.jpg)

Taiwan has experienced delays in renewable energy projects, especially in offshore wind and solar power, the island's largest renewable energy sources. (Photo: Wikimedia Commons)

{kind=link}

Taiwan's renewable energy market is at a pivotal point. With ambitious targets for decarbonization and energy transition, Taiwan is grappling with both progress and challenges in liberalizing its electricity market, increasing renewable energy capacity, and creating a more efficient market for green power. As Taiwan moves forward, understanding the trajectory of its renewable energy policies, particularly its feed-in tariff (FIT) scheme, will be crucial for businesses, investors, and policymakers.

This article highlights the key takeaways from a comprehensive report on Taiwan’s renewable energy market, focusing on the electricity market structure, renewable energy development and major challenges, especially from the feed-in tariff scheme. Additionally, the article will explore the international experiences from the UK and Germany to offer insights into potential future developments for Taiwan’s renewable energy market.

Taiwan’s electricity market and renewable energy development

Taiwan’s electricity market has undergone significant changes since the liberalization process began in the mid-1990s. The Electricity Act Amendment of 2017 marked a watershed moment in this transformation, opening the door for private sector participation in renewable energy generation and retail.

The law envisioned a two-phase liberalization process: the first focused on renewable energy, and the second, expected to include fossil fuels, was to be completed by 2025 but has since been delayed. Despite these advances, Taiwan's electricity market remains partially liberalized, with the state-owned Taipower still holding a dominant position in electricity transmission and distribution, particularly in conventional energy sources such as coal, gas, and oil.

By 2024, Taipower’s share of total installed capacity had decreased to 48%, yet it still controlled a significant portion of electricity sales. While the generation market has seen an influx of independent power producers (IPPs) in recent years, most renewable energy continues to be sold through Taipower’s transmission network. These limitations highlight the challenges Taiwan faces as it strives for a more competitive and diversified energy market.

Taipower maintains dominance in Taiwan’s electricity transmission and distribution. (Photo: RECCESSAEY/Carol Chen)

Growth of renewable energy in Taiwan

Since the introduction of the Electricity Act Amendment, renewable energy generation has grown steadily. The proportion of renewable energy generated in Taiwan has steadily increased, particularly with solar and wind power. Despite this growth, Taiwan still faces a relatively small proportion of renewable energy being sold to the free market. In 2023, Taiwan generated over 26 TWh of renewable energy, but only 7% of it entered the market for trade, suggesting a constrained supply and demand mismatch.

In the past few years, Taiwan has seen a surge in corporate demand for renewable energy, driven largely by major players such as Taiwan Semiconductor Manufacturing Company (TSMC), which significantly boosted its purchases of renewable energy in 2021. Demand has been rapidly growing in the next few years.

Key issues in Taiwan's renewable energy market

Despite this expansion, Taiwan's renewable energy market faces three main challenges: supply uncertainty, uneven distribution, and a rigid price floor.

1. Supply uncertainty

Taiwan has faced delays in its renewable energy projects, particularly in offshore wind and solar power, which are also the largest sources of renewable energy generation on the island. Several major projects have been delayed, and the target to reach 20 GW of solar and 6 GW of wind by 2025 has now been postponed to 2026. These delays are attributed to a variety of factors, including global supply chain disruptions and land development limitations. As a result, there is significant uncertainty in the supply of renewable energy in the coming years.

2. Uneven distribution

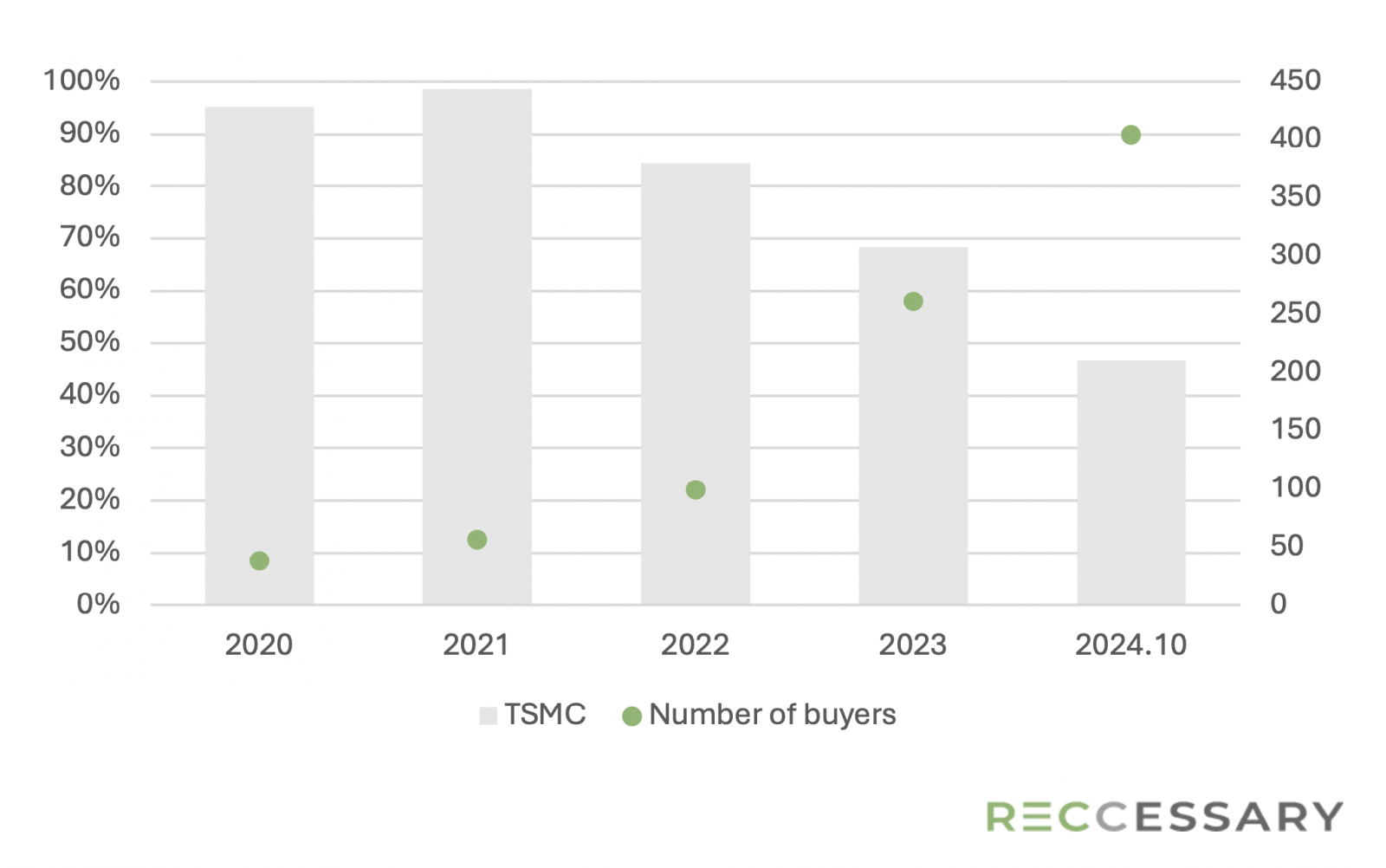

There is a noticeable concentration of renewable energy purchases among a few large buyers, particularly in the electronics industry. TSMC alone accounts for nearly half of all renewable energy purchases in Taiwan, highlighting an imbalance in access to renewable energy. Smaller companies, especially in traditional sectors, often face higher prices and opaque market conditions, limiting their ability to procure renewable energy at competitive rates. This lack of market transparency exacerbates the issue of unequal access to green power.

Graph 1. TSMC's green energy procurement share and changes in the number of buyers in Taiwan

3. Rigid price floor

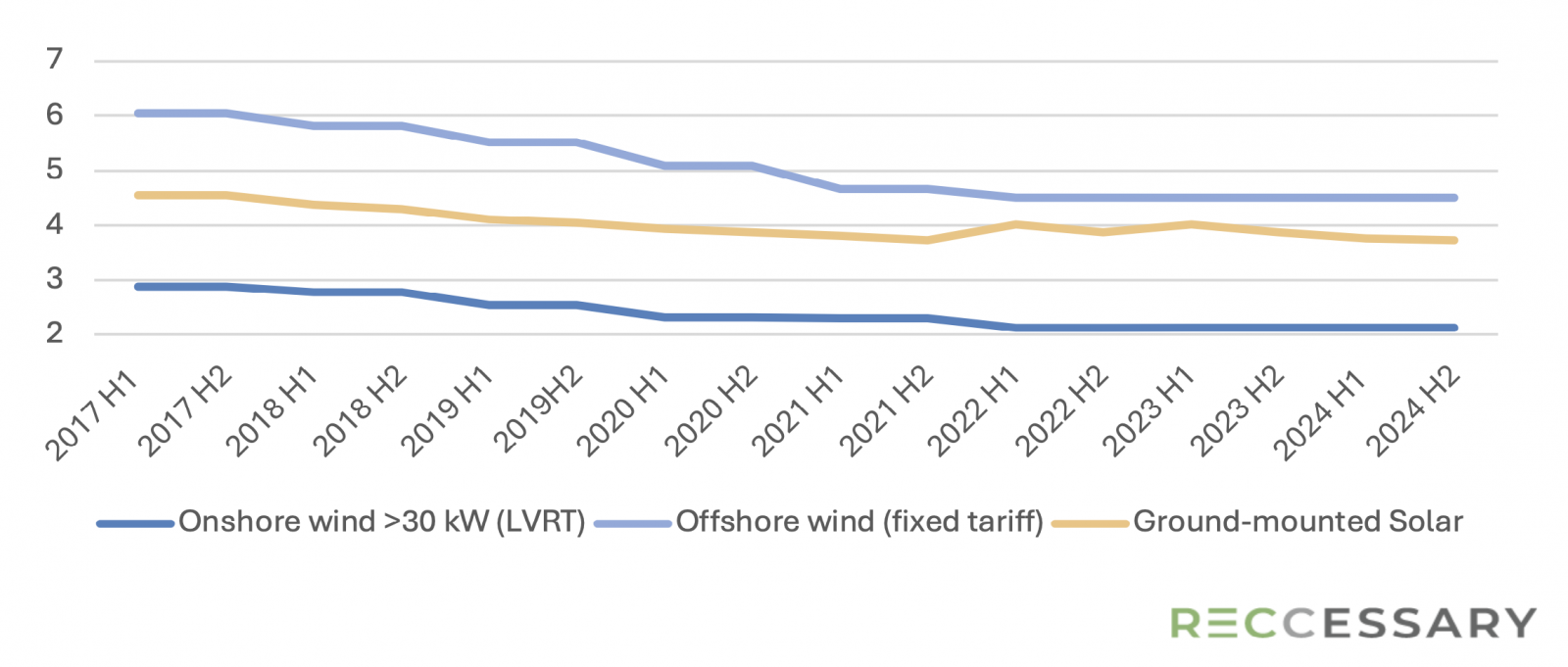

A significant issue in Taiwan’s renewable energy market is the rigidity of feed-in tariffs, which have not adjusted in response to market changes. The slow phase-out of feed-in tariffs, particularly for solar, has made it difficult for buyers to negotiate lower prices in the market. As a result, renewable energy prices remain high, limiting market participation and raising concerns about the long-term sustainability of Taiwan’s renewable energy transition.

Graph 2. Taiwan's FIT rate changes for solar and wind power (2017–2024)

Taiwan’s Feed-in Tariff scheme: An overview

Admittedly, the feed-in tariff (FIT) system in Taiwan has played a critical role in incentivizing the growth of renewable energy generation, particularly in solar and wind power. Introduced to guarantee a fixed payment for renewable energy producers, the FIT system has offered stability and certainty for investors, thereby driving the development of renewable energy projects. However, as Taiwan’s renewable energy market matures, the effectiveness of the FIT system has come into question.

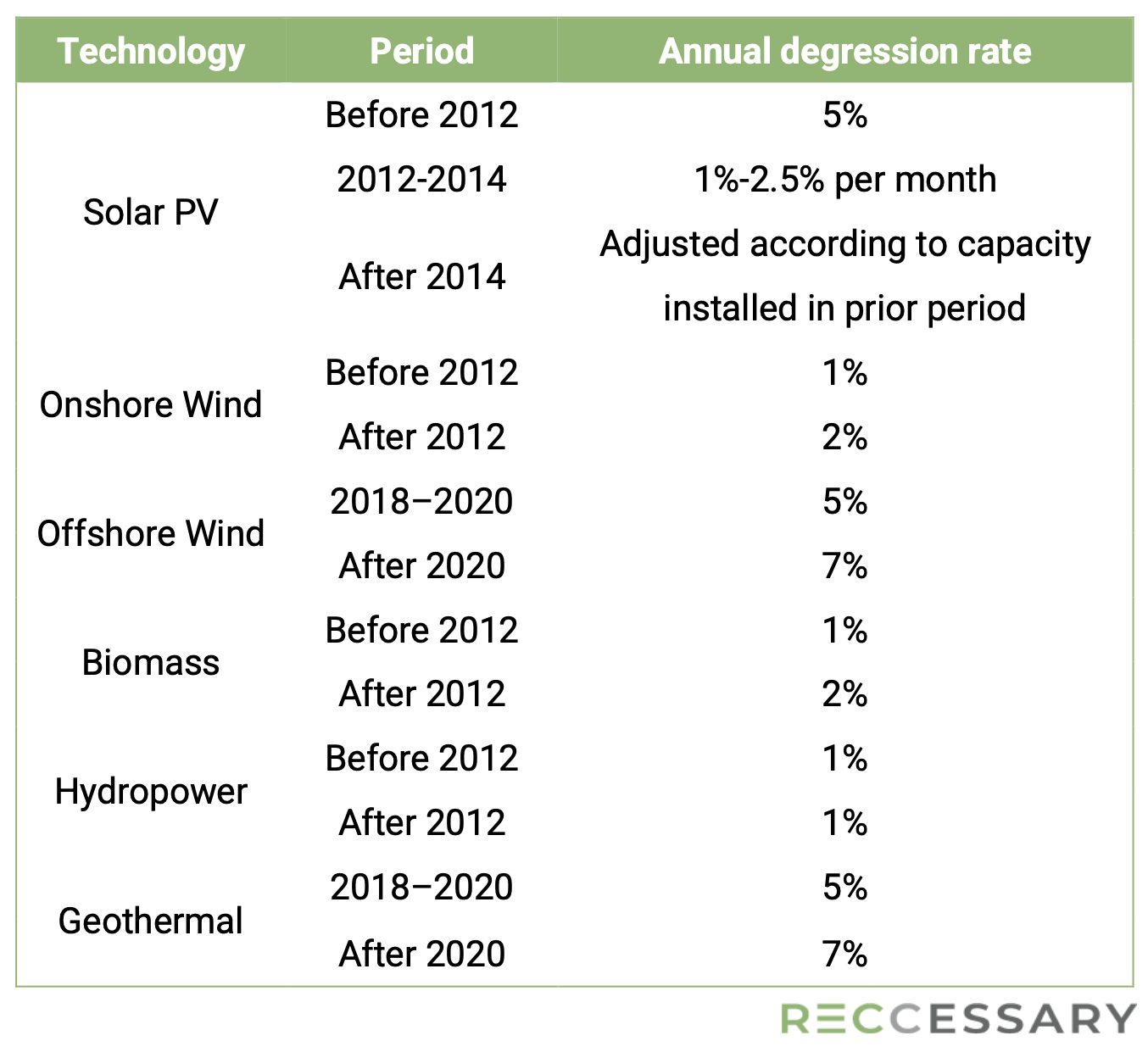

For solar power, the FIT rates have steadily decreased over time, in line with the global trend of reducing subsidies for renewables. Ground-mounted solar projects, for instance, saw their FIT rates gradually decrease by around 2.1% every half-year before the pandemic-induced increase in 2022. Despite these changes, FIT rates have remained relatively rigid, failing to reflect the lower costs of renewable energy production. In fact, compared to the scheme’s originator has phased out FIT for renewables at much faster rates (see the table below).

Table 1. Taiwan's FIT rates

The continued existence of the FIT system does not incentivize renewable energy producers to sell directly into the market, limiting the flexibility and responsiveness of the energy market.

One of the main critiques of the FIT system is that it fails to foster a truly competitive market. The rigid price floor prevents producers from adjusting prices to market conditions, and without a wholesale market, there is little transparency for buyers and sellers to negotiate fair prices. This lack of flexibility in the market raises concerns about Taiwan's ability to meet its renewable energy goals in a cost-effective manner.

International lessons: The UK and Germany’s success

To gain insight into how Taiwan could overcome its renewable energy market challenges, we look at the experiences of two relatively mature energy markets in Europe: the UK and Germany.

United Kingdom

The UK’s experience offers valuable lessons for Taiwan. The UK implemented two key mechanisms—the Renewable Energy Obligation (RO) and Contracts for Difference (CfD)—to increase the supply of renewable energy and reduce costs.

The RO scheme incentivized electricity suppliers to source a portion of their electricity from renewable sources, while the CfD scheme guarantees stable revenue for renewable energy developers, reducing their exposure to market price fluctuations. These schemes have been successful in increasing renewable energy capacity and lowering costs, particularly in offshore wind.

.jpg)

Offshore wind turbine installation at the Walney Offshore Wind Farm in the UK. (Photo: Wikimedia Commons)

{kind=link}

Taiwan could potentially adopt a similar approach by introducing a contract mechanism that allows renewable energy producers to hedge against price volatility, while also creating incentives for long-term investments in renewable energy.

Germany

Germany’s Renewable Energy Sources Act (EEG) has been pivotal in the country’s renewable energy transition. The EEG initially relied on feed-in tariffs to guarantee fixed payments for renewable energy producers. However, over time, Germany transitioned to a more market-driven model through competitive auctions for large-scale renewable energy projects.

These auctions have driven down costs and increased market efficiency. Furthermore, Germany introduced a sliding feed-in premium (FIP) to encourage renewable producers to sell electricity directly into the market, with a premium paid to bridge the gap between market prices and the guaranteed price under the feed-in tariff system.

Germany’s experience demonstrates that while FIT can kickstart renewable energy development, it is essential to transition to more market-oriented mechanisms as the sector matures. Taiwan could follow suit by implementing auction systems for large-scale renewable projects and introducing premium schemes to align market demand with renewable energy generation.

.jpg)

Germany shifted from feed-in tariffs ensuring fixed payments for renewable energy producers to a market-driven model using competitive auctions for large-scale projects. (Photo: unsplash)

Looking ahead: Taiwan’s renewable energy future

Taiwan’s renewable energy market faces significant challenges, but it also has immense potential. To achieve its renewable energy targets and meet its decarbonization goals, Taiwan must address the supply uncertainty, uneven distribution, and price rigidity that currently stifle the market.

One of the key changes needed is the establishment of a wholesale market for electricity. A wholesale market would improve price transparency, facilitate competition, and create market-aligned pricing, thereby increasing the efficiency of Taiwan’s renewable energy sector. Additionally, Taiwan could benefit from introducing a CfD scheme and sliding premiums to encourage more efficient and cost-effective renewable energy development.

In conclusion, while Taiwan has made impressive strides in renewable energy generation, there is still much to be done to ensure that the market is competitive, transparent, and aligned with market demand. By learning from international experiences and implementing new mechanisms, Taiwan can build a robust and sustainable renewable energy market that meets both its energy and environmental goals.