The Asia Climate Summit (ACS), held by IETA, is one of the most prominent carbon market conferences in Asia. (Photo: IETA)

The annual Asia Climate Summit (ACS), hosted by the International Emissions Trading Association (IETA), one of the world’s three major carbon market organizations, is among the most influential carbon market gatherings in Asia. This year’s summit took place in Bangkok from July 8 to 10, drawing more than 900 delegates from international organizations, businesses, and governments, including the United Nations, World Bank, and Google.

RECCESSARY attended the event and, based on discussions with developers, institutional investors, and experts, summarized three major trends and opportunities shaping Asia’s carbon markets.

Trend 1: Too many methodologies spark anxiety, unified standards in demand

The voluntary carbon market is expanding rapidly worldwide, but its fragmentation and lack of unified standards have become a central concern at this year’s summit. Developers, certification bodies, and investors noted that methodologies are still governed separately by different standard-setters such as Gold Standard and the Climate Action Reserve (CAR), making it difficult for projects to comply with multiple requirements and significantly raising verification and communication costs.

For instance, if a developer uses Gold Standard’s methodology, the resulting carbon credits cannot be directly listed on other registries such as Verra, creating substantial barriers to market entry.

Although mechanisms such as the Integrity Council for the Voluntary Carbon Market’s (ICVCM) Core Carbon Principles (CCP) label and Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) have been introduced to improve the quality and verification of carbon credits, they have yet to address the underlying issue. Many participants at the summit stressed that the market urgently needs a more authoritative and unified framework.

Article 6.4 of the Paris Agreement, overseen by the United Nations Framework Convention on Climate Change (UNFCCC), is seen as one potential solution. With its foundation of international legitimacy, it could play a key role in establishing unified standards and rebuilding market trust. The mechanism could both reduce the risks developers face in aligning with multiple standards and support countries in achieving their nationally determined contributions (NDCs).

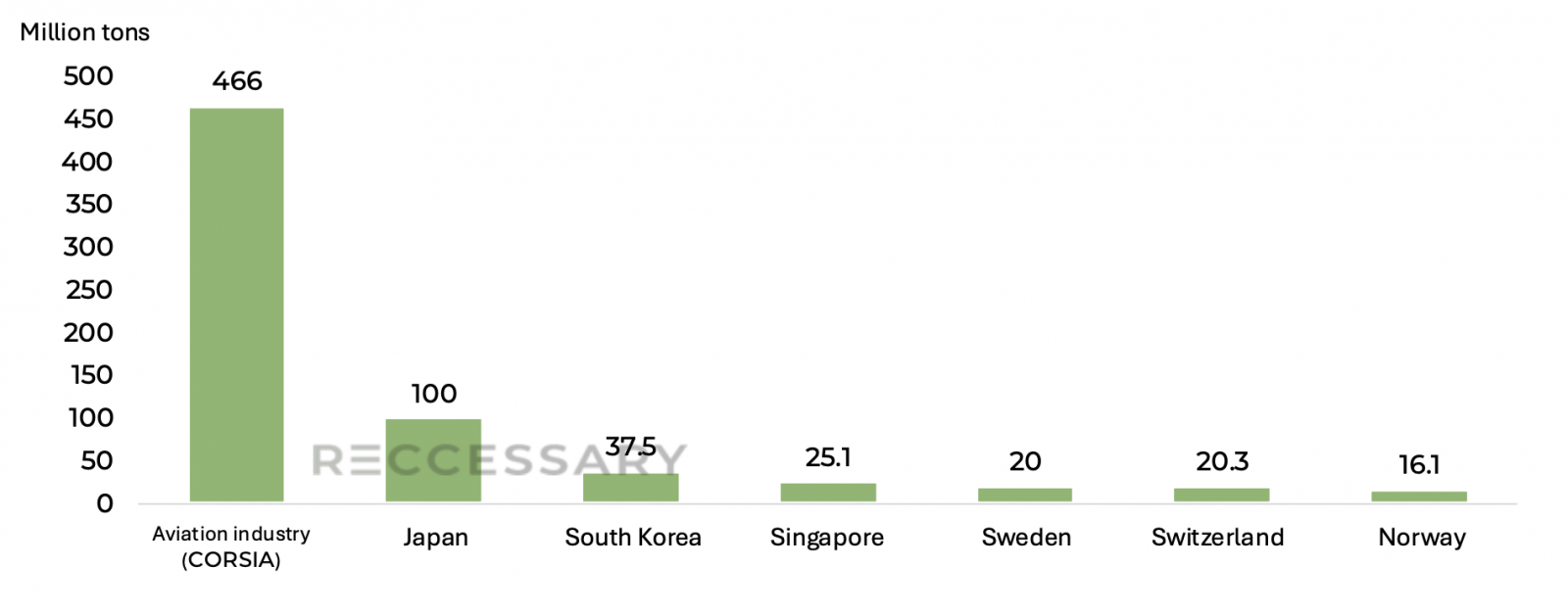

Figure 1. Projected demand for Internationally Transferred Mitigation Outcomes (ITMOs) by 2030 [1]

Trend 2: ASEAN advances regional cooperation on carbon markets

At the event, President Asadej Kongsiri of the Stock Exchange of Thailand said that ASEAN countries should work together and jointly invest in the carbon market. While ASEAN does not have a unified carbon market like the EU, most member states have recognized the importance of carbon pricing and are in the process of establishing their own systems.

Thailand: Positioning Premium T-VER as ASEAN’s carbon credit standard

Thailand has implemented the Thailand Voluntary Emission Reduction Program (T-VER) since 2014 and introduced in 2022 an upgrade version, Premium T-VER, designed to better aligned with international standards. The government now plans to seek recognition under CORSIA and the CCP label.

According to Thailand’s Department of Climate Change and Environment (DCCE), the country aims to elevate Premium T-VER to the international stage through adopting more stringent verification standards, positioning it as a primary reference for carbon issuance in ASEAN.

At present, 526 projects have been registered under T-VER, with an expected annual reduction of 1.41 million tons of CO2 equivalent. By comparison, Premium T-VER has four registered projects, with 19,517 tons of carbon credits expected to issue annually. As DCCE continues to promote the new program, stakeholders are closely watching whether Thailand could emerge as a leading supplier of carbon credits in ASEAN.

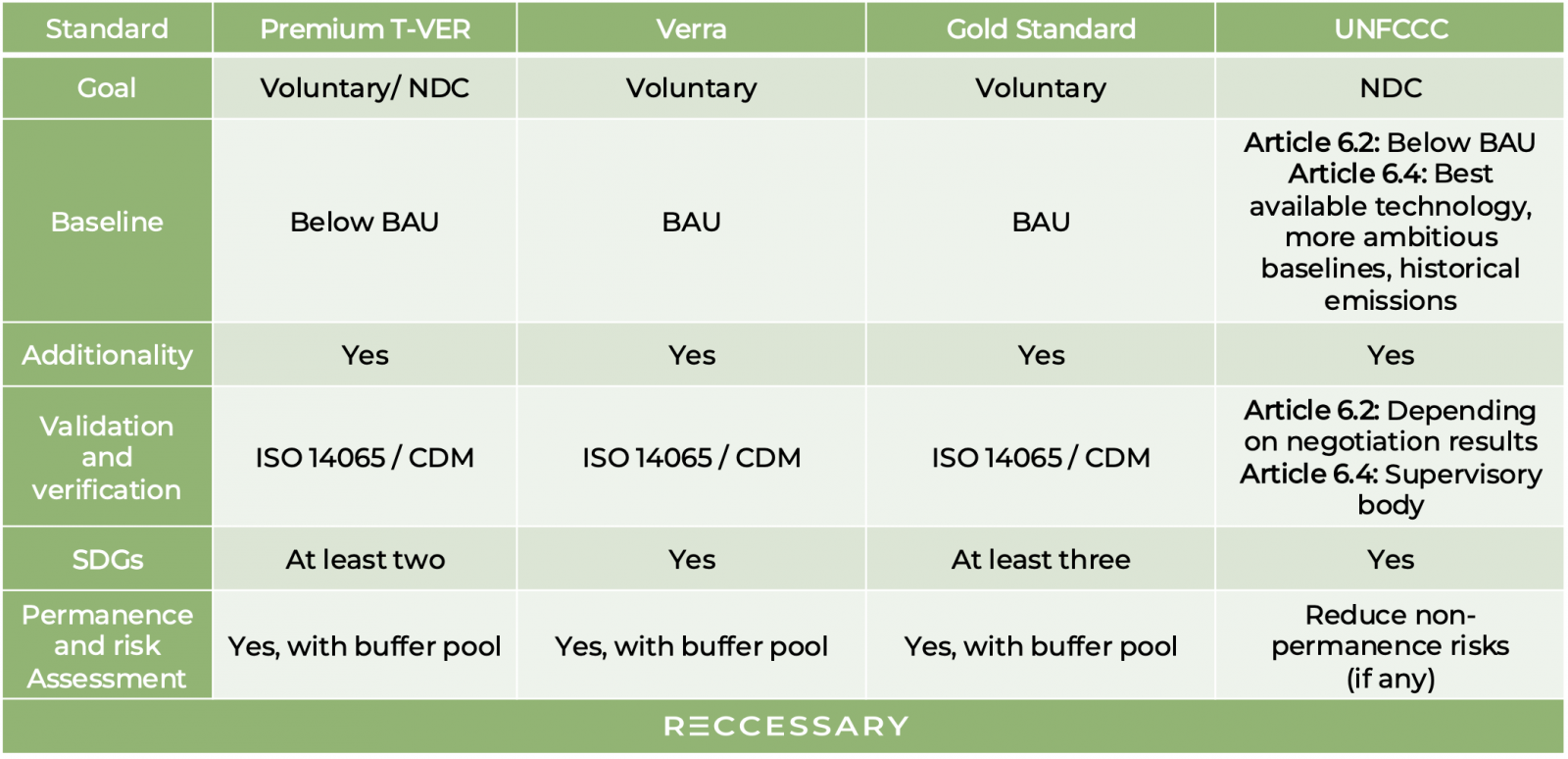

Figure 2. Comparison of Thailand’s Premium T-VER and international standards [2]

Vietnam and Indonesia: Expanding carbon market ambitions but tightening for foreign investors

Vietnam and Indonesia continue to stress their commitment to achieving national NDC targets and are accelerating the pace of domestic greenhouse gas inventories. However, close examination shows that two major entry barriers remain for foreign investors: difficulties in land acquisition and policy risks.

Vietnam is among Japan’s top three partners in the Joint Crediting Mechanism (JCM) in Southeast Asia, after Indonesia and Thailand, and the two sides have long pursued active carbon diplomacy. Recently, however, Vietnam has moved to tighten land-use conditions, giving priority to domestic developers. Several Japanese companies at the summit noted that in recent years it has indeed become more difficult to advance carbon projects in the country.

Indonesia, on the other hand, has seen frequent changes in carbon policies, raising barriers to market entry. In 2022, the government banned the sale of domestically developed credits on international platforms. With the recent lifting of that measure, and a mutual recognition agreement (MRA) signed in May between the Ministry of Environment and Forestry and Gold Standard, protectionist attitudes appear to be easing. However, under Regulation No. 21/2022, it is still clear that Indonesia intends to keep development activities largely domestic [3]. Investors are therefore advised to closely monitor shifts in local policies and regulations.

ASEAN’s carbon market cooperation remains in its early stages, but with regional organizations and associations facilitating dialogue, countries such as Thailand, Malaysia, and Singapore have expressed strong interest, suggesting significant potential. However, with the Philippines set to assume the ASEAN chairmanship in 2026, short-term policy directions could face uncertainty.

Trend 3: Carbon finance becomes key as projects must prove bankability

On carbon project financing, representatives from financial institutions such as Mitsubishi UFJ Financial Group (MUFG) and UK-based Climate Asset Management agreed that project feasibility now outweighs internal rates of return. They pointed to three key indicators:

- Political risk: The hardest to predict, with the widest potential impact.

- Price volatility: Whether short- and long-term trends can be forecast and how budgets are set.

- Project performance: Including the choice of methodology, deliverability of outcomes, and the design of risk control mechanisms.

Beyond financial returns, many financial institutions place greater emphasis on the feasibility of carbon projects. (Image: iStock)

For banks and investors, even if carbon prices are expected to rise, developers that cannot demonstrate stable cash flows or robust monitoring, reporting, and verification (MRV) mechanisms will struggle to secure loans or investment commitments. In other words, future access to capital will depend less on projected financial returns alone and more on long-term credibility that can win investor trust.

At the summit, many participants stressed that regional cooperation in carbon markets is urgently needed. Building a complete mechanism will require trust, regulatory clarity, and climate finance as key foundations. The discussions showed that Asia is working to build bridges for cooperation. Although countries are moving at different paces, there is strong willingness to collaborate. For Taiwan, engaging in the emerging ASEAN market will be essential to seize critical investment opportunities early.

Note

[1] Source: IETA. Under Article 6.4, carbon credits must be authorized by the host country and subject to corresponding adjustments before they can be converted into ITMOs.

[2] Source: Thailand Greenhouse Gas Management Organization (TGO).

[3] For example, in the setting of carbon buffers: 5% for domestic projects and 10–20% for overseas projects.

.jpg)