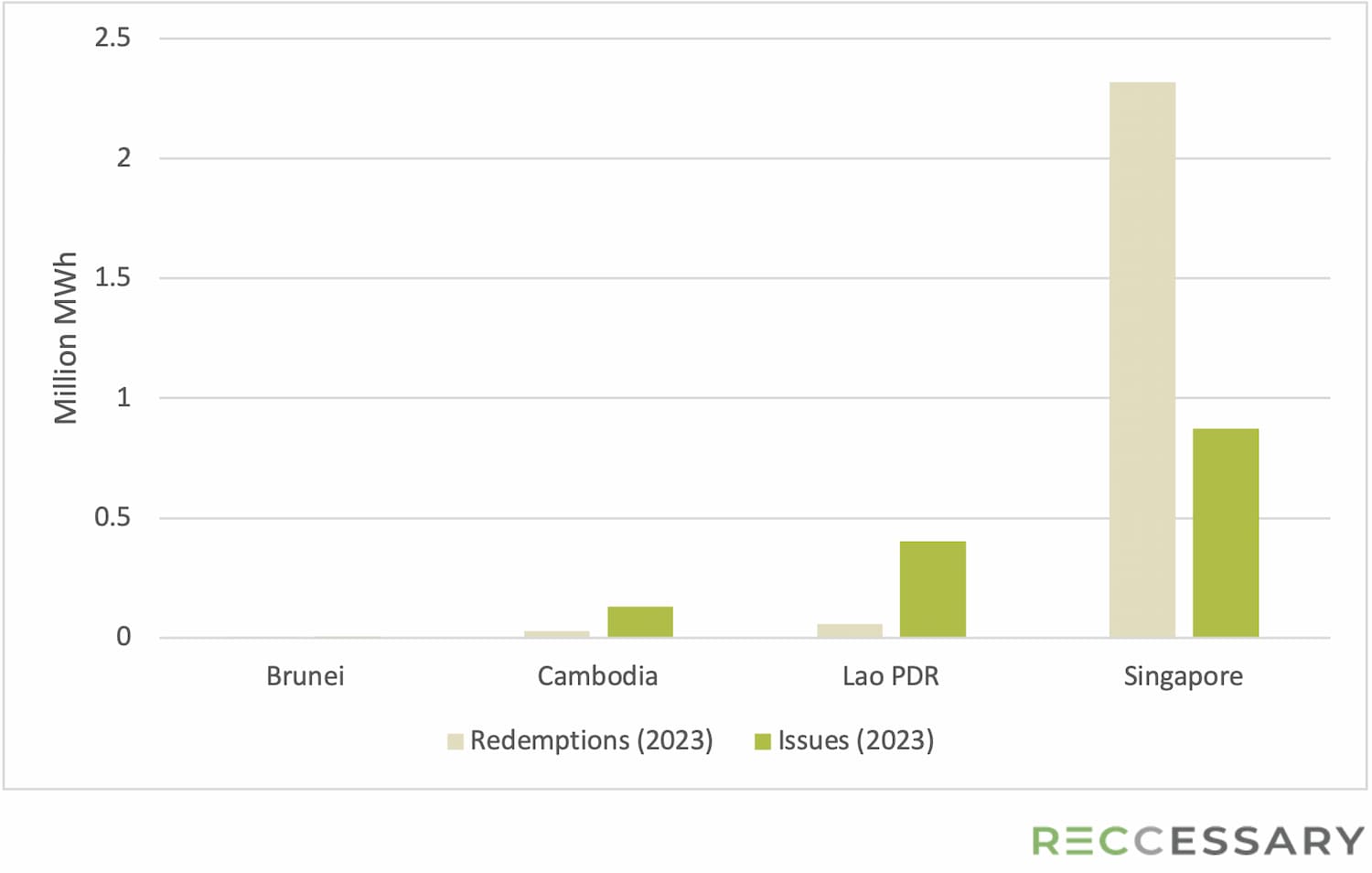

Apart from greenwashing risks, unbundled RECs are also susceptible to supply instability which then creates price fluctuations. The case for REC markets in Southeast Asia is worth noting because RECs are allowed to be traded across borders. As the figures below show, REC supply is sufficient in all Southeast Asian countries except for Singapore, and there is even an oversupply in Vietnam.

Figure 1. RECs Supply and Demand in 2023

Figure 2. RECs Supply and Demand in 2023

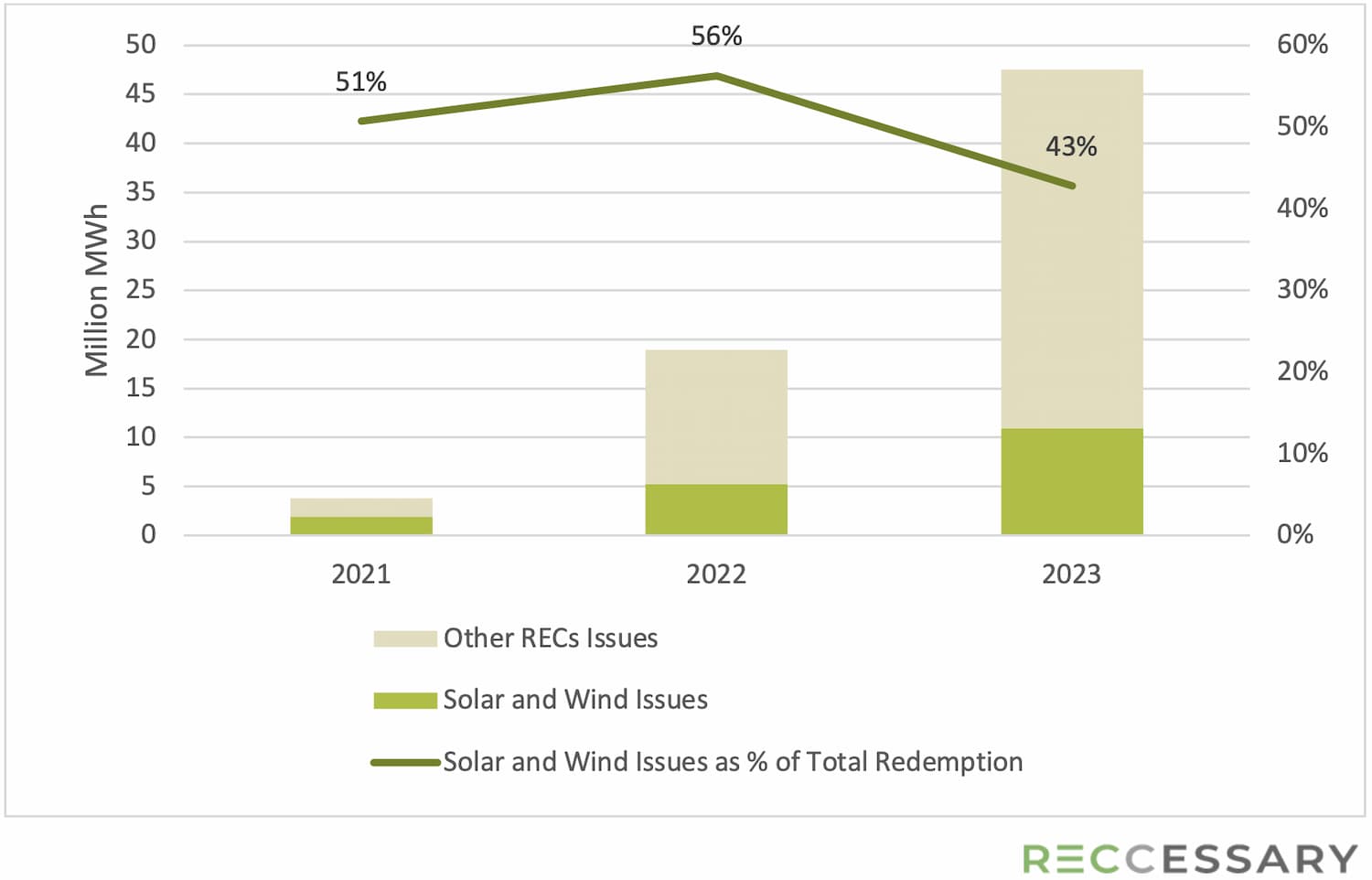

Yet, when it comes to the most desired products, solar and wind RECs, there exists the concern for retaining enough supply for renewable power generating countries and the abuse of prices for RECs sold from big supplier markets to high demand markets. At first glance, solar and wind RECs issuances have increased in absolute amount over the years, but a closer look will show that only 22% are solar and wind in 2023, making up for 43% of the total redemption in the same year (see Figure. 3) In fact, variance in REC prices is already showing – based on the statistics we gathered, a solar REC bought in Vietnam can be sold for a price as much as tenfold the procurement costs.

Figure 3. Proportion of Solar Total I-REC Supply and Total I-REC Demand in Southeast Asia

The above-mentioned risks are further complicated by the region’s growing practice of cross-border power trading which, without comprehensive pricing and tracking frameworks, could breed protectionist measures when energy prices swing and create leeway for double counting.

Risk-mitigating market mechanisms: national platforms and stricter standards

Cognizant of these issues, governments in the region and leading standard setters are developing mechanisms to assert greater supervision over the market. While there are voluntary standards like SS 673 in Singapore that encourages prioritizing the use of domestic RECs, they serve as best-practice guides rather than legally binding documents given the difficulty to prove the inability to acquire domestic RECs. That said, emerging national REC systems in the region signal that there are sufficient incentives to take the registration and redemption of RECs under state management. At the same time, RE100 also narrows the definition for ‘renewable energy’ and has a 15-year limit on power facility age, effectively eliminating varying proportion of RECs available in each country as shown in the table below.

![]()

In the past five years, government agencies in Malaysia, Philippines, Indonesia, and Thailand have already devised domestic REC trading platforms or registry. In the next five years, we expect to see this effort to further consolidate as the deadline for RE60 by 2030 nears. The reason is multifold and first is that this will allow the states to better regulate and account for risks associated with REC trading.

Second, regional power trading via the ASEAN Power Grid (APG) calls for clearer regulations and data management as power-rich countries like Laos export power to high power demand economies. National registries could help countries in the region to reach regional and national renewable energy targets by keeping track of the installment and generation of renewable facilities. For these platforms acquire international recognition, it is most likely that countries will adopt international standards as some of them already do. Adopting existing standards not only provides external credibility, it also helps avoid aforementioned risks in cross-border trading along the APG.

In the meantime, as MNCs try to reduce their scope 3 emissions, more companies in the region will be required to abide to more stringent REC standards. These standards are mostly likely to prioritize use of RECs generated on the same national market of the company premise and to match REC as close to the time of its generation as possible. Nonetheless, the success of standard implementation hinges upon many other external factors to the enterprises such as national grid capacity, energy storage development, and renewable energy supply in the region. For now, it would be interesting to see if emerging national REC platforms will replace their foreign precursors and become the sole registries in each of their own country.

Three steps in buying RECs in Southeast Asia

With that, we recommend enterprises to follow these three steps when buying RECs in Southeast Asia.

- Check: Understand scope 2 emission reporting criteria with your organization, be that your end client or voluntary standards. Take special notice of the requirements around facility age, technology, location, and vintage.

- Buy: Avoid price abuse in price discovery. Reccessary offers assistance in finding a fair quotation in the market with our list of contacts.

- Claim: Ensure credible claims by making sure single ownership of RECs from purchase to retirement. This can be done through vetting the serial number of each REC on the registries.