The development of the global carbon market has received widespread attention. Carbon Forward Asia held on March 7 and 8 in Singapore gathered industry experts and scholars to discuss the current market situation and future trends. Participants from Singapore, Malaysia, China, South Korea, and the EU focused on two major topics: the development of carbon markets in the Asia-Pacific region and the future of the global voluntary carbon market.

Divergence in Southeast Asia's carbon pricing systems

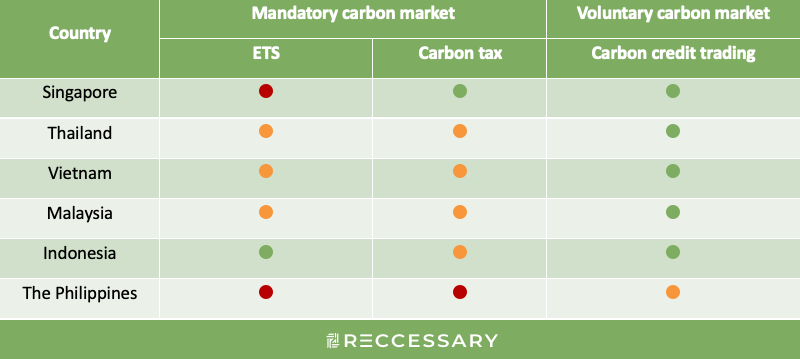

Globally, the carbon market in the Asia-Pacific region is gradually maturing, but the carbon-related mechanisms in Southeast Asia remain quite fragmented. Unlike the EU Emissions Trading System (EU ETS), Southeast Asia has developed its own rules for carbon pricing. Table 1 outlines the implementation status of carbon pricing tools in various regions, including Emissions Trading Systems (ETS), carbon taxes, and carbon trading.

Table 1: Carbon Pricing Tools in Southeast Asia

Reviewing Southeast Asia's carbon pricing mechanisms reveals that each country adopts slightly different strategies. Indonesia, as one of the world's top ten greenhouse gas emitters, is the first country in the region to establish an ETS. Compared to government-led mandatory carbon markets, voluntary carbon markets, primarily focusing on carbon offsetting, are favored by many Southeast Asian countries. For example, Malaysia's Bursa Carbon Exchange and Thailand's FTIX Carbon Trading Platform started operations last year. Additionally, Singapore's carbon tax system and carbon credit trading are more mature, with comprehensive regulations and market liquidity.

Differentiated strategies for Southeast Asia's carbon market

Why do Southeast Asian countries choose different market systems compared to the EU ETS, implemented since 2005? And why is the development of voluntary carbon trading markets a primary strategy? There are three main reasons behind this choice: differences in political systems, energy structures, and economic development.

1. Differences in political systems

Compared to the highly integrated EU, Southeast Asia has significant differences in policies and regulations, making it difficult to establish a unified carbon market. Furthermore, the EU has demonstrated high political will and leadership towards common emission reduction goals, while Southeast Asian countries have yet to achieve such political consistency and cooperation. Therefore, diverse carbon market models are more effective in these regions.

2. Differences in energy structures

The energy structures and emission sources in Southeast Asian countries vary. Some countries rely more on fossil fuels, while others focus more on renewable energy development. For instance, Indonesia primarily uses coal to meet its energy needs, while Vietnam has significant potential in solar and wind energy. These differences greatly influence the strategies each country adopts for their carbon markets.

3. Differences in economic development

Southeast Asian countries have varying levels of economic development and industrialization. Implementing mandatory carbon markets could significantly impact their economies. Developing voluntary carbon markets offers a flexible and liquid mechanism, allowing companies to choose whether to participate, thus incentivizing carbon trading behaviors and promoting market development.

At the conference, World Bank financing expert Jeffrey Delmon acknowledged Southeast Asia's strategy for voluntary carbon markets. Establishing a cooperative carbon market system is crucial. For example, Singapore has bilateral agreements with Indonesia and Bhutan for carbon credit transfers, and Vietnam has extended its market to the Asia-Pacific region, becoming the fourth-largest carbon project issuer under Japan's JCM mechanism. As countries gradually introduce carbon pricing systems, whether Southeast Asian carbon markets can be integrated will be a focal point.

Global voluntary carbon market status

In 2021, the voluntary carbon market's value exceeded USD 2 billion. Although the carbon credit trading volume dropped by 50% the following year, the total transaction value remained similar, indicating a rise in the price per unit of carbon. This trend is primarily due to the increasing emphasis on high-quality carbon credits.

.png)

Figure 1: Global Voluntary Carbon Market Trading Volume and Transaction Value

Three major trends in the global carbon market

The quality of carbon credits has garnered attention after several carbon credit controversies. Factors like methodology recognition, regulatory measures, carbon credit issuance, and certification are standards for quality determination. However, there is still a lack of uniformity in the international carbon credit market, and the complexity of market systems deters investors. There are three significant issues to watch in the global carbon trading market in 2024:

1. Challenges and opportunities of the Paris Agreement's Article 6

Article 6 of the Paris Agreement is key to the integrity of the voluntary carbon market, particularly Articles 6.2 and 6.4. Although consensus on Article 6.4 has yet to be reached, Article 6.2 has spurred robust development in international carbon credit cooperation. Currently, over 45 countries have signed cooperation agreements, with Singapore and Switzerland being notable examples. Singapore has agreements with Southeast Asia, Africa, and South America, while Switzerland's agreement with Thailand marks the first implementation of Article 6.2, showcasing the value of the Paris Agreement's Article 6 in providing opportunities for international cooperation.

2. Pursuit of high-quality carbon credits

The emergence of the Integrity Council for the Voluntary Carbon Market (ICVCM) and the Voluntary Carbon Markets Integrity Initiative (VCMI) has created more development opportunities for the voluntary carbon market. Additionally, the Civil Aviation Organization's CORSIA carbon credit certification standard has set higher quality requirements. International organizations' involvement helps ensure transparency and fairness in the carbon market, boosting participant confidence.

3. Need for unified market rules

Despite the growing influence of voluntary carbon markets globally, differing market systems remain a challenge. Different regions have varying understandings, rules, and enforcement methods for carbon markets, complicating market participation. Establishing consistent market rules and standards provides a guideline for companies and promotes market activity.

In summary, the global carbon market requires more regulations to collectively achieve global climate commitments. At the end of the conference, participants agreed that addressing carbon market challenges depends on international cooperation. Market participants, including carbon traders, developers, policymakers, and investors, should closely follow carbon market developments, engaging in active exchange and cooperation to promote healthy market growth.

As the impact of the carbon market grows, companies will play a more crucial role in emission reductions. Considering the different development systems of carbon markets in various regions, early planning can seize market opportunities and address challenges arising from market changes.