This year’s Carbon Forward Asia, the leading annual carbon market event in the Asia-Pacific, examines policy trends, market liquidity, and challenges in Singapore, Malaysia, Vietnam, and Indonesia. (Photo: Carbon Forward)

Carbon Forward Asia concluded its two-day conference in Singapore on March 5, bringing together government officials, corporate leaders, investors and experts to discuss the latest developments in Southeast Asia’s carbon markets.

Reccessary covered the event on-site, providing businesses with firsthand insights into Southeast Asia’s rapidly evolving carbon market landscape.

This year’s discussions centered on policy developments, market liquidity, and challenges in Singapore, Malaysia, Vietnam, and Indonesia. Delegates also examined the regional impact of Article 6 of the Paris Agreement and how countries are responding to increasingly stringent emissions reduction requirements.

Singapore: Carbon tax fuels market growth; trading boosts liquidity

Singapore, a front-runner in Southeast Asia’s carbon market development, has established a comprehensive carbon pricing framework. The country raised its carbon tax in 2024 from SGD 5 per tonne to SGD 25, with further increases planned to SGD 45 in 2026 and an estimated range of SGD 50 to 80 by 2030. This pricing policy aims not only to drive decarbonization in carbon-intensive industries but to help stabilize prices.

Representatives from AirCarbon Exchange (ACX) and Climate Impact X (CIX), Singapore's two major carbon trading platforms, pointed out that market liquidity is a key concern. While ASEAN countries are actively developing their own trading mechanisms, Singapore’s system is already mature, positioning the nation as a potential carbon trading hub for the region.

To enhance transparency, ACX is promoting standardized contracts aligned with international methodologies and credit standards. Meanwhile, CIX emphasized the importance of market efficiency and liquidity. Both exchanges play vital roles in price discovery and attracting foreign investors, with liquidity set to improve as more buyers enter the market.

Malaysia: Slow voluntary market development hampers corporate participation

Compared to Singapore, Malaysia’s carbon market remains in its early stages. While the government is actively promoting the development of a voluntary carbon market, participation levels remain low. A lack of clarity around carbon credit verification mechanisms and an evolving regulatory framework have left companies and developers hesitant to engage

Despite its abundant natural resources, Malaysia lacks methodologies aligned with international standards, and the high cost of project development and verification continues to discourage investment. At present, the Kuamut Rainforest Conservation Project (KRCP) is the only certified nature-based carbon project in the country, with credits priced at USD 12 per tonne (see Table 1). How to attract international investors will be a critical challenge for policymakers as the market matures.

(1).jpg)

Table 1. Historical overview of carbon credit auctions in Malaysia

Indonesia: Market opened to foreign companies in hopes of boosting trading activity

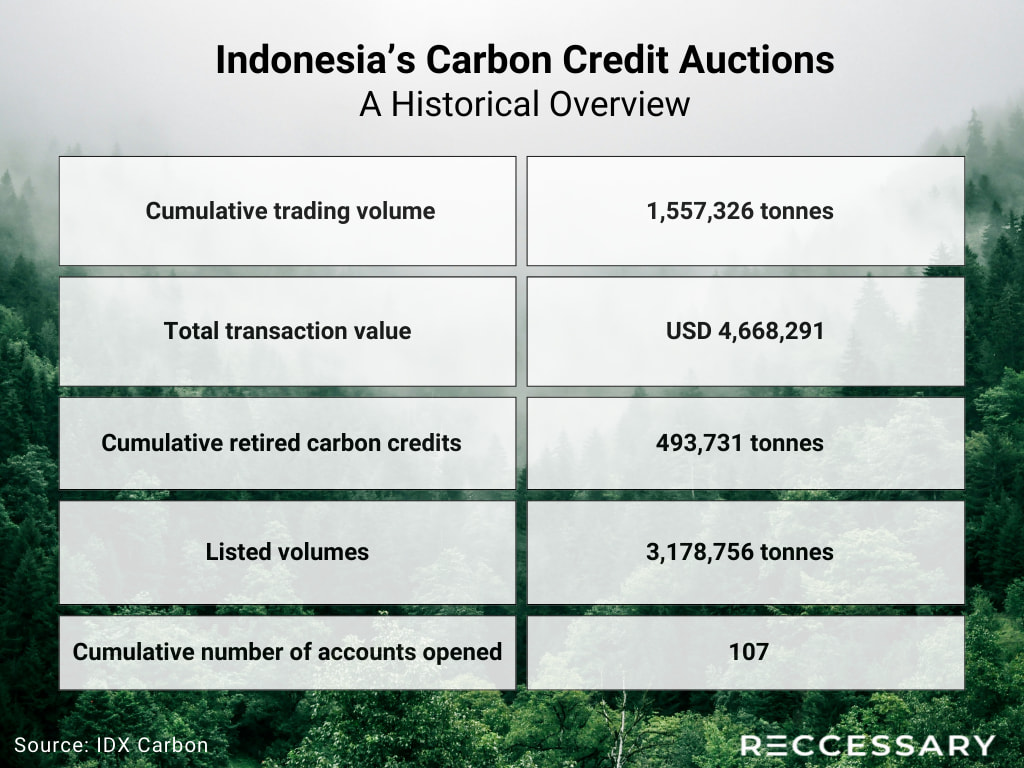

Indonesia officially initiated its carbon exchange, IDX Carbon, in September 2023, becoming one of the front runners to implement carbon trading. As of February 21, 2025, the Indonesian carbon market had recorded a cumulative trading volume of 1.55 million tonnes, with total transaction value exceeding USD 4.66 million. The volume of retired carbon credits also showed steady growth, reaching 490,000 tonnes (see Table 1). To date, five carbon credit projects have been listed, including those of renewable energy and energy efficiency (see Figure 2).

Table 1. Historical overview of carbon credit auctions in Indonesia

Figure 2. Share of carbon credit listed in Indonesia by type (Source: IDX Carbon)

Since January this year, Indonesia’s carbon exchange has allowed foreign entities to purchase carbon credits on its platform, a move expected to stimulate market activity. In addition, Indonesia’s Emissions Trading System (ETS) expanded its regulatory scope this year and is expected to cover more than 80% of the country’s greenhouse gas emissions. The compliance and voluntary markets will together drive the long-term developments of Indonesia’s carbon market.

Vietnam: Regulatory framework gradually improving, whereas market mechanisms remain underdeveloped

Vietnam’s Ministry of Natural Resources and Environment plans to launch a nationwide Emissions Trading System (ETS) in 2028, with pilot phase set to begin in June 2025. Emission reporting has begun across various industries. In 2022, the power and heat generation sector accounted for the highest share of the country’s emissions, followed by the industrial sector (see Figure 3).

According to Vietnam’s carbon pricing regulations, the first phase of the ETS will cover facilities with annual emissions above 3,000 tonnes, including geothermal, steel, and cement sectors—an estimated 150 corporates in total. However, the market still faces challenges such as limited awareness of carbon pricing and an incomplete regulatory framework, which will require joint efforts from both government and the private sector to address.

Figure 3. Share of Vietnam’s CO2 emissions by sector in 2022 (Source: International Energy Agency)

Regional market outlook: Standardization and collaboration are key

During the conference, experts discussed the impact of Article 6 of the Paris Agreement, which allows countries to cooperate through Internationally Transferred Mitigation Outcomes (ITMOs). The mechanism is seen as a major driver for carbon market development in Southeast Asia. Singapore, in particular, has taken the lead by actively engaging in cross-border carbon credit trading under Article 6, signing agreements with Bhutan, Papua New Guinea, and Ghana.

Singapore has launched its second round of Requests for Proposals (RFPs), committing to the purchase of international carbon credits under Article 6. Meanwhile, Indonesia and Vietnam are assessing how to leverage the mechanism to access international funds. However, challenges remain regarding implementation, including the need for clear regulations, market integration mechanisms, and effective corresponding adjustment frameworks.

To promote ASEAN carbon market integration, the ASEAN Common Carbon Framework (ACCF) has been introduced and made its official debut at COP29 in 2024. Led by Malaysia, the initiative aims to advance standardization and regulatory cooperation across the region to improve market liquidity and transparency.

The formation of ACCF signals a move toward closer regional collaboration. How ASEAN countries align methodologies and standards with international frameworks will be a key focus moving forward, and policy developments in the coming years will determine the region’s potential role in the global carbon market.

.jpg)