.jpg)

(Photo: Pixabay)

A global treaty on plastics, which is being touted as the most important environmental treaty since the 2015 Paris Agreement, is set to be negotiated in South Korea over the next week.

At the fifth and final scheduled session of the UN’s Intergovernmental Negotiating Committee on Plastic Pollution (INC-5), member countries hope to finalise and approve the text of the “international legally binding instrument on plastic pollution”.

A successful treaty could have important implications for climate change.

The production, use and disposal of plastics is responsible for around 5% of global greenhouse gas emissions and they are typically made from fossil fuels. Plastics production is expected to be one of the leading drivers of oil demand growth over the coming years.

Measures to reduce plastics use will be a key part of the agenda, as around 90% of emissions from plastics come from production. The negotiations will see countries discuss setting targets, accountability and transparency measures.

Carbon Brief analysis shows that without any agreement to cut plastic production, emissions from plastics could consume half of the remaining carbon budget for limiting warming to 1.5C above pre-industrial levels.

One expert tells Carbon Brief that the best outcome possible for the negotiations is to ratify a global target to limit plastics production, coupled with legally binding national targets.

However, she warns that oil-producing countries are likely to veto any such proposal.

Below, Carbon Brief presents five key charts showing why the plastics treaty matters for climate change.

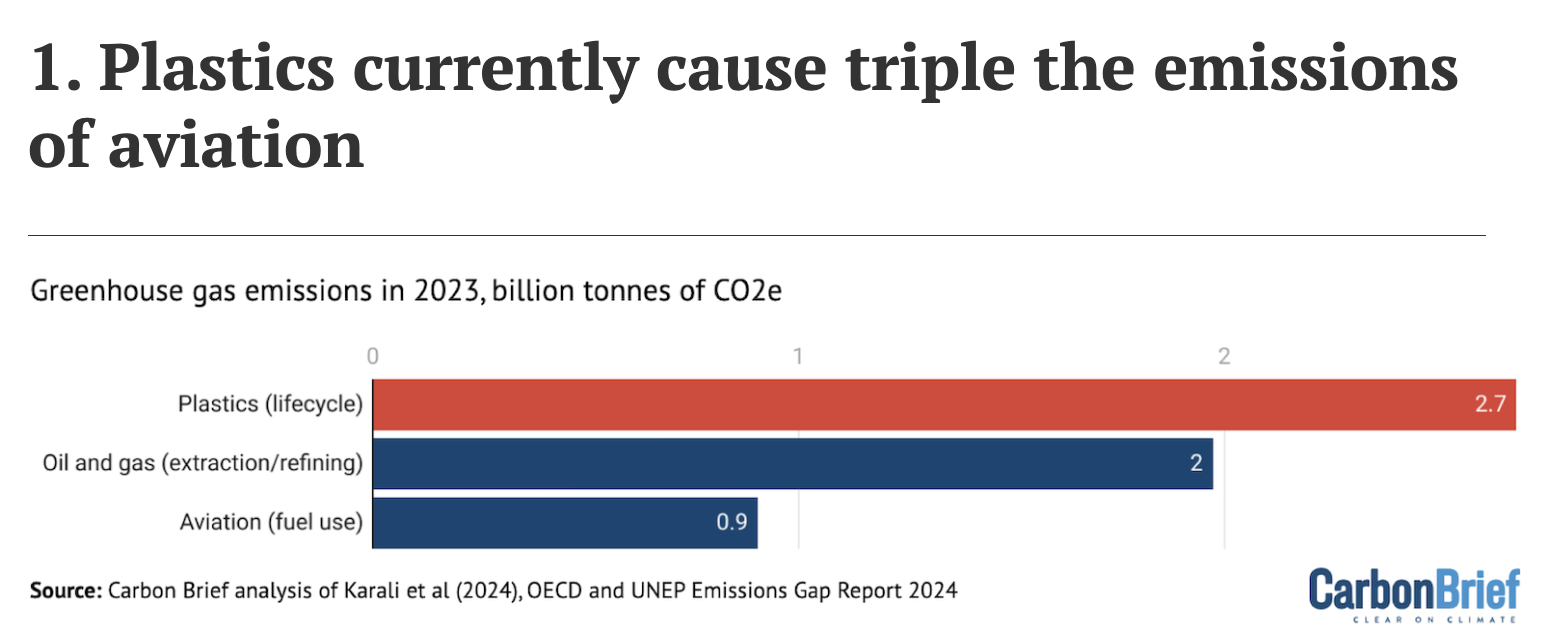

Greenhouse gas emissions in 2023, in billion tonnes of CO2e. Source: Carbon Brief analysis of Karali et al (2024), the OECD and the UNEP Emissions Gap Report (2024). Note that oil and gas (extraction/refining) includes fugitive methane emissions, and aviation only considers emissions from fuel use.

Plastics are a versatile and durable material that have revolutionised industries from fashion to medicine. However, they also cause serious environmental problems.

The most commonly discussed downside of the widespread global use of plastic is the ecosystem damage caused by waste. Even if disposed of safely, the production and disposal of plastics produce greenhouse gas emissions that contribute to global warming.

Carbon Brief calculations suggest that plastic lifecycles generated more than 2.7bn tonnes of CO2 equivalent (GtCO2e) in 2023 – around 5% of global emissions. This is roughly three times more than the emissions produced by aviation, as shown in the graphic above.

Around 90% of emissions from plastics come from production – the process of extracting fossil fuels and converting them into plastics. The world produces around 400m tonnes of plastics every year and this number is expected to grow over the coming decades.

Most plastics are made from fossil fuels, using oil, coal or gas converted into feedstock chemicals. Extracting the fossil fuels needed from underground is directly associated with greenhouse gas emissions, for example due to leaky mines, wells and pipes that contribute to rising methane emissions.

Overall, extracting oil, gas and coal from the ground accounts for around one-fifth of plastics production emissions.

The rest of the emissions associated with plastics production come from the processes required to first convert the fossil fuels into plastics. The fossil fuels are refined to produce petrochemical feedstocks, such as ethane and naphtha.

In one of the most emissions-intensive steps of the process, these feedstocks are broken apart in a high-pressure steam cracker to produce chemicals called monomers. Finally, the monomers are joined into chains called polymers, which are used to construct plastics.

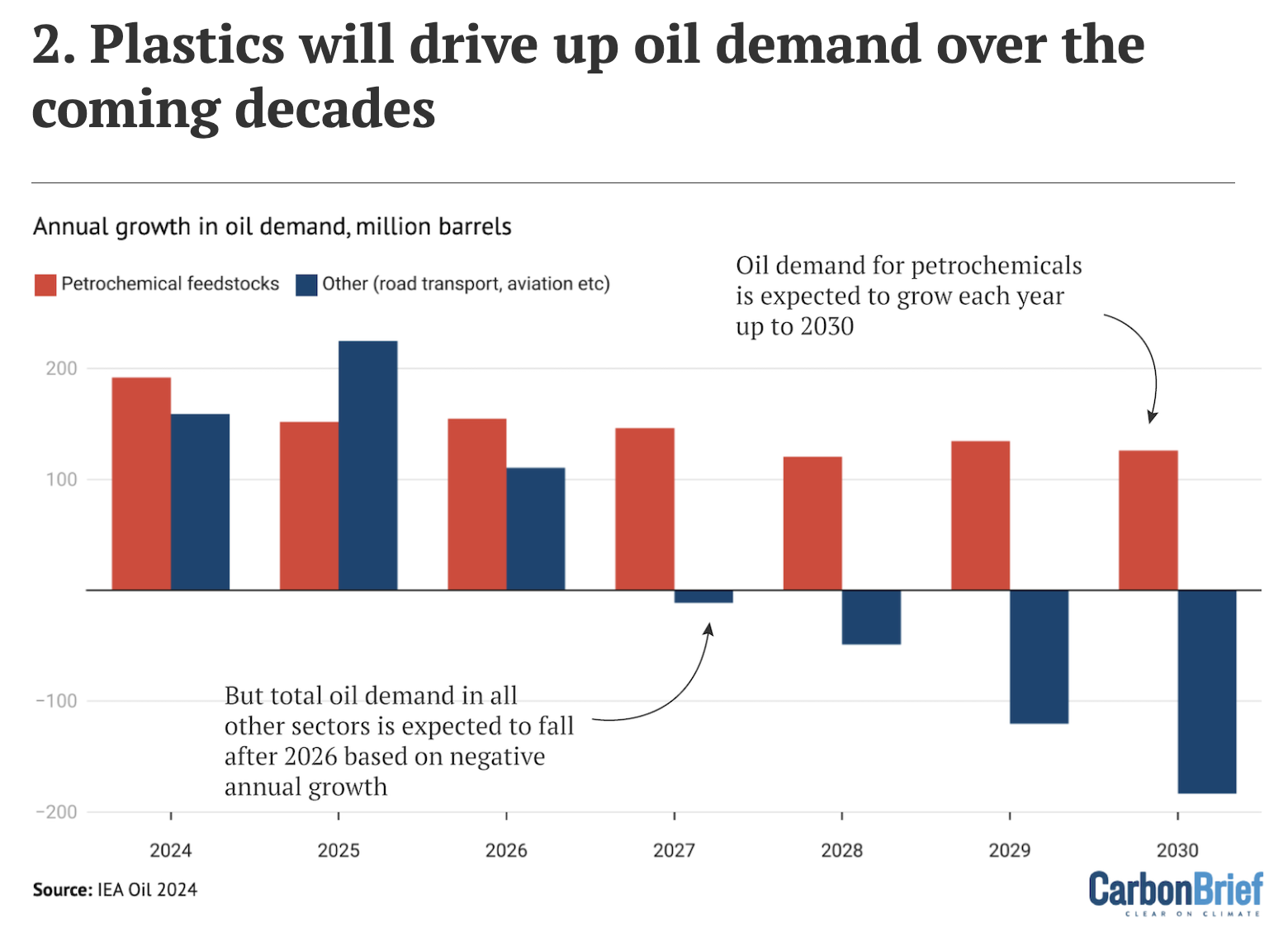

Annual growth in oil demand, in millions of barrels. Source: IEA Oil 2024 report

The world’s consumption of oil is currently around 100m barrels per day. According to an International Energy Agency (IEA) special report, around half of the oil produced globally is currently used to fuel road transport – and this is being squeezed by the rising popularity of electric vehicles (EVs).

Along with renewables substituting for oil-fired electricity generation and increasingly efficient engines, EVs are the major driver of expectations that global oil demand could soon peak.

Petrochemicals feedstocks – chemical substances derived from fossil fuels that can then be used to make products such as plastics, rubbers and fertilisers – are widely seen as the last growth market for global oil demand. As such, the future of the $700bn plastics production industry is a key concern of the fossil-fuel industry.

Currently, only 14m barrels per day are used as a petrochemical feedstock – the majority of which is used to produce plastics. But the IEA expects this to grow further in the coming years, even as demand in other sectors falls.

The figure above shows projected annual growth in oil demand from petrochemical feedstocks (red) and other sectors, such as road transport and aviation (blue), up to 2030, according to the IEA’s Oil 2024 report.

Numbers above zero indicate an increase in oil demand compared to the previous year, while numbers below zero mean a decrease.

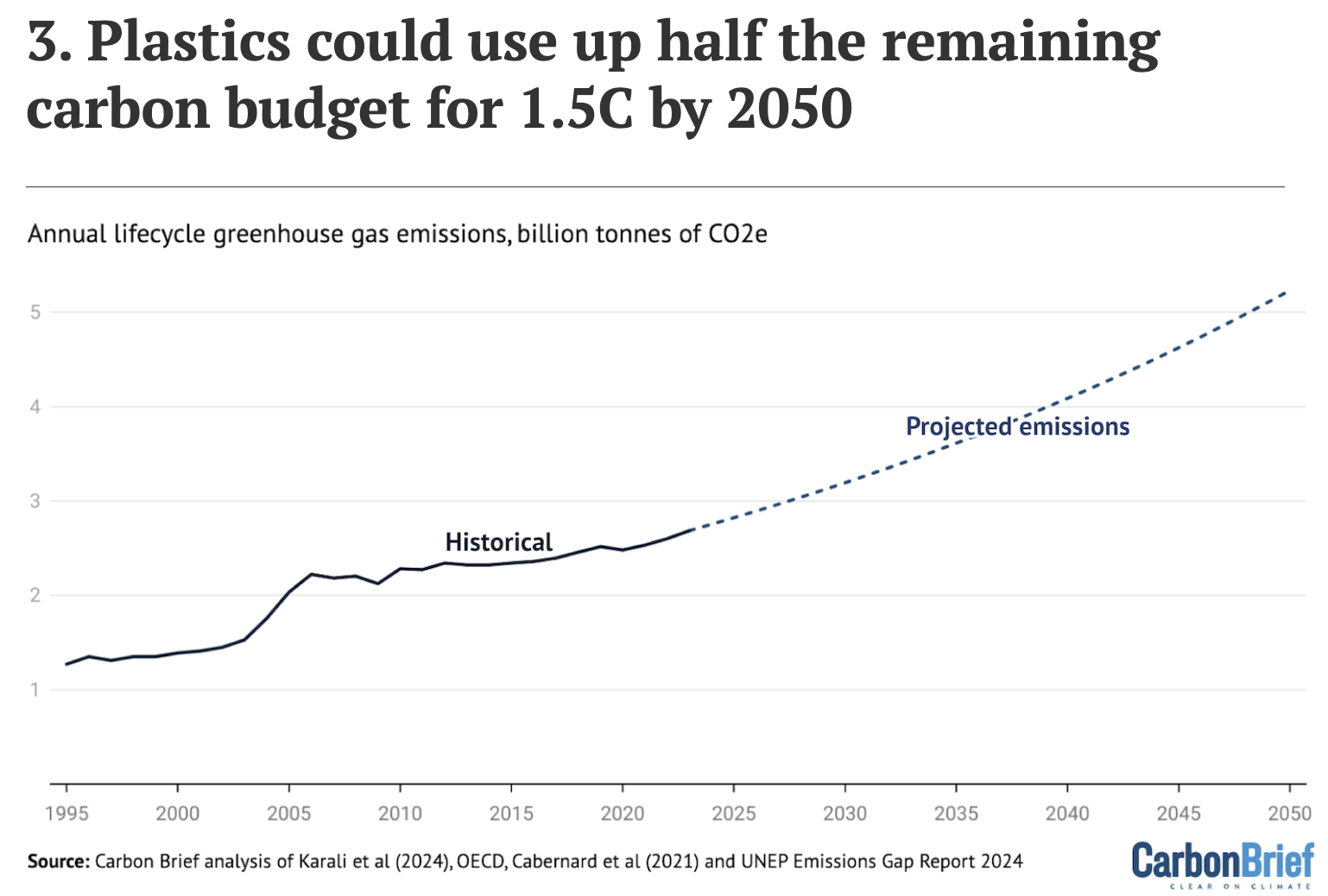

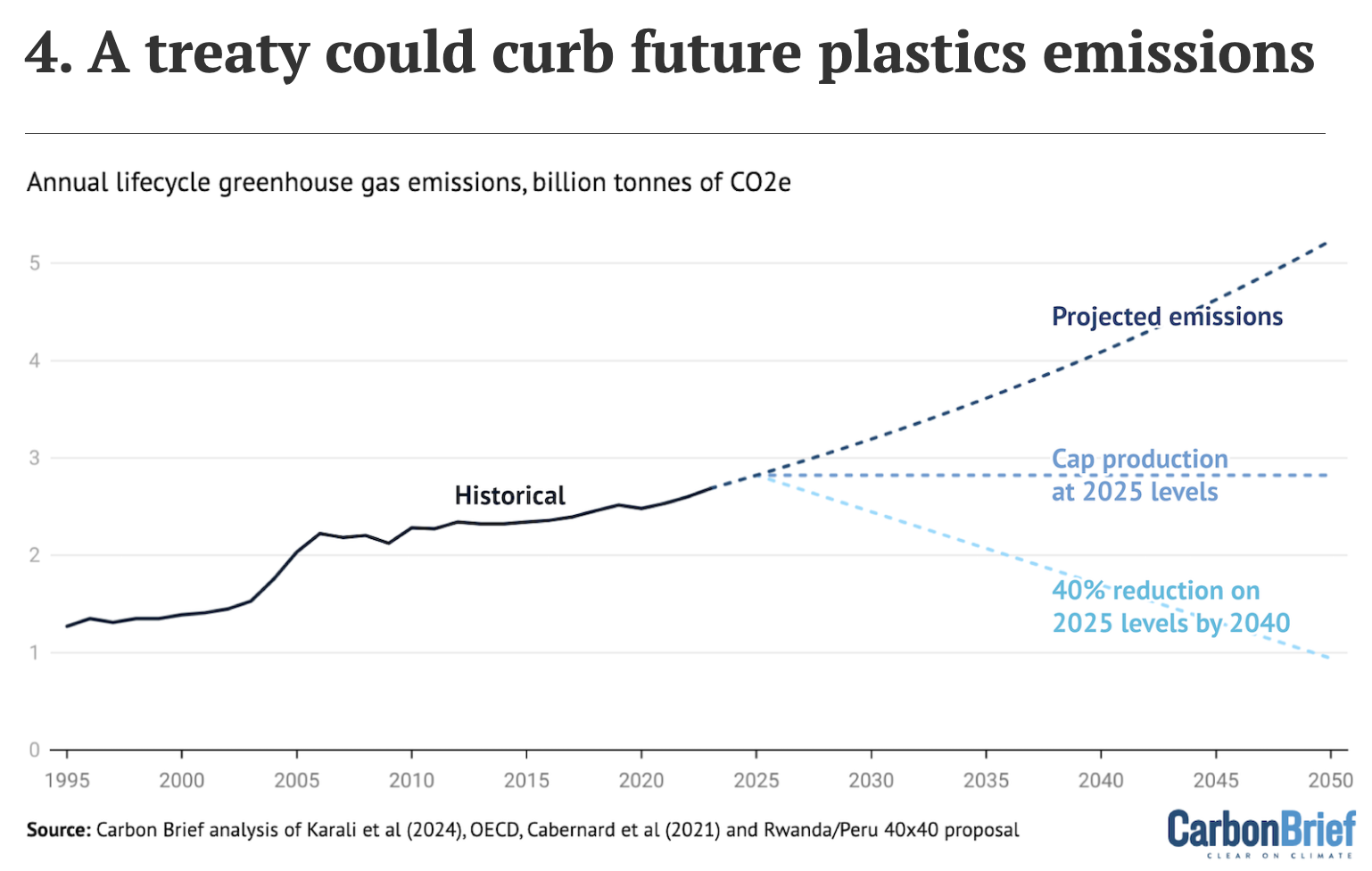

Annual lifecycle greenhouse gas emission, in billions of tonnes of CO2e. Source: Carbon Brief analysis of Karali et al (2024), OECD, Cabernard et al (2021) and the UNEP Emissions Gap Report (2024).

To have a 50% chance of limiting global warming to 1.5C above pre-industrial levels, humanity can only emit a further 200bn tonnes of CO2, according to the latest estimate from the emissions gap report from the UN Environment Programme (UNEP).

Unless there is a change in current trends, plastics production is expected to use up a significant proportion of this carbon budget.

A landmark 2024 report from the Lawrence Berkeley National Laboratory (LBNL) outlines two scenarios for plastics growth between now and 2050. Under its “conservative growth scenario”, the report says that plastics production will grow by 2.5% per year, based on projections of the Organisation for Economic Co-operation and Development (OECD).

Meanwhile, an alternative scenario is defined by a much more rapid 4% per year growth scenario, based on projections from National Academies of Sciences, Engineering and Medicine (NASEM)

Carbon Brief finds that, under the conservative growth scenario, annual “lifecycle” emissions from plastics could double by 2050, reaching 5.2GtCO2e. Under this scenario, plastics production, use and disposal would cumulatively emit 104GtCO2e between 2024 and 2050, consuming more than half of the remaining carbon budget.

Under the rapid growth scenario, cumulative emissions would be 130GtCO2e – or around 65% of the remaining carbon budget.

The rise in annual emissions from plastics, including all stages from fossil-fuel extraction to plastics disposal, are shown above. The black line indicates historical emissions, while the dark blue line shows the conservative growth scenario from the LBNL report, originally taken from the OECD.

At the negotiations in South Korea, countries will attempt to ratify a legally binding agreement on curbing plastics pollution.

Daniela Duran Gonzalez is a senior legal campaigner focused on the plastics treaty at the Centre for International Environmental Law (CIEL). She tells Carbon Brief that when discussing emissions from plastics at INC-5, experts usually focus on limiting production because plastics production is “challenging to decarbonise”.

At the negotiations, countries will consider a global target to limit plastics production, Duran explains. She likens this to the Paris Agreement 1.5C warming limit, arguing that “it gives us a north star, but it doesn’t provide any enforceable obligation to any country to actually achieve it”.

If it is agreed, the treaty could stipulate different ways to achieve this overall target. The first option, which Duran says is “very vague”, is for countries to all work towards the target at their own discretion, without any targets set.

Another method with more accountability would be for countries to set their own voluntary, non-legally binding and non-enforceable measures – similar to the climate pledges (“nationally determined contributions”) that countries submit under the Paris Agreement.

The most enforceable method on the table would be to set legally binding targets for each country, Duran explains. She says this could work in a similar way to the Montreal Protocol, which successfully cut global emissions of substances that deplete the ozone later.

To set targets, countries would need to agree on a baseline year to measure against, a goal and a deadline for the goal to be met.

For example, at the last set of negotiations (INC-4) earlier this year in Ottawa, Rwanda and Peru put forward a global target for a 40% reduction on 2025 levels by 2040. Under this scenario, plastics would emit 52GtCO2e by 2050.

Others have suggested a cap on plastic production at 2025 levels – a scenario that would see the production, use and disposal of plastics emit 76bn tonnes of CO2e by 2050. These scenarios are shown in light blue and blue on the graph above.

In early November, Ecuadorian ambassador Luis Vayas Valdivieso – chair of the INC – developed and submitted his non-paper three to the committee for the talks. This document set out his proposed basis for the negotiations.

Under the proposal, a single party would be able to veto any decision, similar to the process under the UN climate regime. WWF warns that this “can result in a stagnant and dead treaty, incapable of adapting to changing developments and circumstances in the future”.

Developed countries have already been accused of bowing to pressure from lobbyists seeking to avoid any caps on plastics production at the international negotiations. According to CIEL analysis, at the last set of talks, 196 fossil fuel and industry lobbyists registered, up from the 143 who registered at the previous discussions in Nairobi.

Duran tells Carbon Brief that plastics production is an “existential” issue for Gulf countries, whose economies currently rely on continued oil and gas extraction.

As a result, she says that these countries likely will not be “negotiating in good faith” at the INC-5 and “will never accept a treaty that has any mention of plastic production, because it’s their lifeline”. She argues for other countries to “overcome this idea of universal ratification” to ensure a “good” treaty.

According to expert interviews conducted by the University of Portsmouth, crucial outcomes from the negotiations include deciding on a voting mechanism as a backup if consensus cannot be reached.

(The UN climate regime must take all decisions by consensus because rules on how it makes decisions – including voting – were never agreed.)

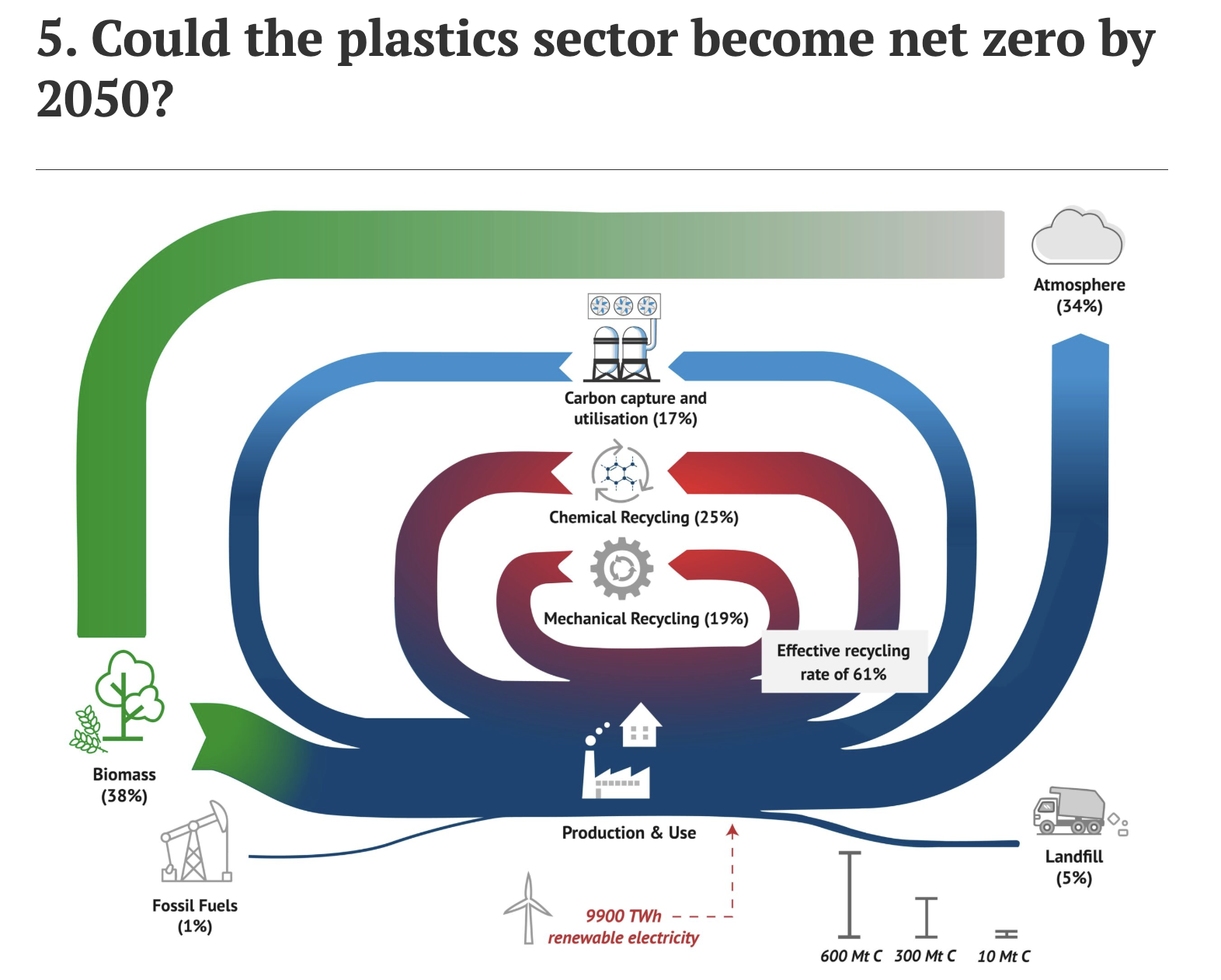

Carbon content flows for the proposed ‘circular carbon’ net-zero plastics sector pathway in the year 2050, million tonnes of carbon (MtC). TWh = terawatt hour. Source: Based on Meys et al (2021)

INC-5 negotiations could lead to a reduction in plastics production, which could be key to limiting emissions from the industry. However, decarbonising the production, use and disposal of plastics could also help to bring down the carbon footprint of the sector.

One way to reduce emissions is to recycle plastics. Only 9% of plastics that have ever been produced have been recycled. However, the present-day number is likely higher, as recycling rates around the world are rising.

A report by the IEA says that most plastics recycling today is physical or “mechanical”. This involves grinding down plastics without changing their chemical structure, but can lead to the quality of plastics degrading over time.

Meanwhile, chemical recycling is becoming more popular, it says. This involves breaking down the plastics back into small chemical sections called monomers, which can be used to make new plastics. This method generally produces a higher-quality plastic, but it can be more energy intensive, resulting in higher emissions.

Another option is to switch from using petrochemical feedstocks, which are derived from fossil fuels, to using alternative feedstocks.

Bio-based feedstocks, such as starch, can also be used to produce plastics. These biological materials draw down carbon as they grow and also do not have the emissions associated with fossil fuel extraction.

Meanwhile, carbon capture, utilisation and storage (CCUS) can be used to draw down CO2 from chemical plants before it enters the atmosphere. The captured CO2 can be combined with hydrogen to generate synthetic feedstocks. Using renewable energy to produce the hydrogen for this process can help to keep the materials’ carbon footprint low.

The IEA report says that the “use of alternative feedstocks, including bio-based feedstock, remains a niche industry due to a considerable cost gap and competing demand with other sectors”.

A 2021 study explores four pathways through which the global plastics industry could reach net-zero by 2050. These are: a recycling pathway; a CCUS pathway; a biomass pathway; and a circular carbon pathway that combines the three approaches in an “optimal” way.

The combined pathway, shown above, is the only scenario that reaches net-zero emissions.

The chart shows the flow of carbon (in million tonnes) through the full lifecycle of plastics under a net-zero scenario in the year 2050. The width of each arrow corresponds to the amount of carbon flowing. In this scenario, around 38% of plastic feedstocks would be made from biomass, 17% from synthetic feedstocks, 44% from recycling and less than 1% from fossil fuels. This scenario would require an effective recycling rate of around 61%, with only 5% of plastics going to landfill and 34% ending up in the atmosphere through incineration.

However, the authors highlight how challenging it would be to fully decarbonise plastics, if production levels continue to rise.

Cutting emissions while production increases would require a significant uptick in the rate of plastics recycling, they note – and the feasibility of fully decarbonising plastics production will be limited by the amount of renewable energy and biomass available to the sector.

In the scenario above, the plastics sector would require 9,900 terawatt hours of renewable electricity (more than global renewable generation in 2023 or 14% of renewables generation under IEA net-zero scenario in 2050), and 19.3 exajoules of biomass (11% of “untapped” biomass potential in 2050).

Duran tells Carbon Brief that, while the INC-5 can talk about limiting production levels, it has not “entered into the discussion of decarbonising the petrochemical industry”.

She says that there are many reasons for this, including political factors and the uncertainty around measures such as CCUS. However, she also says that “decarbonisation is an issue of the United Nations Framework Convention on Climate Change (UNFCCC)”.

She explains that the UNFCCC cannot make rulings on plastics production, but can set out frameworks for the transparency and reporting of greenhouse gas emissions caused by plastic production.

Methodology

The Carbon Brief analysis on the lifecycle greenhouse emissions in this article is based on using the production-related emissions figures from the LBNL study (Karali et al., 2024), and combining this with an estimate of the end of life emissions from OECD data.

In order to make these datasets compatible, it is assumed that the percentage share of emissions from end of life, calculated from OECD data, remains constant at 10.8% and then this is applied to the production-related emissions from LBNL.

Due to differences in methodology, scope and poor availability of detailed data, generally, there are varying estimates of the climate impact from plastics. This analysis uses the values from LBNL study because it is the most recent and comprehensive evaluation of the climate impact from plastics, as confirmed by an expert that Carbon Brief spoke to.

However, the emissions measured in that study are higher than commonly cited estimates from the OECD, which suggests that production emissions in 2019 are around 28% lower than the LBNL estimate. This highlights the large uncertainty in measuring the climate impact of plastic, but the LBNL study authors also note that their higher estimate is “due to the increased level of granularity in modelling production processes, technologies and routes”. Their study also has no “by-product’ assumption”, which they say leads to an underestimation of the climate impact of plastics in other studies if they do not attribute emissions by mass across all the products of a given chemical process.

Historical data for plastics emissions is taken from a combination of LBNL, OECD and Cabernard et al (2021). Due to differences in methodology and uncertainty in the data, these different datasets do not match exactly and, therefore, have been scaled based on overlapping years to ensure that they are aligned with the values from the LBNL.

In order to model future emissions in a consistent manner, a constant emissions intensity per tonne of plastic produced from the LBNL study is used (4.9tCO2e per tonne of plastic, excluding end-of-life emissions) and applied to the production projections for each of the three scenarios presented (2.5% growth, cap at 2025 levels, 40% reduction from 2025 levels by 2040).

The baseline plastics-production projections are taken from the LBNL study, which uses OECD projections of plastics demand under a 2.5% growth scenario and assumes that annual plastics production matches annual demand. The projected end-of-life emissions from plastics are then calculated by using the assumed constant percentage share of emissions (10.8%) from end of life, as per above. For the 40% reduction scenario, it is assumed that production levels continue to reduce at the same rate between 2040 and 2050.

This article was originally published on Carbon Brief under the Creative Commons BY NC ND licence. Read the original article.