The region has emerged as a leading solar exporter, helped by Chinese companies’ relocating their production – but US tariffs are beginning to bite

.jpg)

A worker inspects cables at a floating solar power project in Rayong, Thailand. Southeast Asian countries have welcomed investment to produce solar equipment domestically, though this has largely been destined for export to the United States rather than supporting local capacity (Image: Wang Teng / Imago / Alamy)

In little over a decade, Southeast Asia has become one of the world’s top exporters of solar power equipment – a success driven significantly by the relocation of Chinese manufacturers to the region. But now, the sector faces considerable challenges as US tariffs cut off their main export market, intensifying pressure on a previously booming trade.

Ever since finding themselves in the crosshairs of US import tariffs in 2012, Chinese solar manufacturers began shifting their production to Southeast Asia to circumvent trade barriers. More recently, overcapacity and brutal price wars in China’s domestic market have accelerated these international relocations.

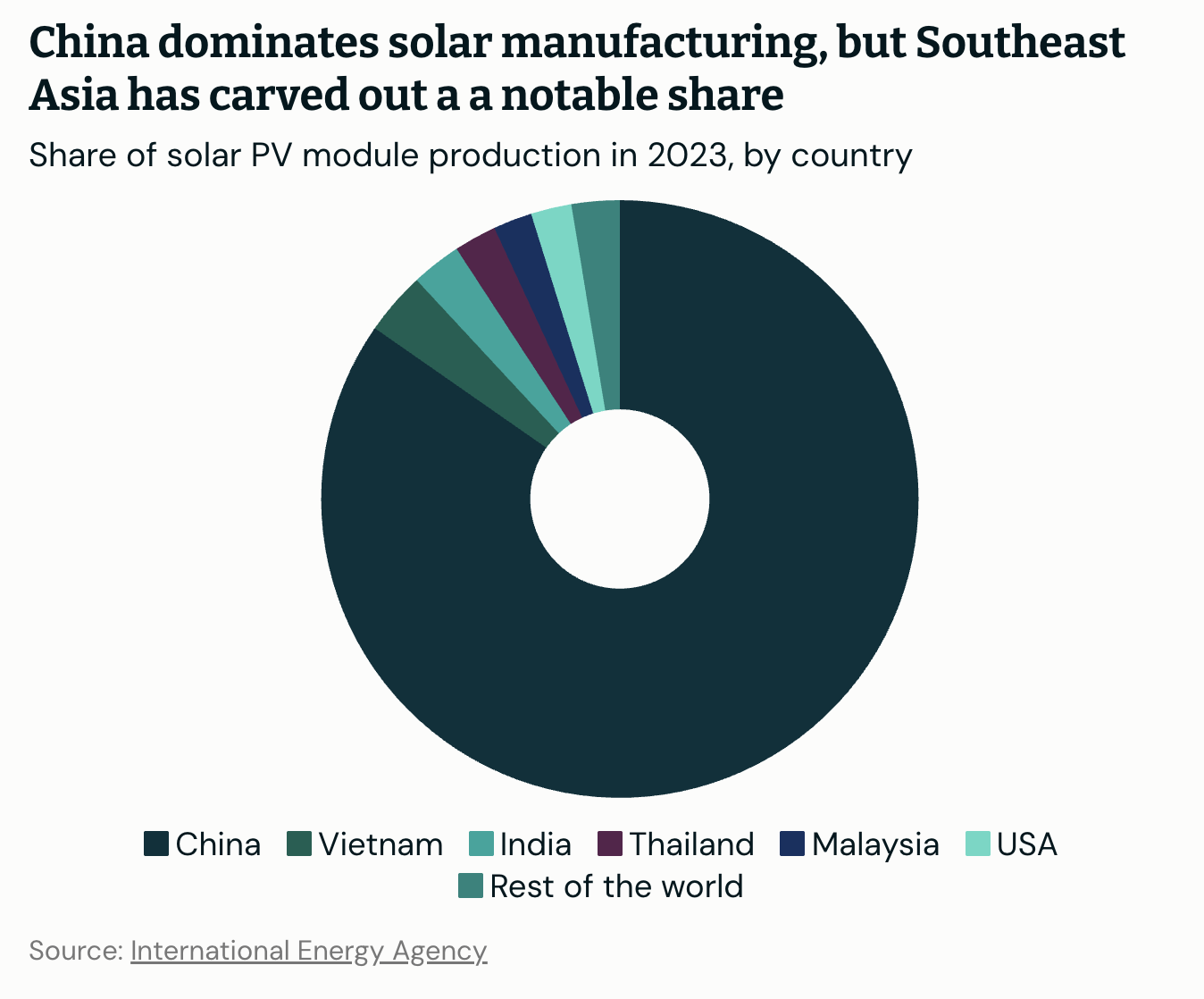

The arrival of factories backed by Chinese solar heavyweights such as Trina, Longi, JA Solar and Jinko Solar, among nearly 20 other competitors, has transformed Malaysia, Vietnam, Thailand and Cambodia into world-leading production and export hubs for a range of solar components. Together, these countries account for over 40% of global manufacturing capacity of solar modules outside China, and around 20% of worldwide exports.

Southeast Asia’s solar exports have primarily targeted the US, with more than 80% of the equipment it imported in the first half of 2024 sourced from Malaysia, Vietnam, Thailand and Cambodia, according to BloombergNEF.

But this successful run is now under threat. In June 2024, then-US president Joe Biden ended a two-year relief on import tariffs for solar panels from the region’s four leading producers, targeting China-linked manufacturers over alleged unfair business practices. Additional levies announced in November prompted several Chinese manufacturers to suspend or scale-back production or shift operations to Indonesia and Laos, which were exempted.

This uncertainty has now been exacerbated by President Donald Trump’s 21 April announcement of hefty tariffs on Southeast Asian solar manufacturers, reaching unprecedented heights of up to 3,521% for some exporters, though varying by country and company. Trina Solar, for example, has been hit with tariffs totalling 375% on its production in Thailand, while Jinko Solar will face rates of 120% on its exports from Vietnam, but lower levies of 40.3% from Malaysia.

Prior to this latest round of tariffs, Dialogue Earth spoke with experts and analysts to hear more about Chinese solar manufacturers’ presence in Southeast Asia, the reception they have received, and what may lie ahead for an industry feeling the heat of global trade tensions.

A triangular trade

The solar sector is just one aspect of a broader trend of Chinese manufacturing investments reshaping Southeast Asia. Investments in the 10 countries of the Association of Southeast Asian Nations (Asean) reached USD 17.6 billion in 2023, according to a recent report by the Asia Society, a US-based think-tank. Besides solar, other key sectors include electric vehicles, batteries and steel.

According to the Asia Society, this investment surge has been driven by Chinese companies’ aiming to avoid trade barriers in advanced economies, to seek lower production costs, and to capitalise on Asean’s strategic position as a global gateway.

Notable Chinese solar investments include Trina Solar’s two factories in Vietnam, producing silicon wafers and solar cells, with a third, USD 454 million, 25-hectare facility announced. Longi has spent more than USD 1.1 billion on multiple facilities in Malaysia, employing over 8,000 people as of 2023, although some operations have reportedly halted in response to tariffs.

Yang Muyi, senior energy analyst at global energy think-tank Ember, said that Chinese technological expertise had helped to accelerate Southeast Asia’s own solar industry.

“China’s success in solar manufacturing did not happen overnight; it was the result of decades of sustained policy support, including long-term investment, research and development funding, and the development of integrated industrial clusters,” Yang told Dialogue Earth. “Even with these strong domestic policies, it still took years for Chinese companies to become global leaders.”

China-backed projects in Southeast Asia have attracted capital, created jobs and supported the upgrading of local industries, he added.

.jpg)

An employee at one of Chinese solar manufacturer Trina Solar’s factories in Vietnam’s Bac Giang province (Image: Imago / Alamy)

Such industrial development is among the reasons that Southeast Asian governments “have been nearly uniformly welcoming of and seeking out” increased Chinese foreign direct investment, the Asia Society report’s authors wrote. The economic benefits have been substantial, with US solar imports from Malaysia, Vietnam, Thailand and Cambodia reaching USD 12 billion in 2023 alone. However, the Asia Society report warned of risks from over-dependence on Chinese industrial inputs and investments amid growing global trade tensions – underscored by the Biden-era tariffs, which caused US solar imports from the region to plummet in the second half of 2024.

Not all Chinese investments have been welcomed locally. Putra Adhiguna, managing director of the Energy Shift Institute, an Asia-focused energy finance think-tank, highlighted controversies surrounding Chinese company Xinyi’s solar manufacturing project on Rempang Island, Indonesia. The solar facility, part of designs for a new “eco city”, sparked protests in 2023 from local communities over plans to evict thousands of residents. Construction has since remained stalled as the government continues to negotiate relocations, reportedly now pursuing a “softer approach”. In March, Indonesia’s transmigration minister issued an official apology to residents who had previously been forcibly evicted.

Responding to tariffs

Even before the Biden administration’s 2024 tariff increases, Chinese solar companies in Southeast Asia had already begun pre-emptively shifting their strategies to avoid trade barriers. Data from the Rhodium Group, a China-focused research provider, shows a significant pivot in Chinese solar investments in 2022 and 2023 towards Laos and, in particular, Indonesia. Previously receiving little attention, these two nations saw billion-dollar commitments, accounting for almost half of the region’s total solar investments over this period.

Other Chinese-linked projects in Indonesia include Trina’s Mas Agra solar cell and module factory, which began operations in October 2024, and Thornova’s new solar module facility launched in November with plans previously announced to export to the US by mid-2025.

However, such ambitions now face major hurdles following the Trump administration’s slew of tariffs. These include not only those targeting solar manufacturers, but also its so-called “reciprocal” tariffs on around 90 nations, launched earlier in April, though later paused until July.

Speaking to Malaysian publication The Edge, Davis Chong, president of the Malaysia Photovoltaic Industry Association, described Chinese-owned firms in the country as having already been almost “killed off” by previous US tariffs. Though the most recent solar tariffs will require final confirmation by the US International Trade Commission in June before coming into effect, Chong said the association expected more Chinese manufacturers to leave the market. Earlier in the month, Bloomberg analysts had similarly suggested US tariffs “might induce producers to leave Southeast Asia altogether” in favour of regions such as the Middle East.

As the US becomes an increasingly inaccessible export market, the possibility of the region looking to alternative markets has been raised. “It’s not so much about Southeast Asian nations reducing their dependency on China as it is about reducing their dependency on the US as a market,” Grant Hauber, strategic energy finance advisor for Asia at the Institute for Energy Economics and Financial Analysis, told Dialogue Earth.

However, the short-term outlook for diversifying export markets seems mixed. The European Union, for example, sources 97% of its solar equipment directly from China, which it has not subjected to tariffs, leaving little room for Southeast Asian producers to quickly offset their losses from the previously dominant US market. Though the bloc’s 2024 European Solar Charter encouraged diversification of supply chains, highlighting risks in the reliance on China, its focus was largely on supporting European manufacturers that have struggled to compete with the low prices driven by Chinese production – prices with which Southeast Asian solar exporters will also be competing in the EU market.

Can local markets plug the gap?

Amidst ongoing trade uncertainties between the US and China, Southeast Asia’s domestic markets could offer a valuable hedge against external uncertainties, according to Yang.

He said accelerating domestic transitions towards clean electricity could generate substantial local demand for solar equipment and infrastructure. But, he cautioned, “there is little time to wait as other regions move quickly to scale up their clean energy industries”.

Despite significant manufacturing capacity growth, local solar installations across Southeast Asia have been inconsistent. “The results for domestic solar installations have been mixed, with growth varying, and driven more by country-level policies,” said Adhiguna.

Vietnam stands out with 18.4GW of installed capacity as of 2023, driven by a robust feed-in tariff scheme for solar and wind, “which saw Vietnam go from nowhere on the renewables map to one of the top markets in the world in just two years,” explained Hauber.

We have a fossil fuel hangover in the region… leaving them behind is hard

- Grant Hauber, strategic energy finance advisor for Asia, Institute for Energy Economics and Financial Analysis

However, experts pointed to barriers that prevent the region absorbing its surplus export capacity domestically. High among these may be the dominance of fossil fuel interests regionally.

Chalie Charoenlarpnopparut, an associate professor at Sirindhorn International Institute of Technology in Bangkok, described policymakers in Thailand as being “scared” of solar development due to competition with established natural gas interests. Regulatory hurdles are slowing approvals for solar projects – large and small: “Even for households or a small business, if they want to install solar rooftop, they still have some difficulties,” he said.

In Indonesia, meanwhile, coal interests are proving hard to overcome, despite pledges to phase-out fuel by 2040. “We have a fossil fuel hangover in the region – Indonesia’s state-owned enterprises and key individuals built their wealth and power from those sources, and leaving them behind is hard,” said Hauber.

Further barriers identified by Hauber include grid connectivity issues, logistical and labour costs, as well as the limited production range of solar components within individual countries. “Governments think if they sign a deal with a solar panel manufacturer, they’ll have solar power made in their country. No, it’s not: it’s one small component. It’s shiny, high-tech and sexy, but it doesn’t get you electricity to the grid.”

Adhiguna echoed Hauber’s view on the need for a broad diversification of Southeast Asia’s solar markets – within and beyond the region, or focusing on domestic demand. He recommended deepening involvement across the solar value chain, despite acknowledging the significant challenges involved. “It’s not easy, as production in early products such as polysilicon is capital-intensive, amid fierce market competition. Deepening the value chain will, nevertheless, likely bring mutual benefits for both the Chinese companies and Southeast Asian countries’ long-term outlook.”

Adhiguna remained optimistic about Southeast Asia’s solar potential, but stressed the importance of improving the sector’s offering amid intensifying competition from places such as India, which are increasingly localising solar manufacturing. “Investors would like to see a clear project pipeline that they can deliver in the short-to-medium term, not too far in the horizon,” he added.

Soraya Kishtwari and Tyler Roney also contributed reporting to this article.

- This article was originally published on Dialogue Earth under the Creative Commons BY NC ND licence. Read the original article.

.jpg)