ASEAN is rich in solar and wind resources. Scaling up renewables offers a viable, cost-effective path to sustainable data center growth.

(Image: iStock)

As Southeast Asia races to cement its place as a global digital powerhouse, its data center industry is expanding at breakneck speed. Yet this growth may carry a heavy carbon price tag. Without urgent action, ASEAN’s rising data center demand risks derailing national and region-wide clean energy ambitions.

Data centers are projected to account for between 2% and 30% of national electricity consumption in the top 5 data center country hubs in ASEAN by 2030. Malaysia alone could see a sevenfold increase in electricity use from data centers, catapulting emissions from 5.9 MtCO2e in 2024 to 40 MtCO2e in 2030.

Strategic opportunity: Solar and wind to the rescue

ASEAN has no shortage of renewable resources. New analysis shows that solar and wind could meet 30% of data centers’ power demand by 2030 without the need for costly battery storage solutions — a critical insight, given concerns about the high cost of storage.

Scaling renewables is a viable, cost-effective pathway for sustainable data center growth. Malaysia’s Peninsular grid, Indonesia’s Java-Madura-Bali (JAMALI) grid, and the Philippines’ grid all have immense untapped clean energy potential.

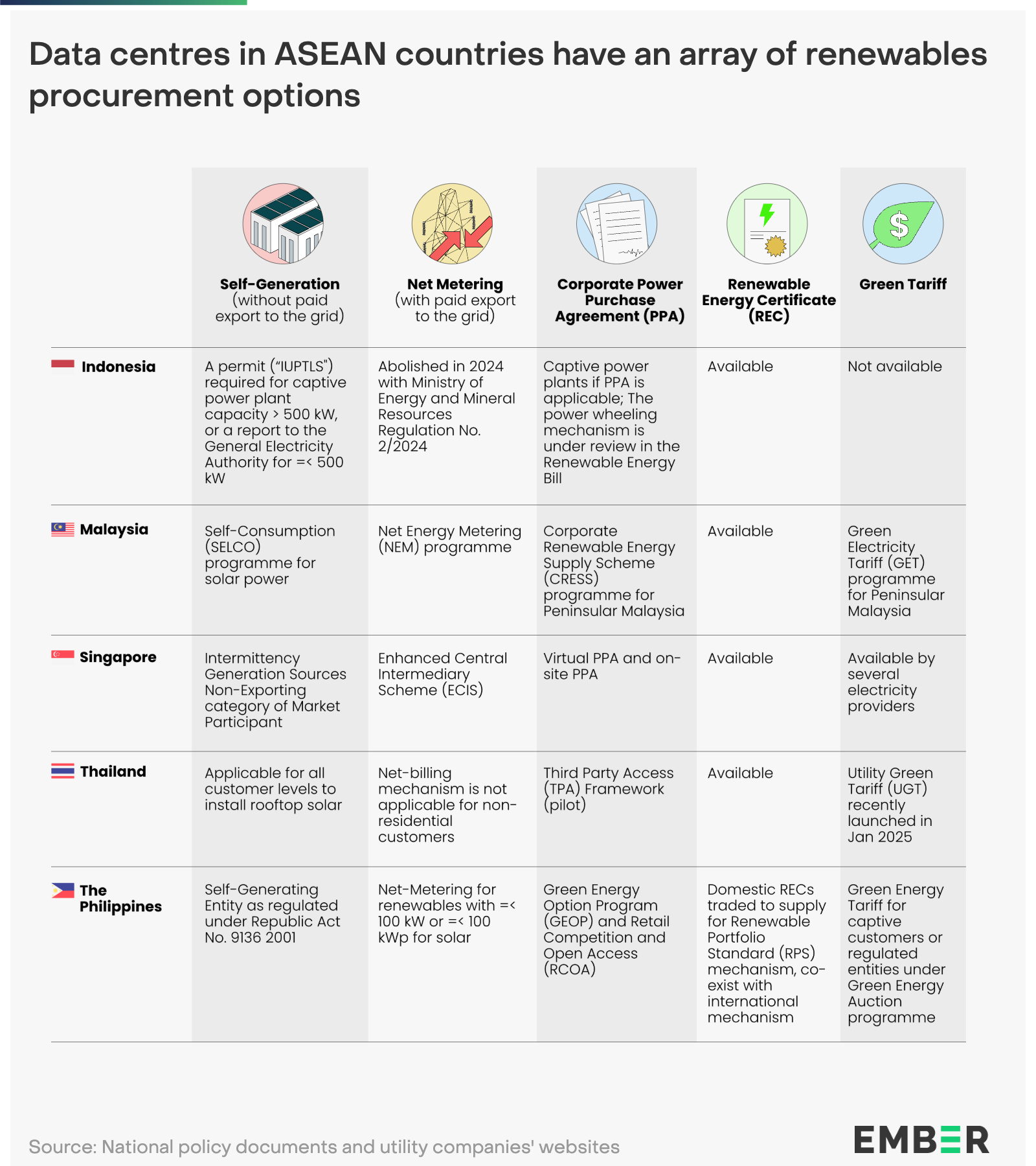

However, there should be avenues to explore a wider range of renewable procurement. Current corporate options are primarily focused on unbundled RECs, which offer poor additionality and expose buyers to price volatility. Broader access to virtual PPAs and green tariffs mechanisms should be prioritised to allow both hyperscalers and smaller providers to go green affordably.

Regional cooperation, innovative financing, and enabling regulations will be key to unlocking private sector investment in grid-connected clean power projects.

Global tech companies — Amazon, Meta, Google — have set ambitious 100% renewable energy targets. However, achieving these goals in ASEAN remains a challenge. In 2023, only 0.15% of Google’s Southeast Asia electricity consumption was sourced from renewables.

This indicates that renewables are not yet sufficiently accessible for corporates to meet their renewables target.

Bridging the gap between renewable potential and private demand

The regions hosting ASEAN’s leading data center hubs are endowed with abundant solar and wind resources—an untapped advantage in the race to decarbonize digital infrastructure. Indonesia’s Java-Madura-Bali and Batam grids alone hold a combined potential of 69 GW in solar and nearly 5 GW in wind. In Malaysia, the Peninsular grid—home to the fast-growing Johor data center cluster—has an estimated 14 GW of solar potential.

Meanwhile, Singapore, the Philippines, and Thailand benefit from fully interconnected national grids, enabling data centers to tap power from across the country. Their solar potential varies widely, from Singapore’s modest 2 GW to the Philippines’ vast 191 GW and Thailand’s 100 GW, with additional wind capacity of 22 GW and 4 GW in the latter two countries, respectively.

Unlocking this potential will require more than recognition—it demands speed. Accelerating solar and wind deployment is the clearest path to cleaning up grid electricity. But the key question remains: how do we turn these resources into real power? It is no longer about availability, but accessibility. The answer lies in strategic private sector involvement. Mobilising capital at scale will be essential, and that means governments must create the right investment climate—stable policy, streamlined permitting, and viable long-term procurement mechanisms.

Corporate Power Purchase Agreements (PPAs) offer companies long-term price certainty and a dependable supply of clean electricity, often bundled with environmental benefits like Renewable Energy Certificates (RECs) or carbon credits. Crucially, these agreements help finance new renewable energy projects. However, access to PPAs remains limited in many ASEAN markets, and navigating the negotiation process can be time-consuming. In Singapore, for instance, some firms resort to sourcing PPAs from overseas projects to meet their sustainability targets due to domestic constraints.

Countries like Malaysia, Singapore, Thailand, and the Philippines, which offer a broader mix of PPAs and green tariffs schemes, also see more competitive pricing for renewables. Malaysia’s government introduced a Third Party Access (TPA) scheme in September 2024, named the Corporate Renewable Energy Supply Scheme (CRESS) programme, targeting not only domestic but also regional buyers.

Singapore, meanwhile, supports both off-site PPAs, where consumers purchase solar power generated elsewhere in the country, and on-site solar PPAs or leasing schemes, which involve installing rooftop solar directly on customer premises. These mechanisms not only improve access for corporate buyers but also strengthen the commercial case for investing in new renewable energy capacity.

Indonesia, by contrast, has yet to implement green tariffs or a power wheeling mechanism—tools that would allow independent producers to sell electricity directly to users by using grid infrastructure. Enabling shared access to the grid could attract more private investment without overburdening national budgets.

Additionally, diversifying procurement options can support the integration of storage technologies, such as batteries. With the right tariff structures and market incentives, energy storage can enhance grid reliability and maximise the use of intermittent renewables.

Governments should not solely rely on unbundled Renewable Energy Certificates (RECs), a widespread but limited solution, exposing companies to price volatility risks. To align private sector demand with regional energy ambitions, governments must urgently scale up enabling policies: virtual PPAs, competitive green tariffs, power wheeling frameworks, and public-private collaboration.

Without strong policy intervention, ASEAN's clean energy transition will remain out of reach. Nations must accelerate the deployment of solar and wind to secure their digital infrastructure’s sustainability and resilience. Otherwise, they risk locking in fossil-based growth for decades.

In short, ASEAN has the renewable resources and the demand to drive a clean digital future. What’s needed now is decisive policy action to connect the two.

Have insights on energy or carbon issues? Share your perspective with us! Send your submission to reccessary@gmail.com for a chance to be featured. Submissions may be edited for clarity and style.

.jpg)