.jpg)

(Photo: Pexels)

According to the International Maritime Organization (IMO), carbon emissions from the maritime industry account for 3% of the world's total. To accelerate industry decarbonization, the EU has included the maritime sector in its Emissions Trading System (ETS), requiring shipping companies to purchase carbon credits for 40% of the carbon dioxide emissions from vessels over 5,000 gross tonnages starting in 2024. The threshold will rise to 70% in 2025 and 100% in 2026[1]. In response, shipping companies have introduced a "carbon surcharge," which ranges from EUR 10 to 50 per twenty-foot equivalent unit (TEU) on routes to and from Europe, with pricing varying depending on the company and route.

Are carbon surcharges imposed reasonably by shipping operators?

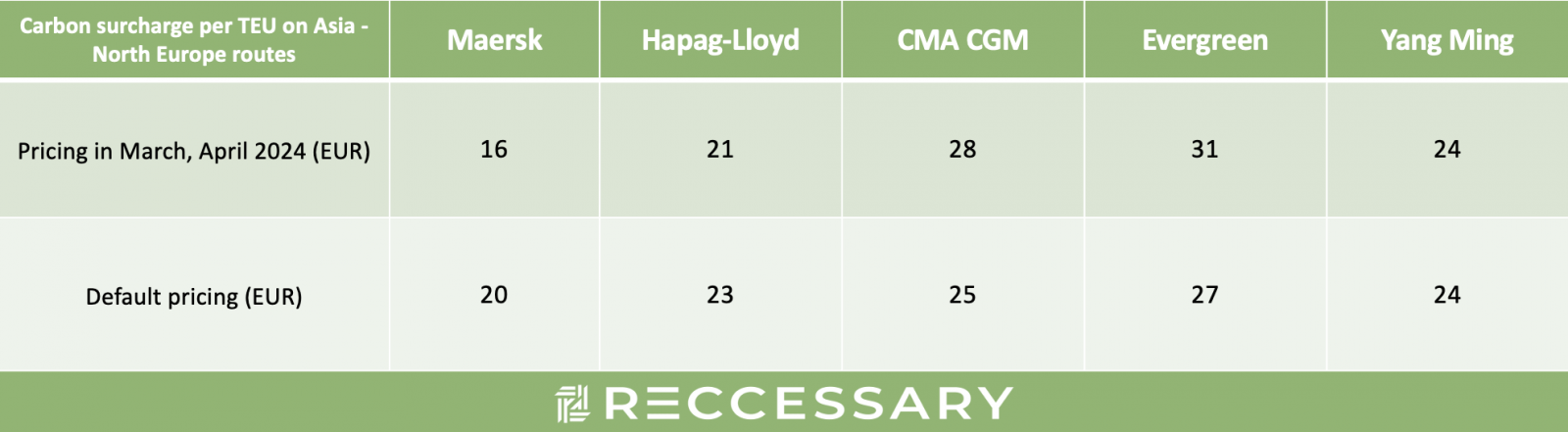

To control costs, shipping companies will pass on part of the carbon costs to their customers. The carbon surcharge pricing set by various companies is shown in Table 1 below. The question that should be asked is: Is this pricing reasonable?

Table 1. Carbon surcharge by shipping companies (Source: company announcements)

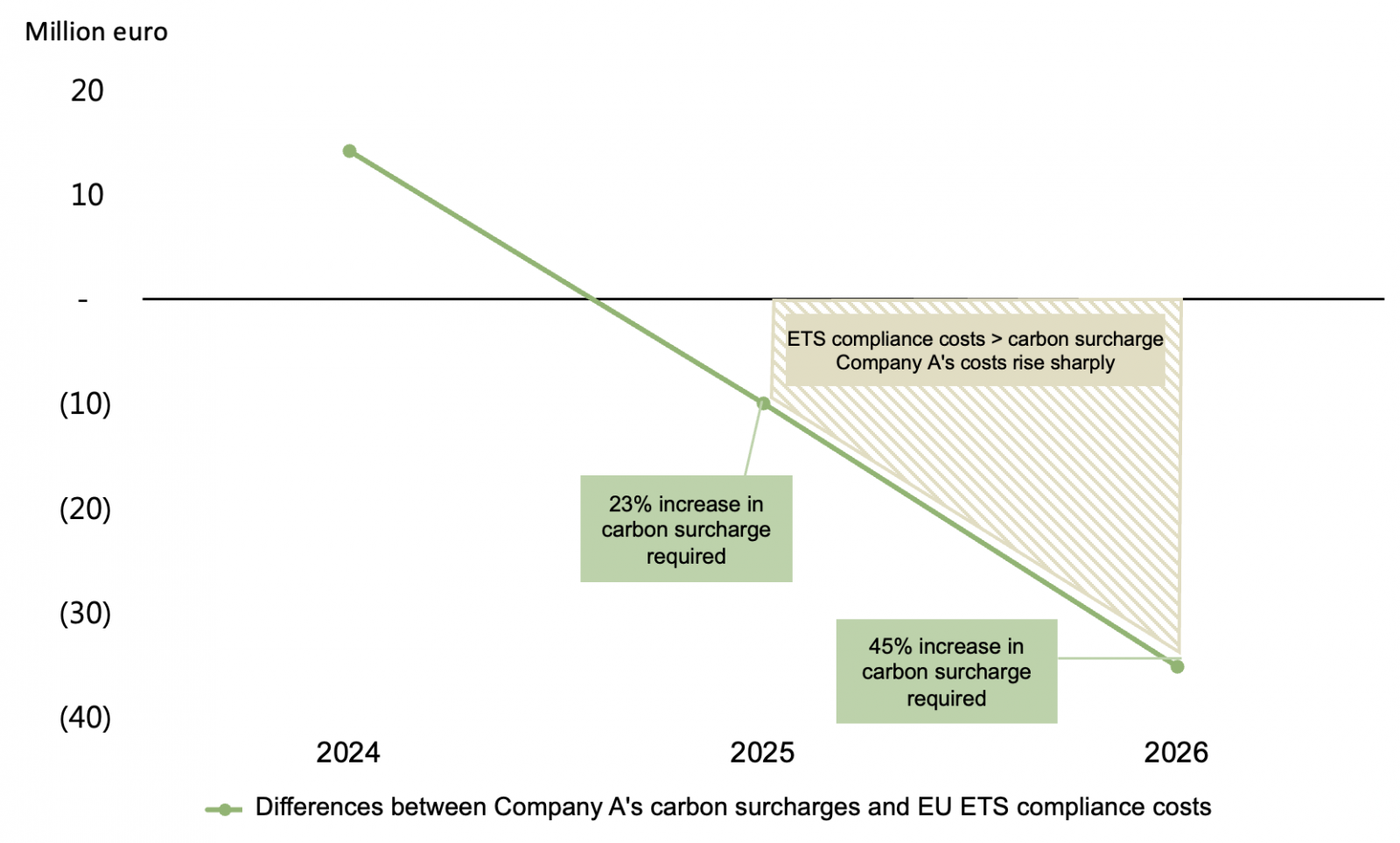

In a scenario where shipping company A has a fleet emissions of 1.4 million tonnes (Asia-North Europe route) and container traffic of 2 million TEUs, along with carbon price projections, Reccessary estimates that, for the same volume of traffic and no significant reductions in emissions, the company's carbon surcharge on customers in 2024 may be higher than its ETS compliance costs, with the gap ranging from EUR 15 to 25 million depending on different pricing and EU carbon price trends (see Figure 1). With the same carbon surcharge pricing and a carbon price of EUR 77 per tonne, company A will overcharge EUR 15 million, which could amount to EUR 25 million or more if the carbon prices fall to just over EUR 50 per tonne. However, as the EU carbon prices rise and the coverage of emissions control expands, company A need to increase the carbon surcharge to offset costs in the long run.

Figure 1. Gap between the carbon surcharge and ETS compliance costs for shipping company A

Company A’s example is by no means an exception. The European Federation for Transport and Environment (T&E) has also accused the current surcharge of profiteering. In a sample of voyages to and from European ports, they found that nearly 90% of shipping lines, including Maersk, Hapag-Lloyd, CMA CGM, and MSC, are overcharging. While some industry players believe that the calculation methods are flawed, it suggests that the carbon surcharges are inadequate in terms of transparency and room for price volatility, which can significantly affect the supply chain.

Risks arising from carbon surcharge pricing

Under the EU ETS, shipping operators are required to surrender EU allowances (EUAs) annually, with prices fluctuating between a high of EUR 95 per tonne and a low of EUR 53 per tonne over the past year. In this context, a fixed price for the shipping carbon surcharge could be controversial. This could be addressed by adjusting pricing on a monthly or quarterly basis, along with increased transparency in the disclosure of pricing information. Currently, the pricing gap between shipping companies can be more than EUR 10 per TEU, without specifying what cost factors are involved in setting the surcharge. For the cost of purchasing carbon allowances alone, EUR 16 to 21 per TEU might be more reasonable[2].

As around 80% of global goods, including raw materials, finished products and consumer goods, are transported by sea, excessive carbon surcharges could lead to significant green inflation. When environmental costs are factored into business operations, companies are forced to raise the price of their products to maintain profitability, and these price increases will be passed along the supply chain and ultimately paid for by consumers.

With governments and major brands committing to net-zero emissions, factors such as compliance with environmental standards, green purchasing and product carbon footprints will impact cooperation opportunities and sales in future markets. Therefore, it is necessary for businesses to engage in carbon reduction to maintain green competitiveness. For shipping companies, using green fuels, switching to eco-friendly vessels, optimizing routes, and controlling sailing speeds can help reduce carbon emissions and lower ETS compliance costs, enabling the reduction of carbon surcharges to attract consumers.

Balance between costs and risk transfer

As concerns grow over environmental costs and governments adopt stricter carbon emissions controls, it becomes increasingly challenging for shipping operators to balance costs with risk transfer. While the pursuit of profitability is inherent in business, it is reasonable for them to pass on costs to their customers. However, overpriced carbon surcharges may adversely affect the industrial chain. Therefore, as the carbon surcharge mechanism has come into effect in 2024, companies should constantly adjust their strategies to strike a balance between achieving environmental goals and maintaining competitiveness and sustainable development in the industry.

When setting the carbon surcharge, shipping operators need to give thorough consideration to ensure that the pricing is effective in facilitating the achievement of carbon reduction targets without imposing an undue burden. Strategies that may be adopted by shipping operators include regularly adjusting rates in accordance with carbon price fluctuations, enhancing pricing transparency to build customer trust, and utilizing the carbon surcharge revenue to invest in carbon reduction technologies or initiatives. By doing so, they can not only balance operating costs and risk transfer but also make positive contributions to sustainable development, establish a good corporate image, and move towards a more sustainable future with their customers.

[1] For detailed specifications and calculation methods, please refer to the announcement by the European Commission.

[2] Based on EUA prices in April 2024