.jpg)

(Photo: iStock)

As climate change intensifies, nations worldwide are implementing carbon pricing policies to curb greenhouse gas emissions. For Taiwanese businesses, adapting to carbon fee policies and effectively implementing decarbonization strategies has become crucial. The cement industry, a significant contributor to carbon emissions, faces mounting pressure to adapt. This report explores the effects of carbon fees on the cement sector and outlines strategies for adaptation.

Why must the cement industry lead in decarbonization?

The cement sector accounts for approximately 7% of global greenhouse gas emissions due to its production processes, which involve burning limestone and coal. Over 80% of its emissions stem from Scope 1 and Scope 2 sources, meaning the industry has substantial control over its emissions through operational and process improvements.

As a primary target of Taiwan’s first phase of carbon fee implementation, the cement industry faces direct challenges. Proactively adopting decarbonization measures will help mitigate the impact of carbon fees. But how significant is this impact, and how should the industry respond?

Evaluating the impact of carbon fees on the cement industry

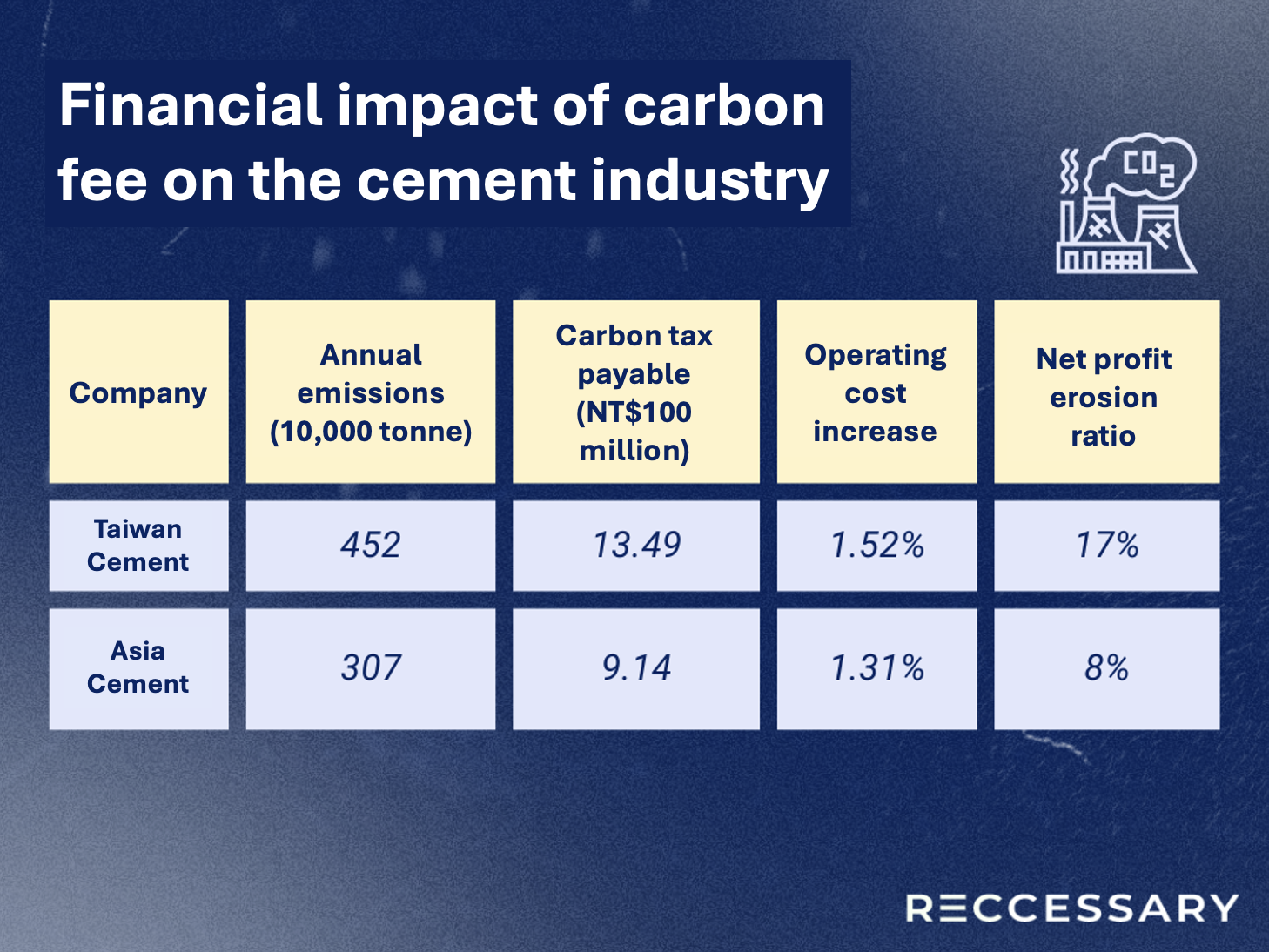

Taiwan’s carbon fee policy exempts emissions below 25,000 tons and imposes fees based on set rates. According to the Ministry of Environment, the cement industry includes five major emitters, such as Taiwan Cement and Asia Cement.

Financial impact assessment

Based on 2023 financial data, if carbon fees are set at NT$300 per ton with a 25,000-ton exemption:

- Taiwan Cement would face a carbon fee of NT$1.3 billion annually.

- Asia Cement would incur approximately NT$900 million.

These costs would increase operating expenses by at least 1% for both companies.

When factoring in net profits, carbon fees could erode profits by 17% and 8%, respectively, underscoring the significant financial strain carbon pricing could impose.

Table 1. Financial impact of carbon fees on the cement industry

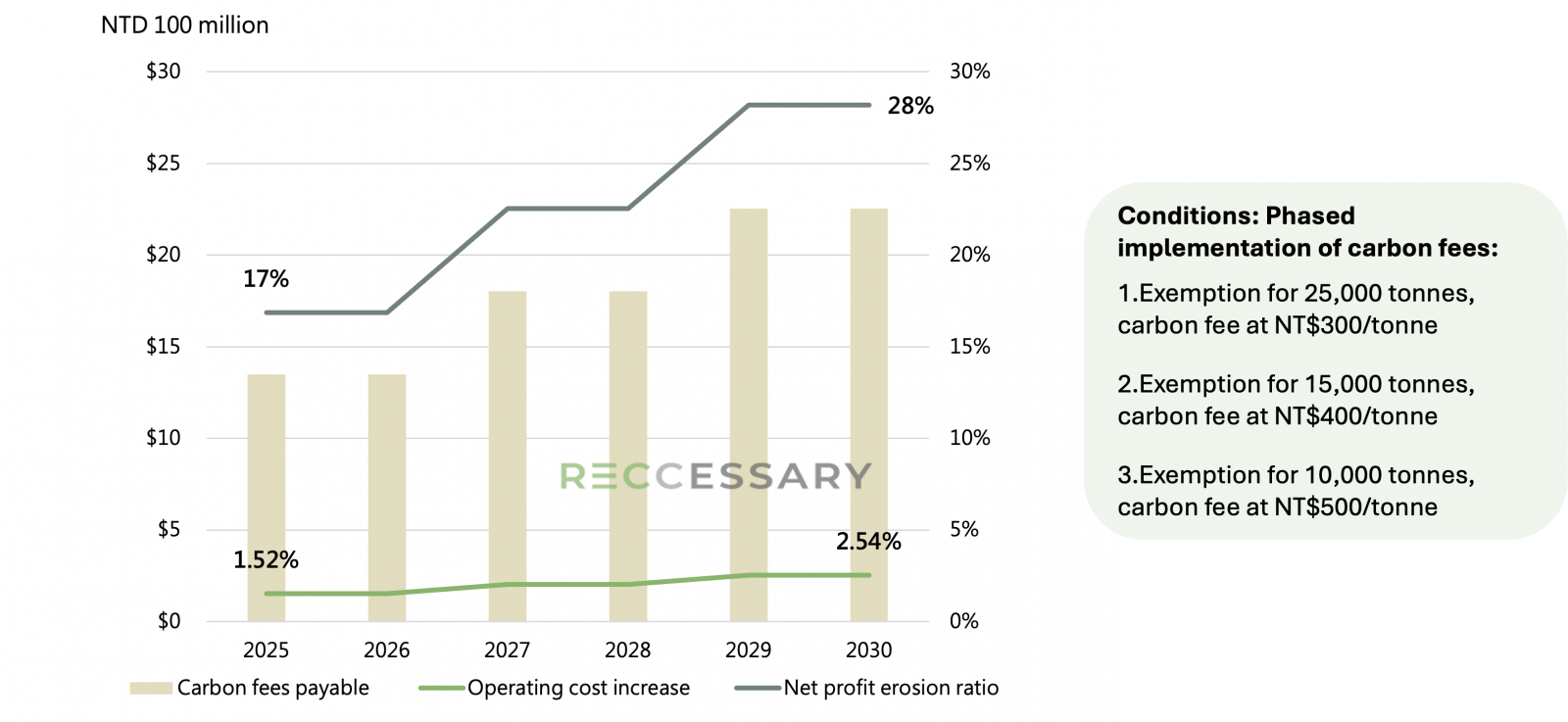

Long-term projections

If carbon fees rise to NT$500 per ton by 2030, carbon costs for a representative company could escalate from NT$1.3 billion to NT$2.3 billion—a 70% increase. This would result in:

- A 28% reduction in post-tax profits.

- A 2.54% rise in operating costs.

Figure 1. Impact of carbon fee policy on carbon costs for non-decarbonizing companies

These projections highlight the growing financial burden of carbon pricing on businesses without decarbonization measures.

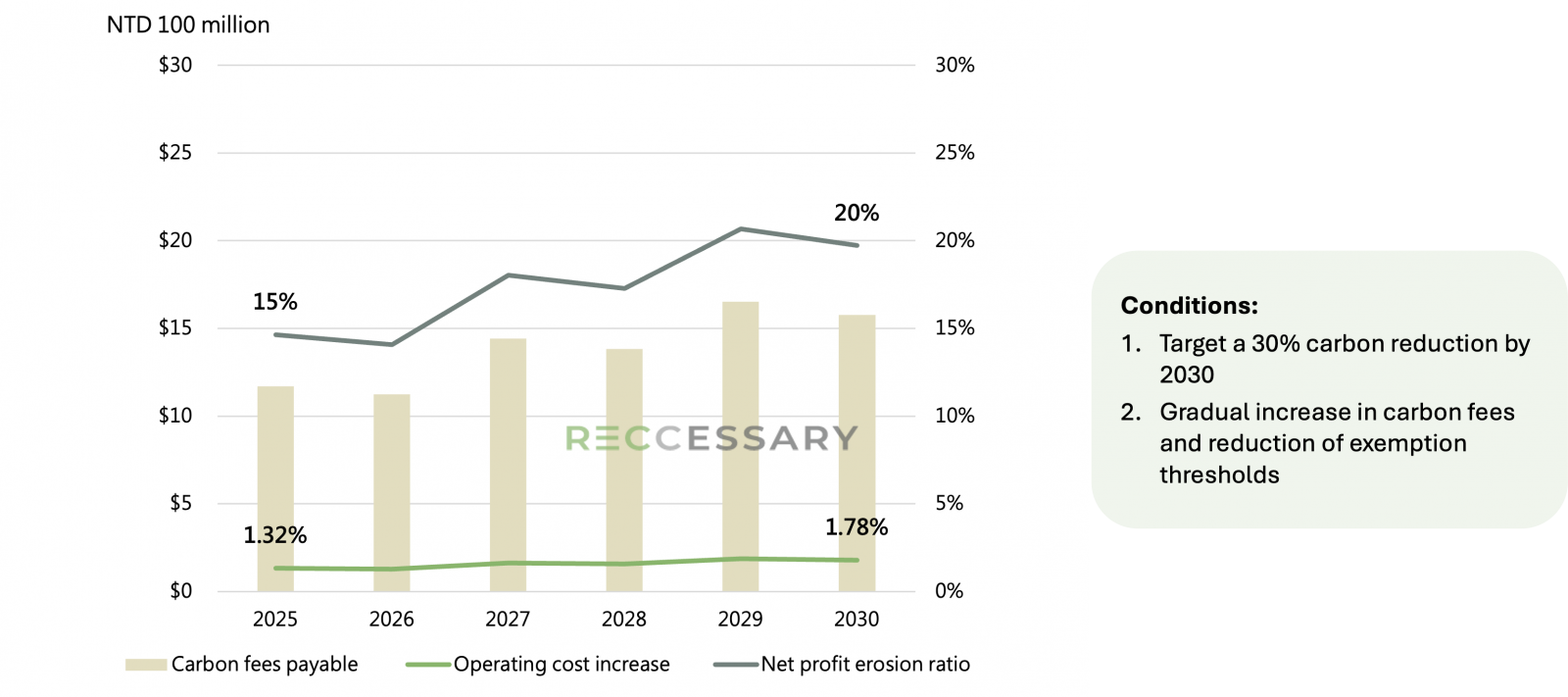

Mitigation through decarbonization

Implementing decarbonization measures could significantly reduce carbon costs. For example, achieving a 30% reduction in emissions by 2030 could lower carbon fees by an equivalent percentage, providing financial relief and reinforcing competitiveness.

Figure 2. Impact of decarbonization measures on carbon costs

Strategic responses for the cement industry

Faced with these challenges, cement companies must adopt proactive strategies across three main areas:

1. Addressing major emission sources

Over 90% of emissions in cement production occur during clinker calcination and coal combustion. Key measures include:

- Enhancing energy efficiency during the calcination process.

- Using cleaner alternative fuels or low-carbon limestone.

- Optimizing production methods to reduce emissions.

2. Innovating products and business models

To address carbon fee pressures, companies should focus on:

- Low-carbon product development: For instance, Asia Cement’s low-carbon cement products reduce emissions by 13–16%, while Taiwan Cement’s clay-blended clinker alternative lowers emissions by 40%.

- Circular economy initiatives: High-temperature cement kilns enable waste recycling, such as incorporating steel slag and fly ash as raw materials. This reduces production costs, improves resource efficiency, and aligns with sustainability goals.

3. Upgrading equipment and advancing technology

Energy efficiency improvements through equipment upgrades include:

- Installing renewable energy systems.

- Introducing digital management systems.

- Transitioning to electric vehicles.

Investments in negative-carbon technologies, such as calcium looping carbon capture developed by Taiwan Cement and the Industrial Technology Research Institute, offer cost-effective solutions compared to conventional methods. Though challenging, combining such technologies with other decarbonization measures could help achieve carbon neutrality.

Implications for the cement industry in a carbon-priced era

The era of carbon pricing poses dual challenges: adapting to policy requirements and achieving meaningful decarbonization. Cement companies must develop comprehensive strategies to remain competitive in this landscape. Failure to act will not only hinder green competitiveness but also result in financial penalties, eroding profitability and market position.

Moreover, the absence of carbon pricing or taxation on imported cement may create an uneven playing field, exacerbating the impact on domestic producers. To sustain operations in a carbon-conscious economy, the industry must:

- Implement solutions targeting major emission sources.

- Pursue product innovation and technical upgrades.

- Adopt sustainable business practices through circular economy initiatives.

By accelerating these efforts, the cement sector can navigate the challenges of carbon pricing and secure long-term viability in a decarbonized future.