(Photo: iStock)

As climate change accelerates, countries are adopting measures to reduce greenhouse gas emissions. Renewable energy certificates (RECs) and carbon credit markets have emerged as critical tools for achieving net-zero targets. While RECs promote renewable energy development, carbon credits use pricing mechanisms to curb total emissions. With overlapping goals, will these markets converge or diverge in the future? This report examines potential trends using Southeast Asia as a case study.

Overview of REC and carbon credit markets

Southeast Asia's renewable energy landscape

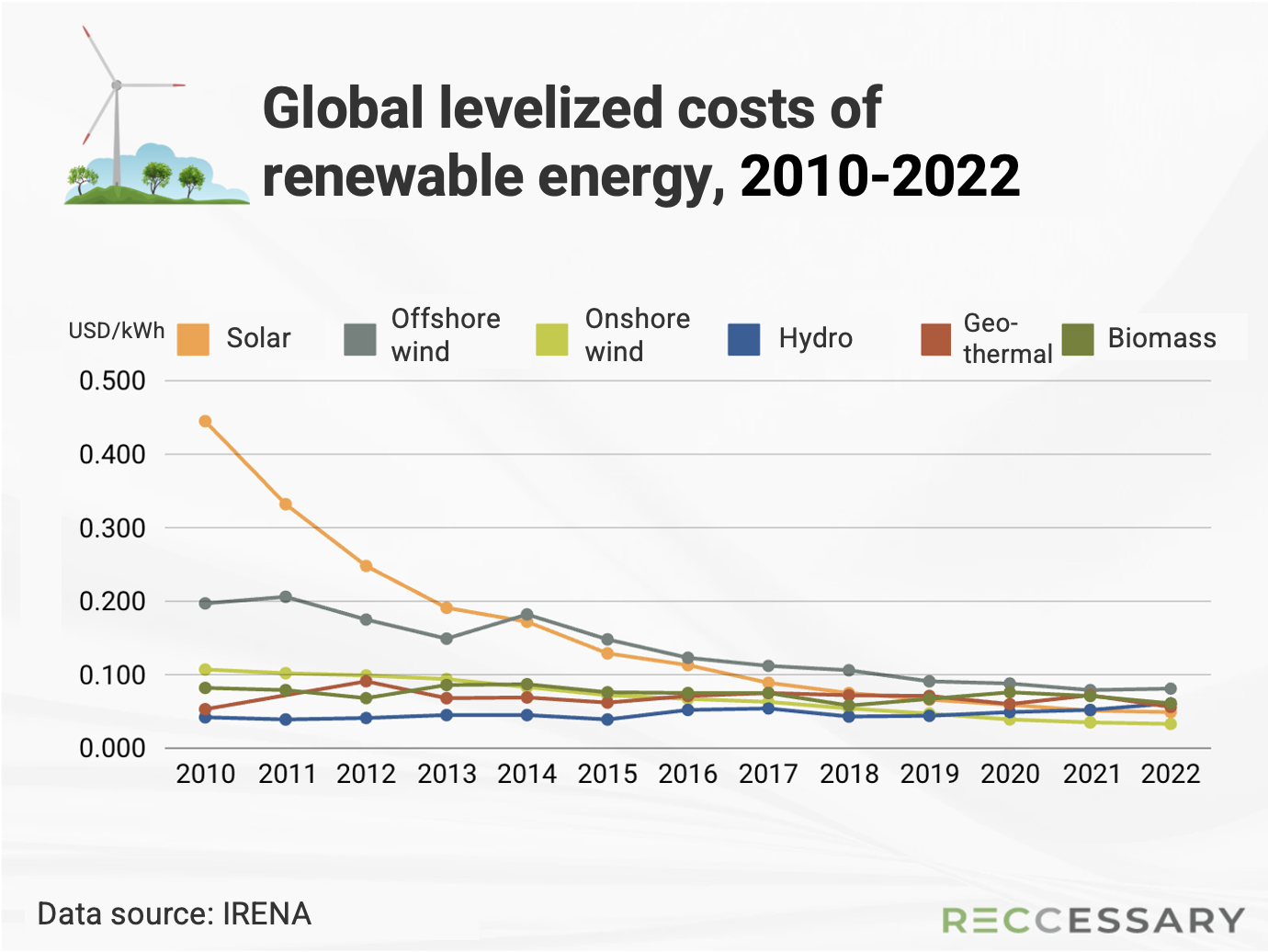

Southeast Asia boasts abundant renewable energy resources, forming the foundation of its REC market. Vietnam, for example, expanded its solar capacity from less than 1 GW in 2018 to approximately 16 GW by 2020, becoming the region's largest solar market. Thailand has achieved significant progress in biomass and small-scale hydropower. Falling costs of solar and wind technologies have further enhanced the competitiveness of renewables in power markets (see Figure 1).

Figure 1. Global levelized costs of renewable energy, 2010–2022[1]

Carbon credit market development

In contrast, carbon credit markets in Southeast Asia remain nascent. Unlike the European Union Emissions Trading System (EU ETS) established in 2005, Southeast Asia's carbon markets are still developing. However, governments are increasingly prioritizing emissions reduction, with Vietnam set to trial a carbon trading scheme by 2025, initially targeting high-emission industries like steel and cement.

Similarities between RECs and carbon credits

1. Unified goals

Both RECs and carbon credits aim to reduce greenhouse gas emissions. Southeast Asian countries are integrating renewable energy promotion and emissions reduction into their energy and environmental policies, forming a dual approach to achieve national decarbonization goals.

2. Trading mechanisms

Both RECs and carbon credits can be traded on platforms or over-the-counter (OTC). OTC transactions, which allow buyers and sellers to negotiate project-specific terms, dominate the market. Trading platforms in Malaysia and Thailand enable companies to access both RECs and carbon credits, providing integrated solutions for emissions reduction.

Key differences between RECs and carbon credits

1. Scope of application

While both tools share the common goal of reducing emissions, their applications differ. RECs address Scope 2 (indirect emissions from electricity use), while carbon credits apply to Scopes 1, 2, and 3. This distinction defines their role in offsetting emissions.

For instance, carbon credits are capped at 5% of offset allowances in many markets, requiring companies to rely on other measures like energy efficiency improvements or renewable energy adoption. RECs remain essential in this context.

RECs are more suitable for energy-intensive businesses, such as data centers and large retail chains, to offset operational electricity use. Carbon credits, on the other hand, serve as tools for hard-to-abate sectors like manufacturing, transportation, and petrochemicals to meet decarbonization goals. They also provide additional benefits, such as biodiversity conservation, enhancing corporate sustainability reputations.

2. Source of projects

RECs derive from renewable electricity supply, while carbon credits encompass diverse sources, including natural resources (forests and oceans), renewable energy, and emissions reduction in residential or commercial sectors.

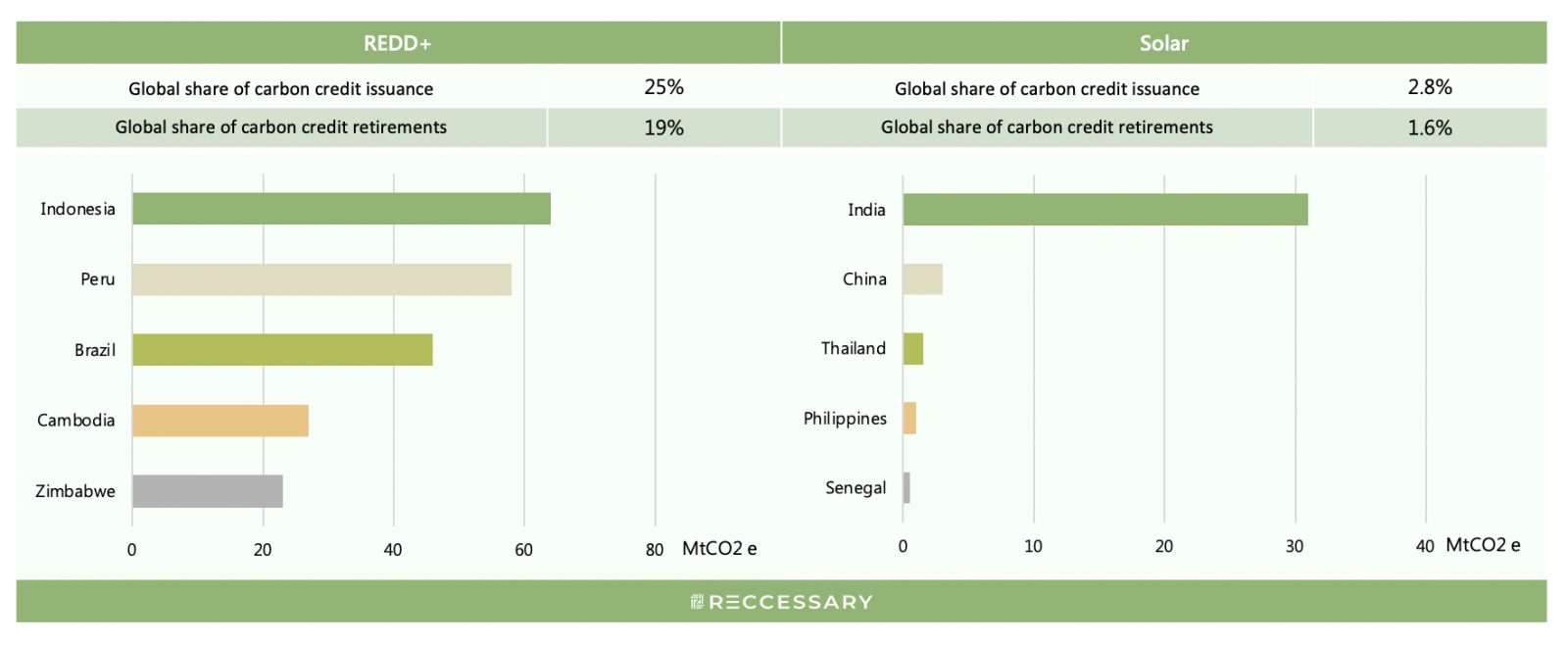

For example, Indonesia’s tropical rainforests offer significant potential for developing nature-based carbon credits, with its REDD+ forest credits accounting for approximately 25% of the global total. Thailand and the Philippines, leaders in solar and wind capacity in Southeast Asia, can leverage these resources to generate renewable energy-based carbon credits (see Figure 2).

Figure 2. Emission reductions from REDD+ and solar carbon credits[2]

Market trends: Convergence or divergence?

The SBTi controversy and its implications

Despite rapid development, RECs and carbon credits still differ in trading items, pricing mechanisms, and market maturity. Recent changes in the Science Based Targets initiative (SBTi) standards have raised concerns, potentially altering how RECs and carbon credits are used. The SBTi now allows companies to offset certain Scope 3 emissions with carbon credits rather than relying solely on RECs for Scope 2 reductions. While this could lead to synergies, there is potential for carbon credits to crowd out RECs, depending on future market dynamics.

Market maturity

RECs benefit from established systems like the International REC Standard (I-REC), offering global trading and management mechanisms. Carbon credit markets, however, are newer and lack unified frameworks. As carbon market standards evolve, they could challenge REC dominance, especially if SBTi updates reshape market rules.

Strategic recommendations for businesses

Understanding the nuances of REC and carbon credit markets is crucial for strategic planning. Businesses should actively engage in market developments and adopt diverse approaches:

- Invest in renewable energy: Diversify energy portfolios to include renewables.

- Enhance energy efficiency: Adopt advanced technologies for operational optimization.

- Build green brands: Leverage sustainability initiatives to strengthen corporate reputations.

Both RECs and carbon credits are pivotal to achieving net-zero goals. By proactively adapting to market changes, businesses can position themselves as leaders in the low-carbon economy.

[1] Source: International Renewable Energy Agency (IRENA)

[2] Source: UC Berkeley carbon credit database